Does Creating an S-Corporation Restart My Two-Year History?

This is the single biggest fear for self-employed borrowers in California, and the answer is a relieving 'no', provided you handle the transition correctly. Mortgage lenders are required to verify a minimum of two years of stable, predictable income. When you switch from a sole proprietorship to an S-Corporation, they don't see you as starting a brand-new venture. Instead, they view it as a change in the legal structure of an existing, ongoing business.

The key concept for underwriters is continuity. As long as you can prove that the S-Corporation is a direct continuation of the sole proprietorship, your history remains intact. The burden of proof is on you, the borrower, to connect the dots for the lender with clear and concise documentation.

What Lenders Consider Continuity

To satisfy an underwriter, the business must demonstrate consistency across three core areas:

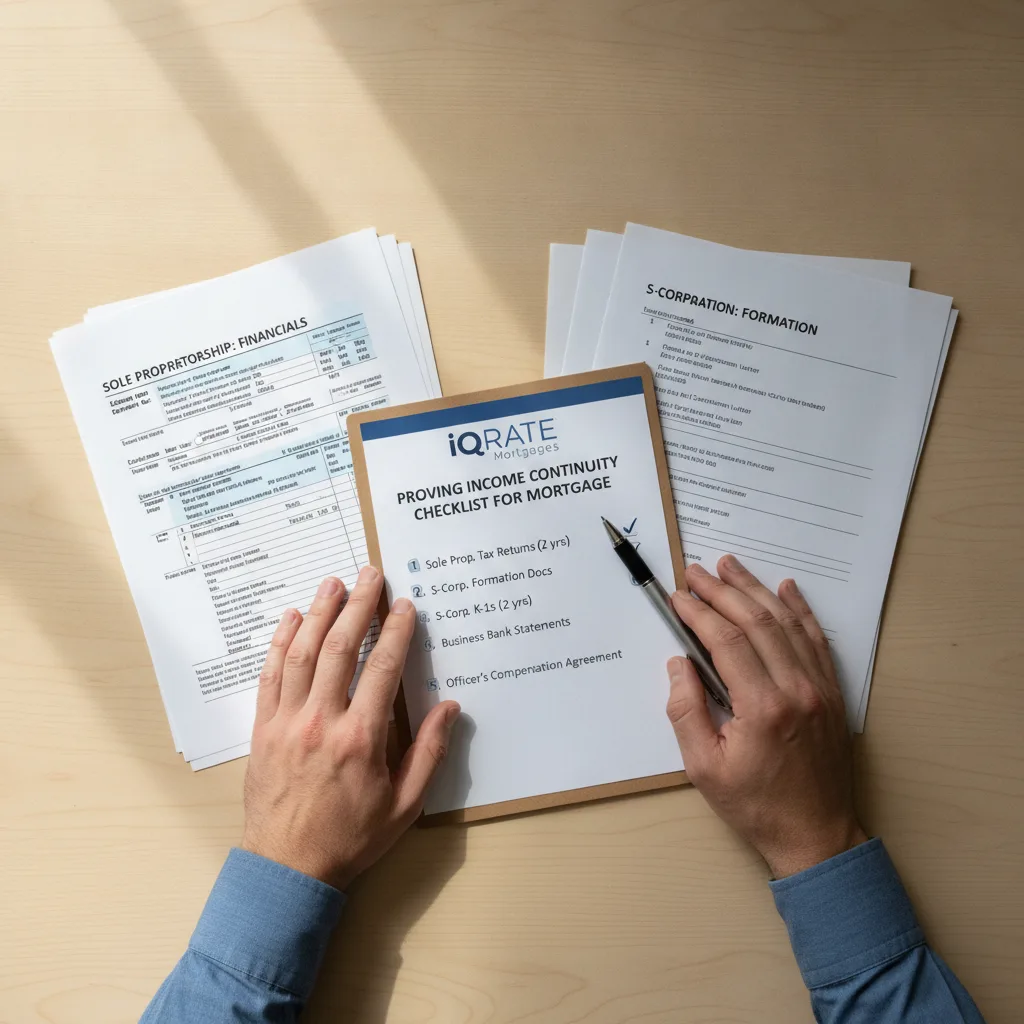

How to Document Your Income During the Transition

Flawless documentation is non-negotiable. Your goal is to present a paper trail so clear that the underwriter can easily follow your income from the old entity to the new one. Haphazard records can lead to delays or even denial. You will need to provide more paperwork than a standard W-2 employee.

Here is a checklist of the essential documents you'll need to gather:

What Underwriters Look For to See Income Continuity

Underwriters are trained to identify risk. When they see a change in business structure, their primary objective is to confirm that the income is just as stable as it was before. They are looking for a seamless financial story.

Key Green Flags for Underwriters:

Should I Wait to Apply for a Mortgage After Changing Entities?

There is no universal rule, but strategy is the key. Applying immediately after forming an S-Corp is possible if your documentation is impeccable and your income is strong. However, waiting can sometimes make the process smoother.

Ultimately, the decision depends on your financial stability, the quality of your records and your urgency. Consulting with a mortgage advisor who specializes in self-employed borrowers can help you time your application perfectly.

How Lenders Calculate Your New Salary and Distributions

Lenders will use a combination of your W-2 salary and the net distributable income from the S-Corporation to determine your qualifying income. They will average this income over a 24-month period, looking at both the old and new business structures.

Here’s a simplified example:

The Lender's Calculation:

This is your qualifying monthly income for the mortgage. Important note: If your income declined from Year 1 to Year 2, the lender would likely use the lower, more recent income as the basis for their calculation to be conservative.

Providing Tax Returns for Both Old and New Businesses

Yes, this is mandatory. You cannot simply provide your new S-Corp returns and expect approval. The lender must analyze a full 24-month period to meet federal lending guidelines. The final Schedule C from your sole proprietorship establishes the income baseline, and the new 1120-S and K-1 demonstrate that the income continued after the legal change. Think of it as two halves of one continuous story. Omitting one half leaves the underwriter with an incomplete picture, and no choice but to deny the loan.

Is a Bank Statement Loan a Better Option in This Scenario?

A bank statement loan can be an excellent alternative for some self-employed borrowers. Instead of analyzing tax returns, these non-QM (Non-Qualified Mortgage) loans use 12 or 24 months of business bank statements to verify income. They calculate your qualifying income based on the average monthly deposits.

When a Bank Statement Loan Makes Sense:

The Trade-Offs: Bank statement loans typically require a larger down payment (often 20% or more) and come with higher interest rates compared to conventional loans. (The data, information, or policy mentioned here may vary over time.) However, for a business owner in Long Beach looking to buy now, they offer a viable and powerful financing solution.

Partnering with Your Accountant for a Smoother Application

Your accountant is a key player on your home-buying team. Proactive communication with them is crucial. Before you apply for a mortgage, sit down with your CPA and discuss these points:

When you're ready to put this knowledge into practice, the next step is getting a clear view of your options. A carefully prepared application makes all the difference for self-employed professionals. Apply now to begin the pre-approval process with confidence.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

Consumer Financial Protection Bureau (CFPB): Explore the mortgage process