Is a 'no-cost' Interest Rate Reduction Refinance Loan actually free?

Veterans in Florida often encounter lenders advertising a 'no-cost' or 'no-fee' Veterans Affairs Interest Rate Reduction Refinance Loan (IRRRL), also known as a VA Streamline Refinance. This marketing can be misleading. A VA IRRRL is never truly free; the costs are simply paid for in a different way. Understanding how these offers are structured is the first step to protecting your finances.

There are two primary methods a lender uses to offer a seemingly 'no-cost' refinance:

Rolling Costs into the Loan Balance: This is the most common approach. The lender takes all the allowable closing costs and adds them to your new loan principal. You don't bring cash to closing, but your total mortgage debt increases. For example, if you refinance a $350,000 mortgage in Jacksonville and the closing costs are $5,000, your new loan amount becomes $355,000. Your monthly payment will still be lower due to the reduced interest rate, but you are now paying interest on a larger balance over the life of the loan.

Accepting a Higher Interest Rate (Lender Credits): In this scenario, the lender offers you a slightly higher interest rate than the absolute lowest rate available. In exchange, the lender provides a 'credit' that is used to pay for some or all of your closing costs. You might get a 4.0% interest rate instead of a 3.75% rate, but the lender covers your fees. This can be a good option if you want to avoid increasing your loan balance, but it's crucial to compare the long-term interest cost against the upfront savings.

Ultimately, a 'no-cost' IRRRL is about financing strategy, not charity. The key is to analyze the Loan Estimate from each lender to see exactly how your costs are being handled and which method benefits your financial situation the most.

What closing costs can be included in my new loan amount?

When you refinance your VA loan with an IRRRL, the VA has specific rules about which costs can be financed into the new loan. The goal is to protect veterans from excessive fees. All reasonable and customary closing costs can typically be included.

Here are the common closing costs you can roll into your IRRRL:

- VA Funding Fee: This is a mandatory fee for most veterans, which we'll detail below.

- Origination Fee: This is what the lender charges for processing your loan. The VA caps this fee at 1% of the loan amount. (The data, information, or policy mentioned here may vary over time.)

- Discount Points: These are prepaid interest fees you can pay to 'buy down' your interest rate. You can finance discount points, but the total cost must be reasonable and allow the loan to meet the VA's recoupment requirement.

- Title Insurance and Recording Fees: Costs associated with ensuring the title is clear and recording the new mortgage with the county.

- Credit Report Fee: The cost for the lender to pull your credit history.

- Other Standard Fees: This can include flood zone determination, tax service fees, and other third-party charges.

It is important to note that you cannot roll unrelated debts, such as credit card balances or car loans, into an IRRRL. This type of refinance is strictly for reducing the rate and payment on your existing VA-backed mortgage and does not permit 'cash-out' equity withdrawal, with one small exception for energy efficiency improvements.

How does the Veterans Affairs funding fee work for an IRRRL in Jacksonville?

The VA funding fee is a one-time charge that helps offset the costs of the VA loan program for U.S. taxpayers, reducing the financial burden in case of borrower default. For an IRRRL, the fee structure is simplified compared to a purchase loan.

For nearly all veterans using an IRRRL, the VA funding fee is 0.5% of the loan amount. This rate is consistent whether it's your first time using a VA loan or a subsequent use. The only factor that changes this is your exemption status.

Certain veterans are exempt from paying the VA funding fee. You are exempt if you are:

- Receiving VA compensation for a service-connected disability.

- Entitled to receive compensation for a service-connected disability, but you're receiving retirement or active-duty pay instead.

- A surviving spouse of a veteran who died in service or from a service-connected disability.

Let's use a real-world example in Jacksonville. Suppose you are refinancing your existing VA loan of $400,000. If you are not exempt, your VA funding fee would be:

$400,000 (Loan Amount) x 0.005 (0.5%) = $2,000

This $2,000 fee can be paid in cash at closing or, more commonly, rolled into the new loan amount, making your new principal $402,000 before other closing costs are added.

Can my monthly mortgage payment go up with an IRRRL in Pensacola?

The primary purpose of an IRRRL is to lower your monthly mortgage payment. In most cases, your new principal and interest (P&I) payment must be lower than your current one. However, the VA allows for a few specific exceptions where the payment is permitted to increase.

Here are the scenarios where your payment could rise with an IRRRL:

- Refinancing an Adjustable-Rate Mortgage (ARM) to a Fixed-Rate Mortgage: The stability of a fixed rate is seen as a net benefit, so an increase in payment is allowed to escape the risk of a fluctuating ARM.

- Financing Energy Efficient Mortgages (EEMs): If you include the cost of qualified energy efficiency improvements (up to $6,000), your payment may increase.

- Shortening the Loan Term: This is a common and financially savvy reason for a payment increase. For instance, if you're a homeowner in Pensacola refinancing from a 30-year term to a 15-year term, your monthly payment will be significantly higher, but you will build equity faster and pay far less interest over the life of the loan.

- Financing Closing Costs and Discount Points: If you roll a significant amount of closing costs or discount points into the loan, it could slightly increase the payment, although this is less common as the interest rate drop usually offsets it.

If your goal is simply to get the lowest possible payment, you'll want to avoid these scenarios. However, switching to a 15-year term can be a powerful wealth-building tool if you can afford the higher payment.

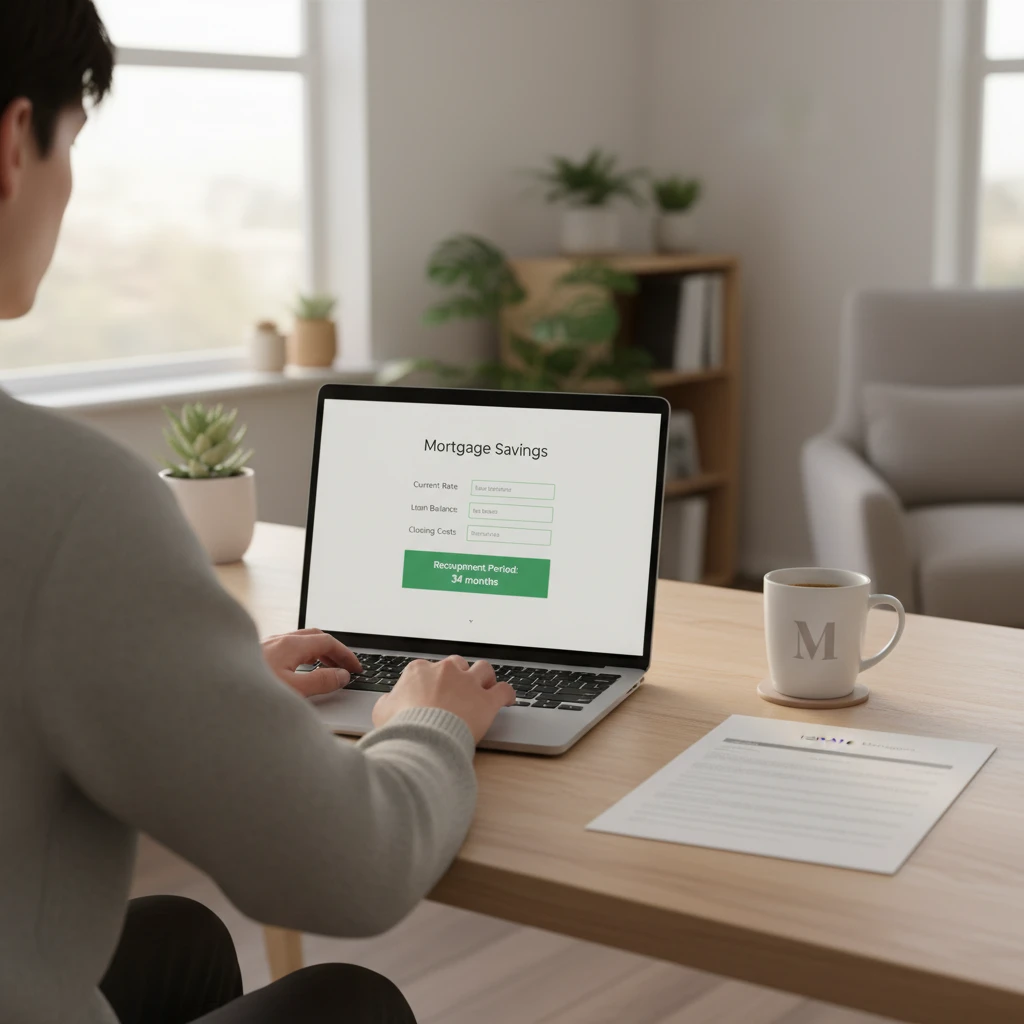

What is the recoupment period and how do I calculate it?

The recoupment period is one of the most important calculations for any refinance. It tells you how long it will take for the monthly savings from your new, lower payment to pay back the total closing costs of the loan. The VA has a strict consumer protection rule: the lender must certify that the veteran will recoup all fees and costs within 36 months of the closing date.

Calculating it is straightforward:

Total Closing Costs / Monthly Savings = Recoupment Period in Months

Let's walk through an example. A veteran in Pensacola is considering an IRRRL.

- Current Monthly P&I Payment: $1,850

- New Monthly P&I Payment: $1,675

- Monthly Savings: $175

- Total Closing Costs (from Loan Estimate): $4,800

Now, apply the formula:

$4,800 / $175 = 27.4 months

In this case, it will take just over 27 months for the veteran to 'break even' on the costs of the refinance. Since 27.4 is well under the 36-month VA limit, this loan meets the requirement. If the calculation resulted in a period longer than 36 months, the lender could not approve the loan.

Do I need an appraisal or credit check for this type of refinance?

The streamlined nature of the IRRRL is one of its biggest advantages, allowing for a faster and less cumbersome process. This often means less documentation and fewer requirements.

Appraisal: For a VA IRRRL, an appraisal is not required. The VA already guarantees a portion of your existing loan, and since you are not taking cash out, they do not need to re-verify the home's value. This saves you several hundred dollars and significant time.

Credit Check: This is a point of frequent confusion. The VA itself does not require a new credit check or income verification for an IRRRL. The logic is that if you have been making payments on your current VA loan, you are a good risk. However, virtually all lenders will require a credit check. Lenders have their own internal guidelines, called 'overlays', to manage risk, and pulling a credit report is a standard part of their process. While a perfect credit score isn't necessary, the lender will want to see that you have a recent history of on-time mortgage payments. (The data, information, or policy mentioned here may vary over time.)

How can I compare different IRRRL offers to find the best deal?

The best way to ensure you're getting a good deal is to shop around and get official Loan Estimates from at least three different lenders. A Loan Estimate is a standardized three-page document that makes it easy to compare offers side-by-side.

When reviewing them, focus on these key areas:

- Page 1: Interest Rate and APR: The interest rate is the cost of borrowing money. The Annual Percentage Rate (APR) is a broader measure that includes the interest rate plus other costs, like origination fees and discount points. A lower APR generally indicates a cheaper loan. (The data, information, or policy mentioned here may vary over time.)

- Page 2, Section A: Origination Charges: This is the lender's primary fee. Compare this number directly between lenders. Some lenders may charge the full 1% allowed, while others may charge less.

- Page 2, Section J: Lender Credits: If you see a number here, it means the lender is giving you money to help cover closing costs, usually in exchange for a slightly higher interest rate. Make sure this trade-off is worth it.

- Calculate the Recoupment Period: Run the recoupment calculation for each offer. A great-looking interest rate isn't so great if it comes with excessively high fees that take years to pay back.

Are there any scenarios where an IRRRL is not a good idea?

While an IRRRL is a fantastic tool for many veterans, it's not always the right move. Rushing into a refinance without considering your long-term plans can be a costly mistake.

An IRRRL might not be a good idea if:

- You plan to sell soon: If you intend to sell your home in Jacksonville or Pensacola before you pass the recoupment period, you will lose money on the transaction. You won't have owned the home long enough for the monthly savings to cover the closing costs you paid.

- The interest rate savings are minimal: The general rule of thumb is that a refinance should lower your rate by at least 0.5%. If the benefit is smaller, the costs might outweigh the savings.

- You need to take cash out: The IRRRL program does not allow you to pull equity from your home. If you need funds for home improvements, debt consolidation, or other expenses, you should look into a VA Cash-Out Refinance instead.

- You are resetting your loan term: Refinancing from a 30-year mortgage you've paid on for 10 years into a new 30-year mortgage will lower your payment, but it also adds 10 years back to your debt schedule. You'll pay significantly more in total interest over the long run. For veterans in Florida, a VA IRRRL can be a powerful tool for saving money, but only when approached with a clear understanding of the costs. Always compare Loan Estimates from multiple lenders and calculate your 36-month recoupment period to ensure the refinance aligns with your financial goals.

Ready to explore if a VA IRRRL is the right move for your financial situation? Apply now to get a clear, no-obligation look at your potential savings and options.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

VA.gov | VA Interest Rate Reduction Refinance Loan (IRRRL)

Consumer Financial Protection Bureau | What is a Loan Estimate?