How Lenders Project Rent in Las Vegas Without a Lease

Buying a vacant investment property in Las Vegas presents a classic challenge: how do you prove rental income without a tenant? A Debt Service Coverage Ratio (DSCR) loan is designed to solve this. Instead of relying on your personal income or an existing lease agreement, lenders qualify the loan based on the property's potential to generate income.

The key to this process is a specialized appraisal that includes a market rent analysis. Lenders use this objective, third-party assessment to confidently project future cash flow and approve your financing.

Key Documents for Projecting Rental Income

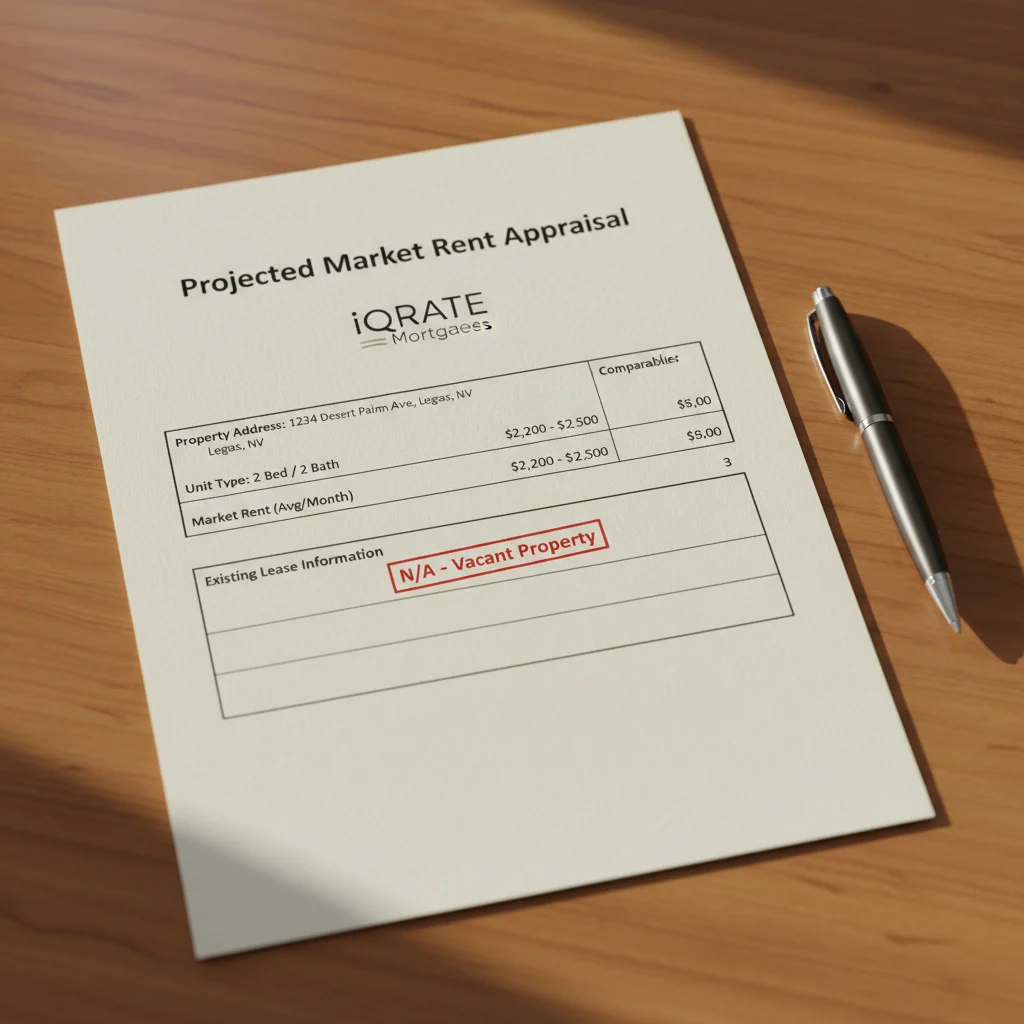

While every lender has specific requirements, the primary document used to establish projected rent for a vacant home is the appraisal report. Depending on the property type, the appraiser will complete one of two forms:

- Form 1007 (Single-Family Comparable Rent Schedule): This is used for single-family homes, including detached houses, townhomes, and some condos.

- Form 1025 (Small Residential Income Property Appraisal Report): This form is for properties with 2-4 units, like duplexes or fourplexes.

These forms are addendums to the main appraisal report (Form 1004). They provide a detailed, data-backed opinion of what the property could realistically rent for in the current market, giving the lender the figure they need to calculate the DSCR.

How Appraisers Determine Market Rent for a DSCR Loan

An appraiser’s goal is to determine the Fair Market Rent for the property. This isn't a guess; it's a methodical analysis based on real-world data from the local market, whether it's a bustling neighborhood in Henderson or a growing suburb of Reno.

Here’s a breakdown of the process:

- Selection of Comparable Rentals: The appraiser identifies at least three similar properties in the immediate vicinity that have recently been rented. These 'comps' should be as close as possible in terms of size, bedroom/bathroom count, age, and condition.

- Data Analysis and Adjustments: The appraiser analyzes the rental price of each comp and makes value adjustments. For example, if your subject property in Las Vegas has a newly renovated kitchen but a comparable rental does not, the appraiser will adjust the projected rent upward. If a comp has a pool and yours doesn’t, a downward adjustment is made.

- Location and Market Trends: The appraiser considers the specific desirability of the neighborhood, proximity to amenities like schools and parks, and current local rental market trends. Is demand high? Are rents rising or stabilizing?

- Final Rent Opinion: After synthesizing all this data, the appraiser provides a final, conclusive opinion of the property's market rent. This is the figure the lender will use for their DSCR calculation.

Example: Imagine you're buying a 3-bedroom, 2-bathroom single-family home in Henderson. The appraiser finds three similar homes in the same zip code that rented within the last 90 days for $2,400, $2,550, and $2,450 per month. After minor adjustments for features, the appraiser might conclude your property’s market rent is $2,475 per month.

Can I Use Short-Term Rental Data for a Vacant Henderson Property?

This is a common question, especially in tourist-driven markets like Henderson and Las Vegas. The answer depends entirely on the lender and the specific DSCR loan program.

- Standard DSCR Loans: Most DSCR lenders prefer to use long-term rental data (12-month leases) because it represents a more stable and predictable income stream. They will typically rely on the Form 1007 or 1025 for their projections and will not consider potential Airbnb or VRBO income.

- Specialized 'STR' DSCR Loans: A growing number of niche lenders now offer DSCR loans specifically for short-term rentals. These lenders may accept data from platforms like AirDNA or Mashvisor to project income. These programs often have different requirements, such as a higher credit score or larger down payment, to offset the income volatility of short-term rentals. The data, information, or policy mentioned here may vary over time.

It is crucial to be upfront with your mortgage strategist about your rental strategy so they can connect you with a lender whose program aligns with your goals.

What is a Debt Service Coverage Ratio and How is it Calculated?

The Debt Service Coverage Ratio is a simple calculation lenders use to measure a property's ability to cover its own expenses. It compares the property's gross rental income to its total housing payment.

The formula is:

DSCR = Gross Monthly Rental Income / Total Monthly Housing Payment (PITI)

PITI stands for:

- Principal

- Interest

- Taxes (property taxes)

- Insurance (homeowner's insurance)

Most lenders require a DSCR of at least 1.0, which means the rental income is equal to the expenses. However, more competitive programs and better interest rates are available for properties with higher ratios, such as 1.15 to 1.25 or more. The data, information, or policy mentioned here may vary over time.

Calculation Example:

Let's say you're buying an investment property in Reno.

- Projected Gross Monthly Rent (from appraisal): $2,800

- Estimated Monthly PITI: $2,200

DSCR = $2,800 / $2,200 = 1.27

With a DSCR of 1.27, this property easily qualifies for most DSCR loan programs.

Are Interest Rates Higher for DSCR Investor Loans Without Tenants?

Interest rates for DSCR loans on vacant properties may be slightly higher than for a tenant-occupied property. Lenders view a vacant property as having a small amount of additional risk; there is no immediate, proven cash flow. This 'risk premium' can translate to an interest rate that is 0.125% to 0.375% higher. The data, information, or policy mentioned here may vary over time.

However, this minor difference is the trade-off for the ability to finance a property based on its potential rather than your personal income. For many real estate investors, the flexibility and speed of a DSCR loan far outweigh the small increase in the interest rate.

Does My Personal Income Matter for These Types of Investor Loans?

For a true DSCR loan, your personal income and debt-to-income (DTI) ratio are not used for qualification. The underwriting decision is based almost entirely on the property's cash flow potential, as measured by the DSCR.

This is a significant advantage for self-employed investors, business owners, or those with complex tax returns. You don't need to provide W-2s, tax documents, or pay stubs.

That said, lenders do have other requirements. You will still need:

- A good credit score: Most lenders look for a minimum credit score of 640, with the best rates reserved for scores of 720 and above. The data, information, or policy mentioned here may vary over time.

- A down payment: Down payments for DSCR loans typically range from 20% to 30%. The data, information, or policy mentioned here may vary over time.

- Cash reserves: Lenders will verify you have sufficient funds in the bank to cover several months of PITI payments after closing, usually 3-6 months. The data, information, or policy mentioned here may vary over time.

How Long Does the DSCR Loan Approval Process Take for Vacant Homes?

The timeline for closing a DSCR loan on a vacant home in Nevada is quite similar to that of a conventional loan, typically taking between 21 to 35 days from application to closing. The data, information, or policy mentioned here may vary over time.

The critical step that can influence the timeline is the appraisal. Since the lender is relying heavily on the appraiser's rent schedule, it’s essential to order the appraisal as soon as possible. A qualified appraiser familiar with rental properties in Las Vegas or Henderson can complete the report efficiently, keeping the process on track.

A typical timeline looks like this:

- Week 1: Application submission and appraisal order.

- Week 2: Appraisal inspection and report completion.

- Week 3: Underwriting review of the appraisal and borrower's credit/assets.

- Week 4: Final approval and scheduling the closing.

Don't let a vacant property stop you from growing your portfolio. If you're ready to explore a DSCR loan for your Nevada investment, take the next step. A knowledgeable mortgage strategist can identify the right lender for your scenario, ensuring a smooth closing. Apply now to see what you qualify for.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.