A Listing Agent's True Liability When a Buyer's Loan Fails

When you advise a seller to accept an offer, you are putting your professional judgment on the line. In the fast-paced real estate markets of Las Vegas and Henderson, the pressure to get a home under contract is immense. However, if that contract collapses because the buyer's financing fails, the consequences extend far beyond a delayed sale. Your liability as a listing agent is real, tangible, and can have lasting damage.

First, there's the immediate financial loss: your commission. Weeks of work, marketing dollars, and time are vaporized. But the more significant damage is to your reputation. The seller, who took their home off the market, packed boxes, and made plans based on your guidance, will hold you accountable. Their trust is broken, and negative word-of-mouth in a tight-knit community can be devastating.

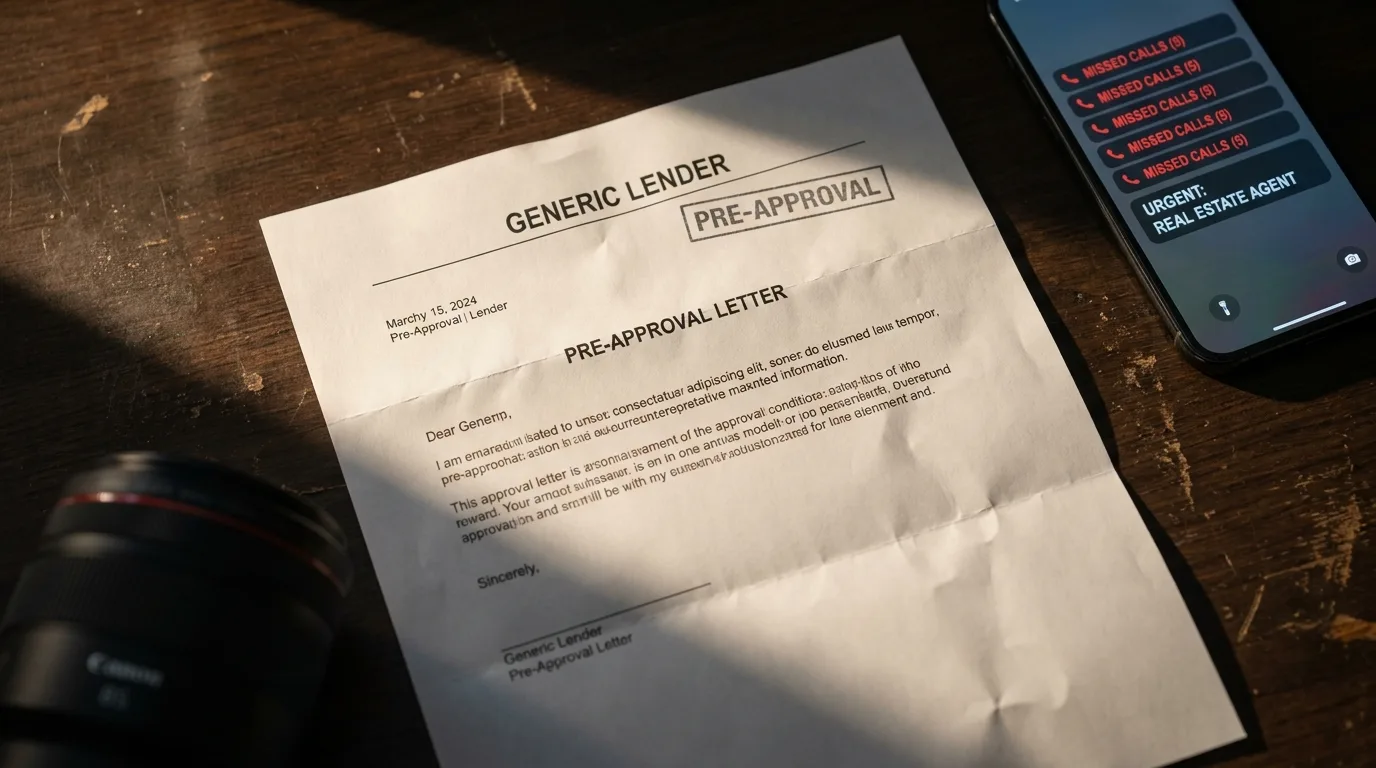

Consider this scenario: you list a desirable single-family home in Henderson. You receive multiple offers and advise your client to accept one that is slightly over asking price, backed by a standard pre-approval letter. Your seller cancels further showings. Three weeks later, deep into escrow, you get the call: the buyer's loan was denied. The lender's underwriter discovered undisclosed debt that torpedoed their debt-to-income ratio. Now, the seller has lost a month of valuable market time, and the other interested buyers have moved on. They are angry, and they are looking at you. This isn't just a failed deal; it's a potential claim of negligence against you for not performing adequate due diligence on the buyer's financial capacity.

Why Standard Pre-Approval Letters Are Insufficient Diligence

A pre-approval letter has become a standard part of an offer package, but it has been dangerously devalued. Many agents and sellers view it as a guarantee of financing, which it is not. A typical pre-approval is often a superficial check, not a thorough financial examination.

Here’s what a standard pre-approval usually entails:

- A Cursory Credit Check: The lender pulls a credit report to see the buyer's score and basic history.

- Stated, Unverified Income: The loan officer asks the buyer how much they make and plugs that number into a calculator. They rarely verify it with pay stubs or tax returns at this stage.

- Stated, Unverified Assets: The buyer states they have funds for a down payment, but the source and availability of those funds have not been documented with bank statements.

Essentially, a pre-approval is a loan officer's opinion based on unverified information. It's an algorithm's best guess, not a commitment to lend. It fails to account for countless deal-killing variables that only a human underwriter can uncover, such as employment gaps, irregular commission-based income, undisclosed alimony or child support payments, or down payment funds coming from an unacceptable source. Relying on this document alone as your diligence is like a home inspector only looking at the paint color. You are failing to look beneath the surface, and that failure constitutes a breach of your professional duty.

Creating a Defensible Standard of Care for Vetting Offers

To protect yourself, your commission, and your clients, you must adopt a higher standard of financial vetting. This is 'defensible diligence': a documented process that proves you took reasonable and professional steps to verify an offer's financial strength. It moves beyond the flimsy pre-approval and demands concrete evidence.

The Core Documents You Need

When you receive an offer, your acceptance should be conditioned on reviewing a more robust financial package. While you won't see every detail, you have the right to ask the buyer's agent for proof that a lender has thoroughly vetted their client. This includes confirmation that the lender has reviewed:

- Fully Executed Uniform Residential Loan Application (Form 1003): This is the buyer's formal application, detailing their income, assets, and liabilities.

- Credit Report with All Three Scores: Confirms the lender is working with a complete credit picture.

- Two Most Recent Pay Stubs: Verifies current employment and income.

- Last Two Years of W-2s or Tax Returns: Provides income history and stability.

- Two Most Recent Bank Statements: Documents the source and availability of funds for the down payment and closing costs.

- A Conditional Loan Approval or Underwriting Summary: This is the key document. It's a statement from the lender that a human underwriter has reviewed the entire file and issued an approval, pending only title, appraisal, and final conditions.

The Power of Documented Communication

Your diligence doesn't stop with paperwork. You must have a direct, documented conversation with the buyer's loan officer. An email is better than a phone call for creating a paper trail. Ask probing questions and save their written responses. This documentation is your evidence that you went beyond the surface level to protect your seller's interests.

Fully Underwritten Approval vs. Typical Pre-Qualification

It is critical that you and your seller understand the hierarchy of financial vetting. These terms are often used interchangeably, but they represent vastly different levels of certainty.

Pre-Qualification: This is the weakest assurance. It's often a 10-minute phone call where a buyer self-reports their financial information. No documents are reviewed, and no credit is pulled. A pre-qualification is effectively worthless in a competitive negotiation.

Standard Pre-Approval: As discussed, this is a step up but still insufficient. It involves a credit pull and a loan officer's review of stated income and assets. The file has not been seen by the person who makes the final decision: the underwriter.

Fully Underwritten Approval (Conditional Approval): This is the gold standard. The buyer has submitted a full application and all supporting documentation (pay stubs, W-2s, bank statements). An actual underwriter has meticulously reviewed the entire file and issued an approval. The only remaining conditions are typically property-related, such as a satisfactory appraisal and clean title report. An offer with an underwritten approval is nearly as strong as a cash offer.

Presenting these options to your seller clarifies that you are not just looking at offer price, but at the certainty of closing.

Explaining a Higher Vetting Standard to Your Seller

Your clients hire you for your expertise and protection. Framing this rigorous process as a key part of that protection is essential. Avoid overly technical jargon and focus on the benefit to them.

Here's a sample script you can adapt:

'Mr. and Mrs. Seller, we have three offers on your Las Vegas home. Offer A is the highest price, but it comes with a basic pre-approval letter. Offers B and C are slightly less, but they have provided proof that their lender's underwriter has already approved their loan. In this market, the biggest risk is a deal falling apart in escrow. The pre-approval for Offer A is based on unverified information and is not a guarantee. The underwritten approvals for B and C are. By choosing a fully vetted buyer, we dramatically reduce the risk of going back on the market in 30 days. The certainty of closing is often more valuable than a few extra thousand dollars.'

Critical Questions to Ask a Buyer's Lender

When you call or email the buyer's loan officer, don't ask, 'Is your borrower solid?' You will always get a 'yes'. You need to ask specific, surgical questions that expose potential weaknesses.

- 'Has a human underwriter personally reviewed the buyer's complete file, including the 1003, credit, income, and asset documentation?'

- 'Can you please confirm you have copies of the last two pay stubs, two years of W-2s, and two months of bank statements?'

- 'Have you sourced and verified the funds for the down payment and closing costs, and are they in the buyer's account now?'

- 'Based on the underwriter's review, are there any outstanding borrower-related conditions that could jeopardize the final approval?'

- 'What is the buyer's debt-to-income ratio as calculated by the underwriter, and does it meet the guidelines for this specific loan program?' (The data, information, or policy mentioned here may vary over time.)

A loan officer who can confidently and quickly answer these questions is likely managing a well-vetted file. Hesitation or vague answers are major red flags.

Strengthening Your Seller's Negotiating Position in Las Vegas

When you can demonstrate that you have multiple offers and are prioritizing those with proven financial strength, you gain immense negotiating leverage. You're not just negotiating on price; you're negotiating on certainty.

Imagine a bidding war for a property in a sought-after Henderson neighborhood. You can go back to the bidders and state, 'We are giving preferential consideration to offers that can provide an underwriting summary or conditional loan approval. This will be a primary factor in the seller's decision.' This move forces buyers to get serious with their lenders, weeding out those who are not truly prepared. It allows your seller to be firm on their price and terms because they are negotiating from a position of power, knowing the chosen buyer is highly likely to close.

Reducing Your Errors and Omissions (E&O) Insurance Risk

Every real estate agent carries E&O insurance to protect against claims of negligence. Your annual premium is based on your perceived risk. A documented history of failed contracts where buyer financing was the cause can be a red flag for insurers.

By implementing a defensible diligence protocol, you are creating a clear, documented record of your professionalism and standard of care. If a seller ever tries to claim you were negligent in vetting a buyer, you can produce the file: the underwriting summary you requested, your email correspondence with the lender, and your notes explaining the financial strength of the accepted offer. This documentation is your best defense. It demonstrates that you acted not just on an industry-standard practice (accepting a pre-approval) but on a higher, more defensible standard. This proactive risk management can be a favorable factor for your E&O provider and, more importantly, can be the evidence that protects your license and livelihood in a dispute. Protect your clients and your business. The next time you receive an offer, insist on a higher standard of financial proof. For guidance on what that looks like, let's connect and discuss how to implement a defensible diligence protocol in your practice.

Ready to present an offer that sellers will take seriously? Start with a fully vetted, defensible loan approval. Apply now to gain a competitive edge in any market.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

CFPB - The closing process: a step-by-step guide for homebuyers and sellers