Can a Lender Cancel My VA Loan in San Diego If My Orders Change?

Receiving Permanent Change of Station (PCS) orders while in escrow on a home in San Diego or Oceanside is a stressful but manageable situation. A lender will not automatically cancel your VA loan, but they are required to re-evaluate it based on one critical factor: occupancy. The foundation of the VA loan program is that the property will be your primary residence.

When your duty station changes, your ability to occupy the home comes into question. If you receive orders to move from San Diego to a base across the country, you can no longer personally fulfill this requirement. In this case, the lender can deny the loan because it no longer meets VA guidelines. However, this is not a punitive action. Lenders who specialize in VA loans understand the realities of military life and will work with you to determine the next steps. The decision hinges on whether you can still meet the occupancy rules through an exception, such as your spouse residing in the home.

How Can I Protect My Earnest Money Deposit If I Get New PCS Orders?

Your most powerful tool for protecting your earnest money deposit (EMD) is the military clause in your purchase agreement. This is a contingency specifically designed to protect service members from financial loss due to unforeseen military obligations. Without this clause, canceling the contract could put your deposit, which can be thousands of dollars, at risk of forfeiture to the seller. (The data, information, or policy mentioned here may vary over time.)

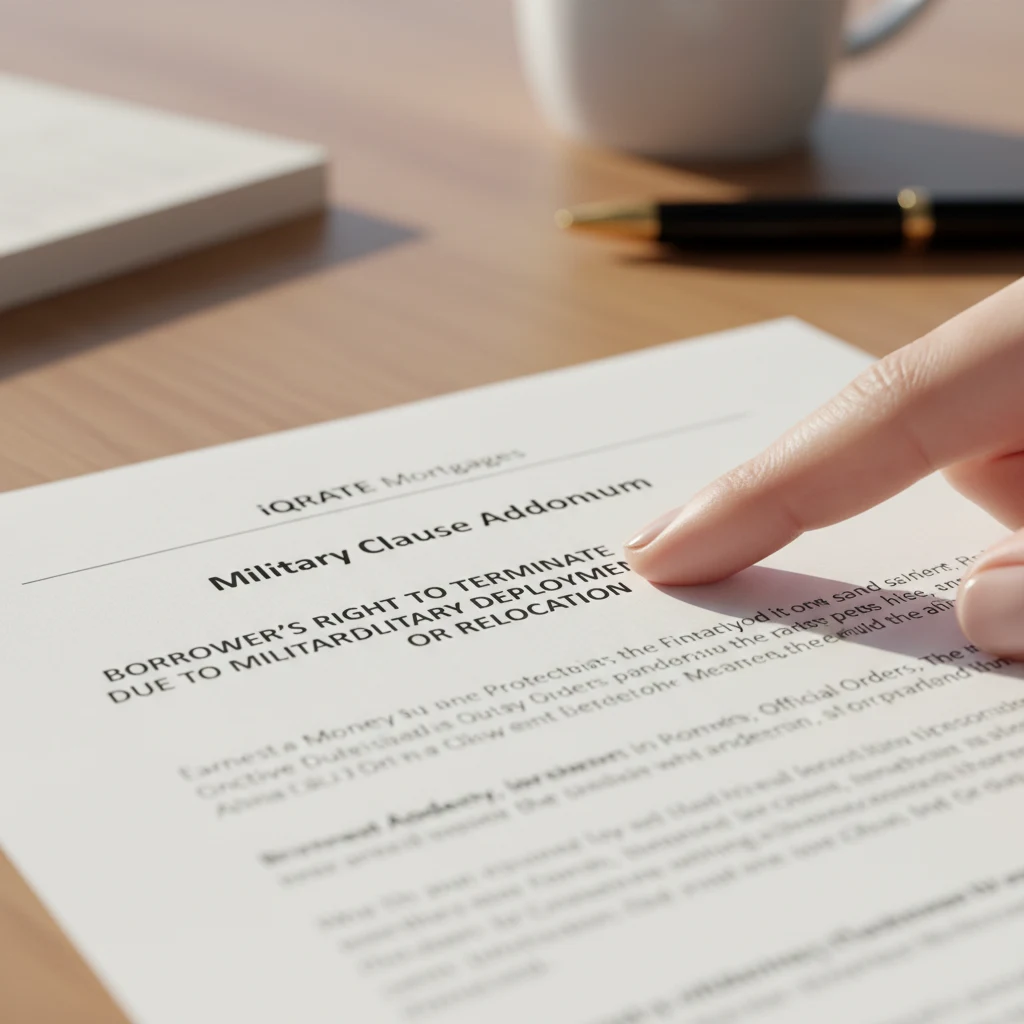

Understanding the Military Clause in Your Purchase Agreement

When you make an offer on a home in Oceanside, your real estate agent should include a military clause in the contract. This clause allows you to terminate the agreement without penalty if you receive official orders that prevent you from completing the purchase. It essentially makes your home purchase contingent on your military station remaining stable through closing. If new PCS orders arrive, you can invoke this clause, cancel the contract, and receive a full refund of your earnest money. (The data, information, or policy mentioned here may vary over time.) It is crucial that this clause is included and properly worded from the very beginning of the transaction.

Does the Military Clause in My Purchase Contract Cover a Change of Orders?

Not all military clauses are created equal. The specific wording is critical. A generic clause may only cover deployments, not a change in duty station. A strong, protective military clause should explicitly mention 'Permanent Change of Station (PCS)' or 'reassignment to a new duty station'.

For example, a well-drafted clause for a home purchase in San Diego might state: 'This agreement is contingent upon the buyer's continued assignment at their current duty station through the close of escrow. Should the buyer receive official military orders requiring a Permanent Change of Station to a location more than 50 miles away from the property, the buyer may terminate this agreement in writing and all deposits shall be returned to the buyer.' (The data, information, or policy mentioned here may vary over time.)

Before signing any purchase contract, review this clause carefully with your real estate agent. Ensure it specifically covers a PCS scenario to provide the protection you need. If the language is vague, insist on an addendum that clarifies it.

Can My Spouse Satisfy the VA Occupancy Rule If I Have to Leave Oceanside?

Yes, and this is the most common way for a VA loan to proceed after the service member receives new PCS orders. The Department of Veterans Affairs has a significant exception to its personal occupancy rule. If you are on active duty and cannot personally occupy the home because of your military service, your spouse's occupancy can satisfy the requirement.

To make this work, you must inform your lender immediately. They will require a few things:

- A copy of your new PCS orders.

- A written statement confirming your spouse will reside in the property as their primary residence.

- Verification of financial stability. The lender will need to ensure that even with you living elsewhere, the household income is sufficient to manage the mortgage payment and other obligations.

If these conditions are met, the loan for your Oceanside home can continue to closing. This allows your family to establish roots and stability even if your duty station changes unexpectedly.

What to Do the Moment You Receive Updated PCS Orders Mid-Transaction

A methodical response is key to navigating this challenge without adding unnecessary stress. Follow these steps the moment you have official orders in hand:

- Read and Confirm Your Orders: Verify the report date and new location. Don't act on rumors; wait until you have the official, written orders.

- Contact Your Loan Officer Immediately: This is your first call. Explain the situation and provide them with a copy of your new orders. They will outline the lender's specific requirements and discuss whether proceeding with spousal occupancy is an option.

- Notify Your Real Estate Agent: Your agent is your advocate with the seller. They need to know about the orders to prepare for either invoking the military clause or communicating your intent to proceed with the purchase.

- Review Your Purchase Contract: Locate and read the military clause again. Understand the specific terms for termination and the timeline for providing notice. (The data, information, or policy mentioned here may vary over time.)

- Decide Your Path: Based on discussions with your family, loan officer, and agent, decide whether you will terminate the contract or move forward with your spouse occupying the San Diego property.

Can the VA Loan Be Transferred to a Property at My New Duty Station?

No, a VA loan cannot be transferred from one property to another. The entire loan application, including the appraisal, title search, and underwriting, is specific to the property you are under contract to buy in California. The VA appraisal, for instance, assesses the value and condition of that particular San Diego home, and its findings are not applicable to a property in another state.

If you decide to cancel your purchase in Oceanside and buy a home at your new duty station, you must start the mortgage process from the beginning. This involves finding a new property, signing a new purchase contract, and submitting a new loan application. While your credit report and some income documents may be reusable if the process is started quickly, a new appraisal and full underwriting review will be required for the new home.

How Do I Communicate a Change of Orders to My Lender and Real Estate Agent?

Clear, prompt, and formal communication is essential to protect your interests.

Notifying Your Loan Officer

Send an email to your loan officer with the subject line 'URGENT: Change in Military Orders - [Your Name] & [Property Address]'. In the email, state clearly that you have received new PCS orders and attach a full copy. Explain whether you intend to cancel the transaction or wish to explore proceeding with your spouse satisfying the occupancy requirement. This written record creates a clear timeline and ensures there is no miscommunication.

Notifying Your Real Estate Agent

Your real estate agent will manage the communication with the seller's agent. After you speak with them on the phone, follow up with an email. If you are canceling, they will draft the official termination notice, citing the military clause, and formally request the return of your earnest money deposit from the escrow holder. (The data, information, or policy mentioned here may vary over time.) Acting quickly is crucial, as your contract may have specific deadlines for providing such notice.

Will I Need to Start the Entire VA Loan Application Process Over Again?

The answer depends on your decision.

If you proceed with spousal occupancy for the San Diego home: You will not need to start over. The loan process continues. Your lender will likely ask for a letter of explanation and a copy of your new orders to add to the file, but the existing application, appraisal, and title work remain valid. The transaction proceeds toward the original closing date.

If you cancel the purchase and buy at your new duty station: You will need to start a new loan application. As mentioned, the loan is property-specific. While your lender may be able to use some recently pulled documents like credit reports and pay stubs to streamline the pre-approval for a new home, you will essentially be starting from square one with a new purchase contract, appraisal, and underwriting process for the new property. Navigating a VA loan during a PCS can be complex. If you're facing a change of orders while buying a home in San Diego or Oceanside, contact a mortgage specialist who understands the nuances of military life to explore your options and protect your homeownership goals.

Unexpected PCS orders don't have to disrupt your homeownership plans. Whether you're moving forward in San Diego or starting fresh at a new duty station, our specialists understand the demands of military life and are ready to help. Apply now for expert guidance tailored to your situation.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

VA Loan Occupancy Requirements - U.S. Department of Veterans Affairs

What is a military clause? - Consumer Financial Protection Bureau