How is a Federal Housing Administration appraisal different from a conventional one?

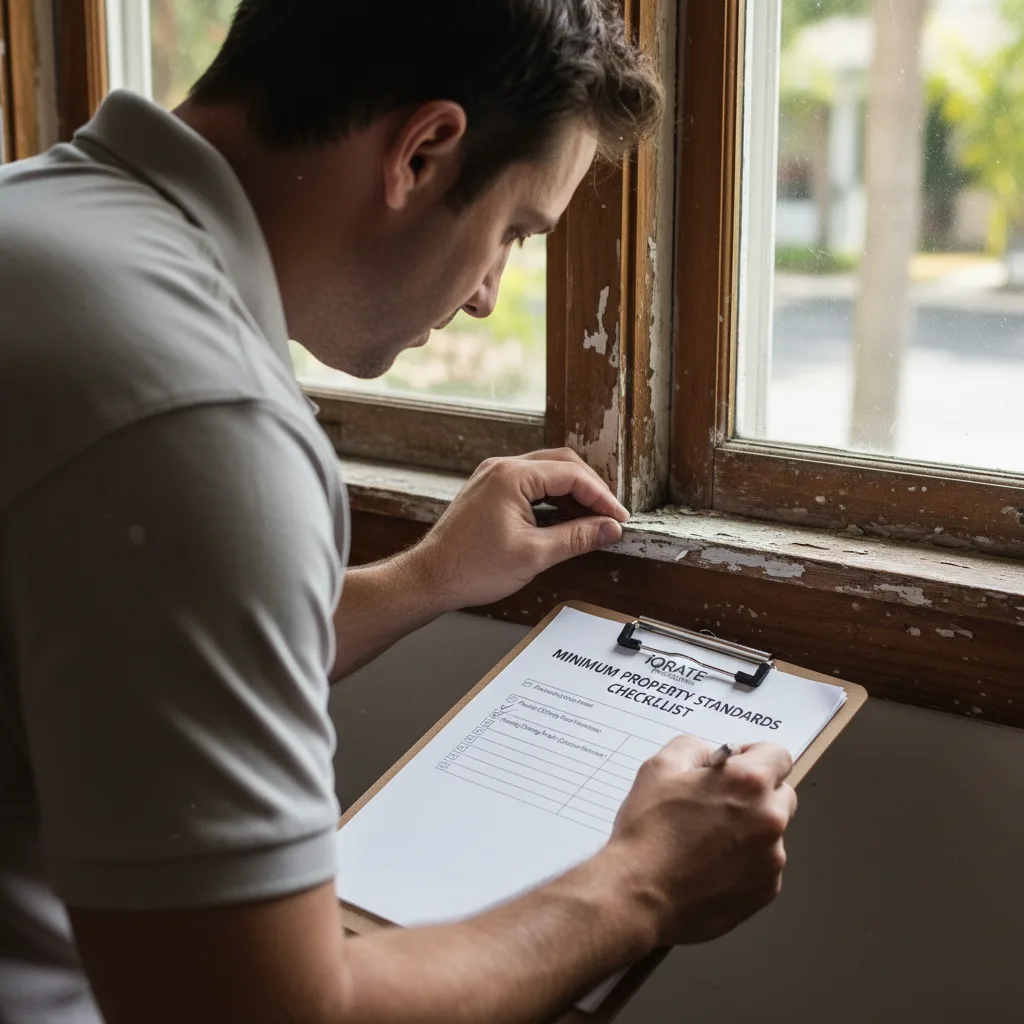

A conventional loan appraisal has one primary job: to determine the home's market value and ensure the lender isn't loaning more money than the property is worth. A Federal Housing Administration (FHA) appraisal, however, has a dual responsibility. It not only establishes the home's value but also serves as a basic safety inspection to confirm the property meets the Department of Housing and Urban Development's (HUD) Minimum Property Standards (MPS).

This second function is the critical difference. An FHA appraiser acts as the eyes for the federal government, which is insuring the loan. They must verify the home is safe, secure, and sound. This means they will flag issues that a conventional appraiser might ignore, leading to required repairs that must be fixed before your loan can be funded.

What are FHA minimum property standards?

FHA's Minimum Property Standards are designed to protect the homebuyer from purchasing a property with significant defects and to protect the FHA's financial interest. The core principle is that the home must be free of any hazards that could affect the health and safety of the occupants or the structural integrity of the property. The standards are often summarized by the 'Three S’s':

- Safety: The property must be free from hazards that could harm residents. This includes issues like exposed wiring, missing handrails on stairs, and evidence of lead-based paint in homes built before 1978.

- Security: The property must be secure and functional. This means exterior doors must lock properly, and windows must be intact. The home should protect its occupants from the elements.

- Soundness: The property's structure must be in good condition. The appraiser will look for signs of foundation damage, significant water leaks, and a roof that has at least two to three years of remaining life.

Other specific items an FHA appraiser will evaluate include:

- A functional and safe heating system.

- Adequate water pressure and a working water heater.

- No active pest infestations, especially termites.

- Proper drainage away from the foundation.

- Attic and crawl space access and condition.

What are the most common repair items an appraiser flags in Tampa?

In Tampa and surrounding areas like St. Petersburg, the climate and age of the housing stock contribute to a specific set of common FHA-flagged issues. Humidity, intense sun, and the risk of termites mean appraisers pay close attention to certain areas.

- Roofing Issues: A roof with curling or missing shingles, active leaks, or that is nearing the end of its lifespan is the most frequent red flag. FHA guidelines generally require a roof to have at least two to three years of life remaining.

- Peeling or Chipping Paint: For any home built before 1978, the appraiser is required to note any areas with peeling paint, both inside and out. This is a potential lead-based paint hazard that must be scraped and repainted by a qualified professional before closing.

- Wood Rot and Water Damage: Florida's humidity can cause wood rot on exterior trim, window sills, and fascia. The appraiser will also look for water stains on ceilings or soft spots in floors, which indicate leaks that must be repaired.

- Outdated Electrical Systems: Older homes in historic St. Petersburg neighborhoods may have outdated electrical panels (like knob-and-tube or certain Federal Pacific panels) that are considered fire hazards and will be flagged for replacement.

- Lack of Safety Features: Missing handrails on staircases with more than three steps, or on porches and decks, is a common and mandatory fix.

Who is responsible for paying for appraisal-required repairs?

This is a critical point of negotiation in your purchase contract. There is no set rule on who pays for FHA-required repairs. The responsibility typically falls to one of three parties or a combination thereof:

- The Seller: In a buyer's market, it's common for the seller to agree to pay for all required repairs to keep the deal alive.

- The Buyer: If the seller refuses, the buyer might choose to pay for the repairs to save the purchase. However, the buyer's lender must approve this, and the buyer must have the cash available, as the costs cannot be rolled into the mortgage.

- A Split Agreement: Often, the buyer and seller negotiate a compromise, splitting the cost of repairs. For example, if repairs total $2,000, they might each agree to contribute $1,000.

It is essential that your real estate contract includes an appraisal contingency that clearly outlines what happens if repairs are required. This protects your earnest money deposit if you and the seller cannot reach an agreement.

Can I switch to a conventional loan if my St. Petersburg home fails the FHA appraisal?

Yes, switching to a conventional loan is a viable strategy if your prospective St. Petersburg home fails to meet FHA's strict property standards. If you are financially qualified, this can save your purchase. For instance, a conventional loan may not require peeling paint to be fixed, whereas it is a non-negotiable FHA requirement.

However, there are important considerations. Conventional loans typically require a higher credit score (often 620 or above) and may have stricter debt-to-income ratio limits than FHA loans. (The data, information, or policy mentioned here may vary over time.) While some conventional loan programs accept down payments as low as 3%, you might need a larger down payment to qualify or avoid private mortgage insurance (PMI). (The data, information, or policy mentioned here may vary over time.) Before making the switch, speak with your mortgage lender to confirm you are eligible for a conventional product and to understand how it might change your interest rate and monthly payment.

What happens if the seller refuses to make the required repairs?

If the seller refuses to make or pay for the FHA-mandated repairs, you have several options:

- Cancel the Contract: If you have an appraisal contingency, you can walk away from the deal and your earnest money should be returned.

- Pay for Repairs Yourself: As mentioned, you can offer to cover the repair costs if you have the funds and your lender approves. This is often a solution when the repairs are minor, such as installing a handrail.

- Renegotiate the Price: You could ask the seller to lower the purchase price by the amount of the repair costs, giving you the financial room to handle the fixes yourself after closing. Note that this only works if you switch to a loan program (like conventional) that doesn't require the repairs to be made before closing.

- Switch Loan Programs: Move from an FHA loan to a conventional loan that doesn't have the same strict property requirements.

How can I identify potential FHA deal-breakers before making an offer?

While you aren't an appraiser, you can learn to spot obvious red flags during a home tour. Being proactive can save you time, money, and heartache. Before making an offer on a home in Tampa, look for:

- Visible Roof Damage: Are shingles missing, curled, or covered in moss? Look for water stains on the ceilings inside.

- Peeling Paint: On homes built before 1978, check window sills, door frames, and exterior siding for chipping or peeling paint.

- Foundation Cracks: Look for large, horizontal cracks in the foundation or 'stair-step' cracks in brickwork.

- Soft Floors: Pay attention to any spongy or soft spots when walking through the home, especially in kitchens and bathrooms, as this can indicate subfloor damage from leaks.

- Missing Utilities: Ensure there is a working stove and that basic utilities appear functional.

Working with a real estate agent experienced in FHA transactions in the Tampa Bay market is your best asset. They can often identify potential FHA issues before you even make an offer.

Does a passed FHA appraisal guarantee the home is in perfect condition?

Absolutely not. This is a dangerous misconception. An FHA appraisal is not a substitute for a comprehensive home inspection. The appraiser's job is to check for compliance with a specific list of minimum standards. They are not performing a deep dive into the home's condition.

A professional home inspector will spend several hours examining hundreds of components of the house, from the plumbing and electrical systems to the appliances and insulation. They may uncover significant issues that are not on the FHA appraiser's checklist but could cost you thousands of dollars down the road. Even if a property passes the FHA appraisal with flying colors, you should always invest in a separate, detailed home inspection from a qualified inspector. Navigating FHA appraisal requirements in Tampa can be complex. If you have questions about a specific property or want to ensure your financing is secure, a mortgage expert can help you understand your options and prepare for a successful closing.

Navigating FHA appraisal requirements can be tricky, but it shouldn't stand in the way of your Tampa home purchase. If you're ready to secure your financing with confidence and want expert guidance through every step, our team is here to help. Take the first step toward a successful closing and Apply now.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

HUD FHA Single Family Housing Policy Handbook 4000.1

CFPB - What is a home appraisal, and what do I need to know?