What are the total closing costs for a Veteran Affairs IRRRL loan?

The primary appeal of a Veteran Affairs (VA) Interest Rate Reduction Refinance Loan (IRRRL), often called a 'streamline refinance', is its simplicity. However, 'simple' does not mean 'free'. While these loans are designed to be low-friction, they still come with closing costs that can significantly impact your potential savings.

Key costs associated with a VA IRRRL include:

- VA Funding Fee: This is a mandatory fee paid to the VA to help fund the loan program. For an IRRRL, it is a flat 0.5% of the loan amount for all veterans, regardless of service history or down payment. This is a significant reduction from the funding fee on a first-time VA purchase loan.

- Lender Origination Fee: This charge covers the lender's administrative costs for processing and underwriting your loan. It's often capped by the VA at 1% of the loan amount, but you should always confirm the exact figure.

- Title Insurance and Escrow Fees: While an IRRRL reuses your original VA entitlement, a new title search and policy are often required by the lender to protect their interest. Escrow fees cover the third party that handles the closing paperwork and funds.

- Recording Fees: These are fees paid to your local county, such as Duval County for Jacksonville or St. Johns County for St. Augustine, to officially record the new mortgage lien against your property.

- Discount Points: These are optional fees you can pay upfront to 'buy down' your interest rate. One point typically costs 1% of the loan amount and might lower your rate by 0.25%, though the exact reduction varies.

In total, you can expect closing costs for a VA IRRRL in Florida to range from $3,000 to $6,000, depending on your loan amount and the specific fees charged by your lender. (The data, information, or policy mentioned here may vary over time.)

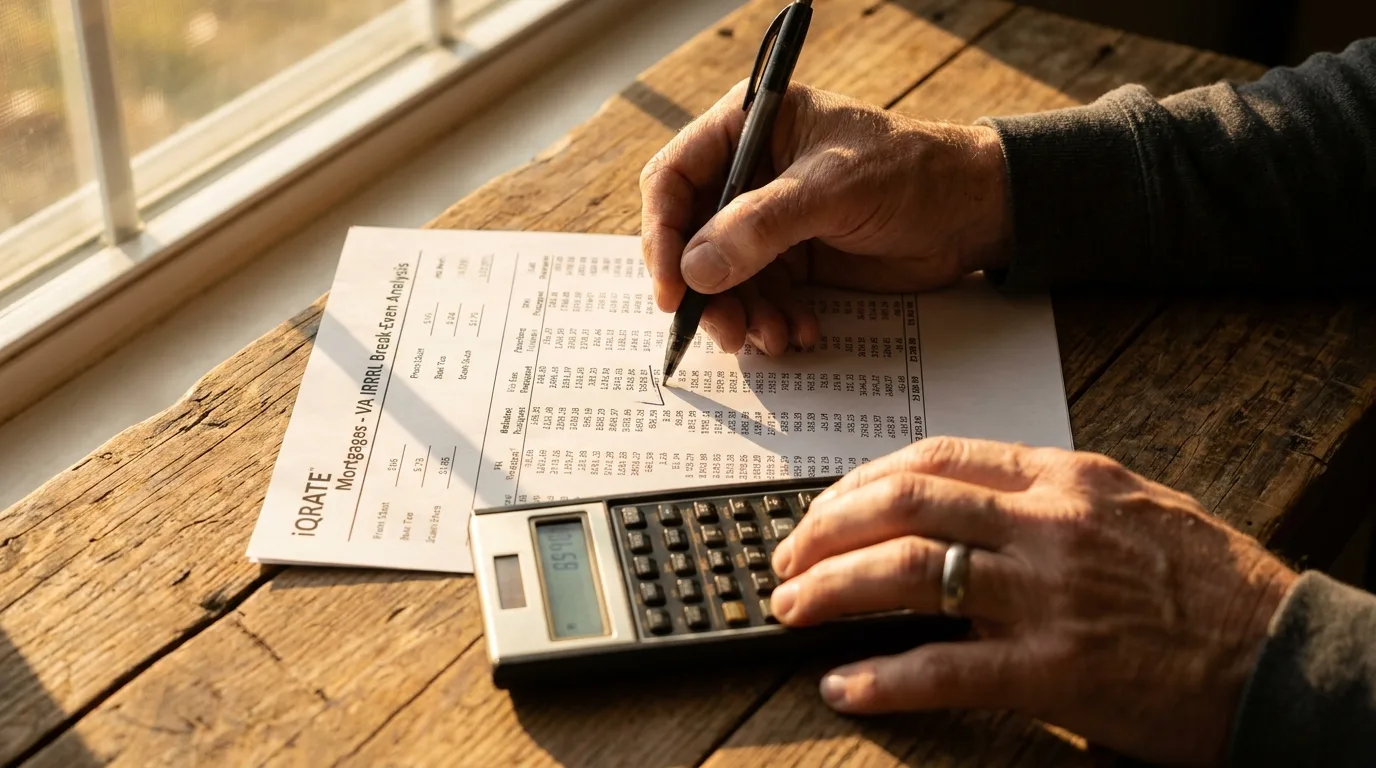

How do I calculate the break-even point on a refinance in Jacksonville?

The break-even point is the single most important calculation to determine if an IRRRL is a financially sound decision. It tells you the exact number of months it will take for your accumulated monthly savings to cover the total closing costs. If you sell the home before you reach this point, you will have lost money on the refinance.

The formula is straightforward:

Total Closing Costs / Monthly Savings = Months to Break Even

Let's use a realistic Jacksonville example:

- Original Loan Amount: $350,000

- Original Interest Rate: 6.5% (Principal & Interest: $2,212)

- New Interest Rate Offer: 5.5% (Principal & Interest: $1,987)

- Monthly Savings: $2,212 - $1,987 = $225

- Total Closing Costs (including VA Funding Fee): $5,400

Now, let's calculate the break-even point:

$5,400 / $225 = 24 months

In this scenario, it would take you exactly two years to recoup the costs of the refinance. If you plan to live in your Jacksonville home for five more years, this is a fantastic deal. However, if you have orders to relocate in 18 months, this IRRRL would be a financial mistake.

When does financing the Veteran Affairs funding fee make sense?

The VA allows you to roll the 0.5% funding fee and other closing costs into your new loan balance. This is a popular option as it eliminates the need to bring cash to closing.

Financing the funding fee makes sense if:

- You lack the liquid cash to pay the costs upfront without straining your budget.

- You are confident you will stay in the home long past the break-even point. The convenience of no-cash-out-of-pocket is beneficial if your long-term savings will far exceed the added interest.

Financing the fee does not make sense if:

- You are trying to maximize equity. Rolling costs into the loan increases your principal balance, which means you are paying interest on those fees for the life of the loan.

- Your timeline in the home is uncertain. If there's a chance you might move close to the break-even date, paying costs in cash lowers your break-even point and reduces your risk.

Using our Jacksonville example, financing the $5,400 in costs would increase the new loan amount to $355,400. While this may only increase the monthly payment slightly, it adds to the total interest paid over the long run.

Can a lender in St. Augustine offer a true zero cost streamline refinance?

Yes, lenders in St. Augustine and across Florida offer 'no-cost' or 'zero-cost' IRRRLs, but it's crucial to understand the trade-off. There is no such thing as a free loan; the costs are simply paid for in a different way.

In a 'zero-cost' refinance, the lender covers your closing costs. In exchange, they will offer you a slightly higher interest rate than you would get if you paid the costs yourself. This is known as a 'lender credit'.

Example Comparison in St. Augustine:

- Option A (Pay Costs): 5.5% interest rate with $5,400 in closing costs. Monthly P&I: $1,987.

- Option B (Zero-Cost): 5.875% interest rate with $0 closing costs. Monthly P&I: $2,077.

While Option B requires no cash, the monthly payment is $90 higher. Over five years, you would pay an extra $5,400 ($90 x 60 months) compared to Option A. The 'zero-cost' loan is more expensive in the long term but provides immediate relief by avoiding upfront fees.

What questions should I ask about my mortgage interest rates today?

When you receive an IRRRL offer, the advertised interest rate is only part of the story. To understand the true cost, you must ask targeted questions. Arm yourself with this list before speaking to a lender:

- 'What is the Annual Percentage Rate (APR)?' The APR includes the interest rate plus most of the fees, providing a more accurate measure of the loan's cost.

- 'Does this interest rate quote include any prepaid discount points?' An unusually low rate may be propped up by thousands of dollars in points, which will drive up your break-even point.

- 'Could you please provide a detailed Loan Estimate?' This standardized document itemizes every single charge, from the origination fee to the title costs. Do not proceed without it.

- 'Is this a fixed interest rate?' While most IRRRLs are fixed-rate, you need to confirm you are not being quoted an adjustable-rate mortgage (ARM) by mistake.

Is it better to shorten my loan term or lower my payment?

An IRRRL offers an opportunity to change your loan's structure. Your primary goal will determine the best path forward.

Goal: Lower My Monthly Payment

If your main objective is to improve your monthly cash flow, refinancing to a lower rate while keeping the same loan term (or even restarting a 30-year term) is the best strategy. This provides the maximum reduction in your monthly housing expense.

Goal: Shorten My Loan Term

If your budget can handle a similar or slightly higher payment, refinancing from a 30-year VA loan into a 15-year VA loan can save you a massive amount of interest over the life of the loan and help you build equity much faster. The interest rates on 15-year mortgages are also typically lower than those for 30-year terms.

Ultimately, this is a personal financial decision based on your short-term budget needs versus your long-term wealth-building goals.

How does my home equity impact my refinance options?

For a standard VA IRRRL, your home's equity position has minimal impact. One of the key benefits of the streamline program is that no appraisal is typically required. This means that even if your home's value has decreased and you owe more than it's worth, you can still be eligible to refinance to a lower rate.

The lender's primary concern is that you have a history of on-time payments on your current VA loan and that the refinance provides a tangible benefit, such as a lower monthly payment.

However, if you have significant equity, it opens up other possibilities. You may want to consider a VA Cash-Out Refinance instead, which would allow you to tap into that equity to pay off debt or fund home improvements.

Are there alternatives to an Interest Rate Reduction Refinance Loan?

Yes, while the IRRRL is the most common refinance option for veterans, it is not the only one.

- VA Cash-Out Refinance: As mentioned, this is for veterans who want to take cash out of their home's equity. It requires a new appraisal and has different credit and income underwriting requirements. The funding fee is also higher than for an IRRRL.

- Conventional Refinance: If you have at least 20% equity in your home and a strong credit profile, a conventional refinance could be a viable option. The main advantage is that there is no funding fee. You could potentially secure a lower overall cost if the interest rate is competitive with VA offers.

Comparing a conventional loan offer against a VA IRRRL, especially regarding the total fees and APR, is a smart move for any financially savvy veteran in Jacksonville or St. Augustine. Understanding the nuances of a VA IRRRL can be complex. If you want a clear breakdown of the costs, benefits, and break-even point for your specific situation in Jacksonville or St. Augustine, a detailed analysis from an expert can provide the clarity you need to make the right decision.

Ready to find out your break-even point and potential savings? A personalized analysis of an IRRRL can provide the clarity you need. Apply now to explore your options.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.