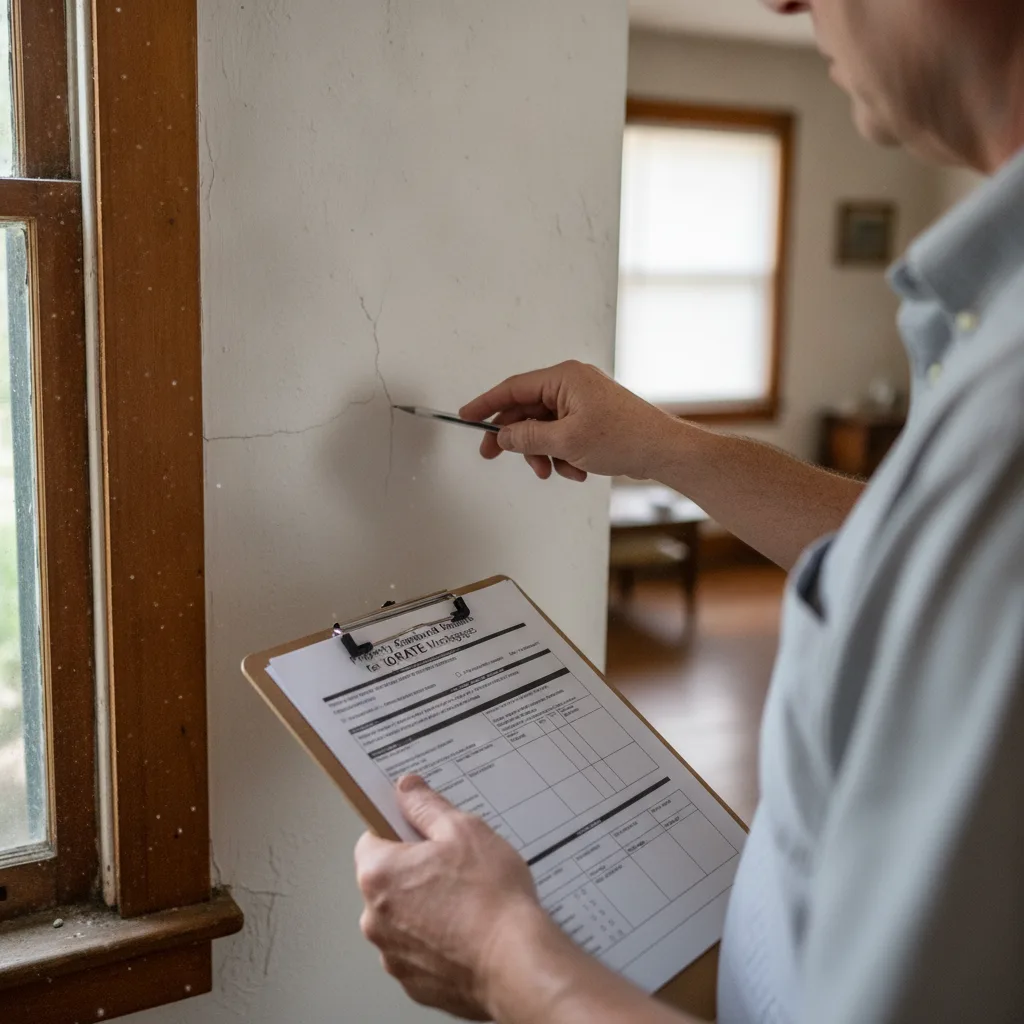

What are Federal Housing Administration Minimum Property Standards?

When you use an FHA loan to buy a home, the property isn't just being evaluated for its market value; it's being inspected to ensure it meets specific health and safety standards set by the U.S. Department of Housing and Urban Development (HUD). These are known as Minimum Property Standards (MPS). The core principle behind them is to protect the borrower from buying a deficient home and to protect the FHA, which insures the loan against default.

The standards are often summarized by the 'Three S’s':

- Safety: The property must be free from hazards that could endanger the occupants. This includes issues like exposed wiring, missing handrails on stairs, and significant structural defects.

- Security: The home must be a secure dwelling. This relates to the overall structural integrity, the quality of the foundation, and ensuring the home protects its inhabitants from the elements.

- Soundness: The property must be in good repair, with no conditions that could jeopardize its structural integrity. This means the appraiser is looking for things like a failing roof, significant water damage, or evidence of termite infestation.

Unlike a standard home inspection, which is for the buyer's information, an FHA appraisal is for the lender. If the appraiser notes MPS violations, those issues must be repaired before the loan can close.

Which Appraisal is Stricter for an Older Tampa Home: FHA vs Conventional?

For an older home in a market like Tampa, the FHA appraisal is unequivocally stricter than a conventional loan appraisal. This is the single most important distinction for buyers to understand.

An FHA appraiser is required to view the property through the lens of HUD's Minimum Property Standards. They operate with a detailed checklist, looking for specific health and safety issues that a conventional appraiser might only note as part of the home's overall condition. For example, peeling paint on a home built before 1978 is an automatic red flag for an FHA appraiser due to the potential for lead-based paint, but a conventional appraiser might simply see it as a cosmetic flaw that affects value.

Conventional loans are not government-insured; they are typically bought by Fannie Mae or Freddie Mac. While these entities also have standards for property condition, their focus is primarily on the home's marketability and value as collateral. A conventional appraiser is mainly concerned with identifying issues that significantly detract from the property's value or pose a major structural or safety risk. They have more discretion and are generally more lenient on minor, non-structural, and cosmetic defects.

What Specific Property Conditions Will Fail an FHA Appraisal in Orlando?

When looking at charming but older homes in neighborhoods across Orlando, an FHA-financed offer can be quickly complicated by the appraisal. An FHA appraiser is trained to identify and flag specific conditions that must be remedied before closing. Here are some of the most common deal-breakers:

- Peeling or Chipping Paint: In any home built before 1978, any surface with peeling, chipping, or flaking paint—inside or out—must be scraped and repainted. This is a non-negotiable lead-based paint hazard protocol.

- Roof Condition: The roof must have a remaining economic life of at least two years. If it's covered in moss, has multiple layers of shingles, or shows clear signs of active leaks, it will be flagged for repair or replacement.

- Electrical and Plumbing Systems: Outdated systems like knob-and-tube or fuse-box electrical panels are often flagged as safety hazards. Leaky plumbing or a water heater that doesn't meet local code will also be called out.

- Inadequate Heating: The home’s primary heating system must be operational and capable of providing adequate heat for the living space.

- Structural and Foundation Issues: Any signs of significant foundation cracking, rotting wood on porches or window sills, or evidence of active termite damage will result in a failed appraisal pending major repairs.

- Safety Features: Missing handrails on staircases (typically with more than three steps), broken windows, or lack of proper ventilation in crawl spaces or attics are common FHA repair requirements.

Are Conventional Loan Appraisers More Lenient on Cosmetic Issues?

Yes, absolutely. This is where the flexibility of a conventional loan shines, especially for homes that are structurally sound but cosmetically dated. A conventional appraiser's primary goal is to determine an accurate market value for the property. They will note cosmetic issues like worn carpeting, dated kitchen cabinets, or scuffed walls, but they typically factor these into the overall value rather than requiring them to be fixed as a condition of the loan.

Here's a practical example:

- Scenario: An older Orlando home has a few cracked windowpanes and peeling paint on an exterior shed.

- FHA Appraisal: The appraiser will likely require the windows to be replaced and the shed to be scraped and repainted ('subject-to' conditions) before the loan can close. These are seen as safety (broken glass) and soundness (paint) issues.

- Conventional Appraisal: The appraiser will note the condition of the windows and shed in the report, possibly adjusting the home's appraised value downward slightly to reflect the needed repairs. However, it is highly unlikely they would require these specific items to be fixed before closing.

This leniency gives buyers using conventional loans a significant advantage, allowing them to purchase a home with cosmetic flaws and address them on their own timeline and budget.

What Happens If the Home I Want Fails the FHA vs Conventional Appraisal?

Facing a failed appraisal can be stressful, but the process and outcomes differ significantly between FHA and conventional financing.

If an FHA Appraisal Fails:

- Repair List Issued: The appraiser provides a list of 'subject-to' repairs that must be completed to meet HUD's Minimum Property Standards.

- Negotiation: The buyer and seller must negotiate who will pay for and complete the repairs. Sellers of 'as-is' properties are often unwilling to do this.

- Repairs Completed & Re-inspected: Once work is done, the appraiser must return to the property to verify completion and sign off.

- The Appraisal Sticks: A critical point—the FHA case number and the appraisal, including the required repairs, 'stick' to the property for 120 days. This means any other buyer attempting to use an FHA loan during that time will be subject to the same appraisal and repair list.

If a Conventional Appraisal Fails:

- Value Comes in Low or 'Subject-to' Repairs: The appraiser might determine the value is lower than the purchase price due to condition, or they may flag a major safety/structural issue (e.g., a failing foundation) that must be repaired.

- More Flexibility: There is more room for negotiation. The buyer and seller can renegotiate the price, arrange for a seller credit for repairs, or the buyer can cancel the contract (if they have an appraisal contingency).

- Switching Lenders is an Option: The conventional appraisal is specific to that lender. While another lender would also require an appraisal, a different appraiser might view the property's condition differently.

- No 'Sticking' Period: The appraisal does not prevent another buyer from getting a different conventional loan appraisal immediately.

Can I Use a Renovation Loan If the Property Needs Significant Repairs?

Yes. Renovation loans are an excellent solution for buying a home that won't pass a standard appraisal. They allow you to finance the purchase of the home and the cost of the necessary repairs or desired upgrades into a single mortgage.

- FHA 203(k) Loan: This is the FHA's dedicated renovation loan. The Limited 203(k) is for non-structural repairs up to $35,000, perfect for things like replacing a roof, updating a kitchen, or painting. The Standard 203(k) is for major projects, including structural work, and requires a HUD consultant to oversee the project.

- Fannie Mae HomeStyle® Loan: This is a conventional renovation loan. It can be used for almost any renovation, from cosmetic updates to luxury additions like a swimming pool, and isn't restricted by the FHA's specific property standards once the work is complete. It often requires a higher credit score and down payment than an FHA 203(k). (The data, information, or policy mentioned here may vary over time.)

How Do Sellers View Offers with These Different Loan Types?

In a competitive market like Tampa, sellers often view conventional loan offers more favorably than FHA offers, especially on older properties. This perception is rooted in the strictness of the FHA appraisal process.

Sellers and their agents know that an FHA appraisal can introduce delays, unexpected repair costs, or even kill the deal entirely. An offer with conventional financing signals a potentially smoother, faster closing with fewer appraisal-related hurdles. For a seller marketing their home 'as-is', a conventional or cash offer is almost always preferred because it shifts the risk of the home's condition to the buyer.

Which Loan is Better for a Home That Might Have Unpermitted Work?

Unpermitted work is a red flag for any type of financing, but it can be a particularly difficult obstacle for an FHA loan. FHA appraisers are trained to assess whether the home's layout matches public records and if all additions appear to be of professional quality. If an appraiser suspects unpermitted work that poses a safety or structural risk, they must call it out and may require retroactive permits or demolition as a condition for the loan.

A conventional appraiser also cares about safety and soundness, but their primary focus is on marketability. If the unpermitted work is common for the area and doesn't pose an obvious hazard (like a well-built patio enclosure), they may simply note it in the report without requiring a specific action. Therefore, a conventional loan often provides a slightly higher chance of successfully financing a home with minor, non-hazardous unpermitted work, although it is never guaranteed. Choosing between FHA and conventional financing for an older Florida home is a strategic decision that goes beyond the interest rate. To ensure you're positioned for a successful purchase, it's vital to speak with a mortgage expert who understands the nuances of property appraisals. A consultation can help you select the loan that best fits the home's condition and strengthens your offer.

Ready to navigate the complexities of FHA and conventional appraisals for your dream home? Take the next step and Apply for a Mortgage to see which financing option best fits your situation.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

HUD Handbook 4000.1 (FHA Single Family Housing Policy Handbook)

Fannie Mae Selling Guide: Property Condition and Quality

Consumer Financial Protection Bureau (CFPB) - The Home Appraisal Process