Why Tax Returns Show Less Income Than You Actually Make

As a successful business owner in Florida, you work with a smart CPA to legally minimize your tax liability. You take advantage of every available deduction, from vehicle mileage and home office expenses to the depreciation of essential equipment. While this strategy is excellent for your bottom line, it creates a significant challenge when applying for a jumbo loan. The problem is that traditional mortgage underwriters base their initial income analysis on the Adjusted Gross Income (AGI) found on your tax returns. This number, after all your strategic deductions, often paints a picture of an income far lower than the actual cash flow your business generates.

Lenders are trained to look at the net income, not the gross revenue. This discrepancy is the single biggest hurdle for self-employed professionals seeking luxury properties in markets like Miami, Naples, or Palm Beach. Your tax returns are designed to show the IRS the least amount of income legally possible, while your mortgage application needs to show a lender the most income realistically available to comfortably afford your payments.

Let's consider a realistic example. Imagine you are a marketing consultant operating as an S-Corporation. Your business grossed $850,000 last year. After paying for software, contractors, marketing, and other operating costs, you also deducted:

- $40,000 in equipment depreciation (computers, servers).

- $10,000 in business mileage.

- $15,000 for the business use of your home.

- $25,000 in one-time software development costs.

After all these valid deductions, your personal tax return might show a taxable income of only $250,000. A conventional lender sees that $250,000 figure and calculates your maximum loan amount based on it, which might be hundreds of thousands of dollars less than what you can truly afford. The key is learning how to help the underwriter see beyond the AGI and recognize your business's true, consistent cash flow.

Common Income 'Add-Backs' for Self-Employed Borrowers

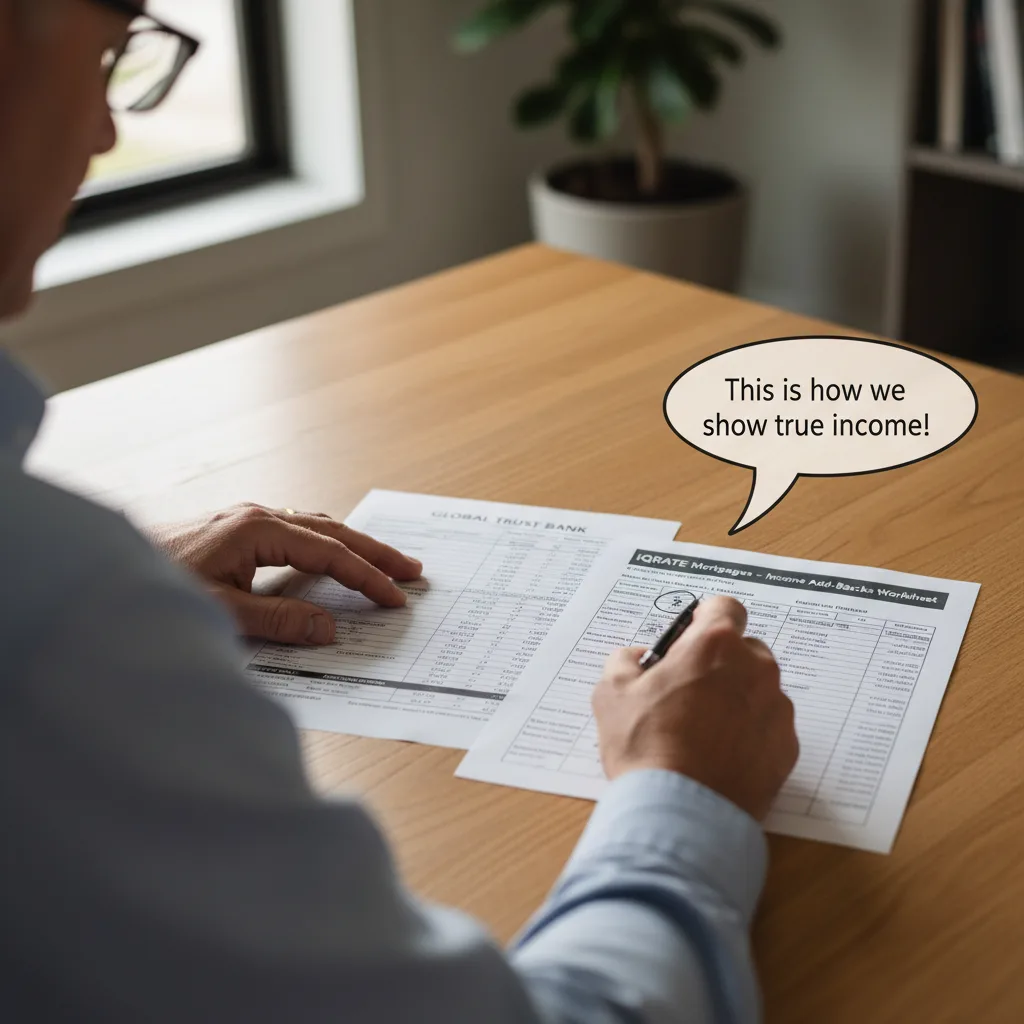

To bridge the gap between your taxable income and your qualifying income, underwriters use a process called 'adding back'. Add-backs are legitimate business expenses that reduce your taxable income but do not actually involve a cash outlay. These are 'paper losses' that can be added back to your net income to present a more accurate financial picture. Understanding and documenting these is critical to maximizing your loan amount.

Depreciation and Amortization

This is the most common and significant add-back. Depreciation is an accounting method used to allocate the cost of a tangible asset over its useful life. For example, if you bought a $60,000 company vehicle, you don't expense the full amount in one year. Instead, you might depreciate it by $12,000 per year for five years. That $12,000 is a non-cash expense deducted from your revenue. Since you didn't actually spend $12,000 in cash that year for that purpose, a mortgage underwriter can add it back to your income. This can be found on your business tax returns (e.g., Form 1120-S for an S-Corp).

Business Mileage

If you use your personal vehicle for business, you likely deduct mileage using the IRS standard rate (e.g., 67 cents per mile in 2024). If you drove 15,000 business miles, that's a $10,050 deduction. This is meant to cover fuel, maintenance, and wear-and-tear. However, since it's not a direct cash expense for that specific amount, a portion of this can often be added back to your qualifying income. (The data, information, or policy mentioned here may vary over time.)

One-Time Major Purchases

Did your business have a significant, non-recurring expense last year? Perhaps you spent $50,000 on a complete website overhaul or purchased a large piece of machinery. An experienced loan officer can argue that this was an extraordinary expense and that your income will be higher going forward without it. This requires careful documentation, such as invoices and a letter of explanation, but it can be a powerful tool for showing higher, more stable future earnings. (The data, information, or policy mentioned here may vary over time.)

Business Interest Expense

While personal interest payments are a liability, interest paid on business loans can sometimes be considered for an add-back. The logic is that the business debt is tied to an asset that generates revenue. This is a more complex calculation that depends on the lender's specific guidelines, but it's another potential area to boost your qualifying income. (The data, information, or policy mentioned here may vary over time.)

How to Prepare a Year-to-Date P&L Underwriters Will Accept

Tax returns show a snapshot of the past. To approve a jumbo loan, lenders need confidence that your business is still performing well this year. This is where a meticulously prepared Year-to-Date (YTD) Profit and Loss (P&L) statement becomes essential. A simple spreadsheet you made yourself will not suffice; it needs to be professional and credible.

An underwriter-ready P&L must include:

- Your Full Business Name and a Clear Date Range: (e.g., 'January 1, 2024 – June 30, 2024').

- Detailed Revenue Breakdown: A clear line item for 'Gross Revenue' or 'Total Sales'.

- Categorized Expenses: Don't just list a single number for 'Expenses'. Break them down into logical categories like Cost of Goods Sold (COGS), advertising, salaries, rent, utilities, etc.

- Clear Net Income Calculation: The final line should show 'Net Income' (Revenue minus Expenses).

- Your Signature and Date: You must personally attest to its accuracy.

For maximum credibility, it's highly recommended that your CPA or professional bookkeeper prepare and sign the P&L. When an underwriter sees a P&L prepared by a third-party financial professional, it carries significantly more weight. This document, when paired with corresponding business bank statements, proves that your income trajectory remains strong and supports the figures from your previous tax returns.

Using 12 or 24 Months of Business Bank Statements Instead of Tax Returns

For many business owners, the most powerful tool for jumbo loan qualification is a Bank Statement Loan. This is a non-QM (Non-Qualified Mortgage) program specifically designed for self-employed borrowers whose tax returns don't reflect their true cash flow. Instead of analyzing your tax returns, the lender analyzes your business bank statements for the most recent 12 or 24 months.

How Lenders Calculate Income from Bank Statements

The process is straightforward. The lender adds up all the business-related deposits over the chosen period (12 or 24 months) to get a total gross revenue figure. They then apply a standard 'expense factor' to arrive at a qualifying income. This factor typically ranges from 30% to 70%, depending on the industry. (The data, information, or policy mentioned here may vary over time.)

Example:

- Your business received $2,400,000 in total deposits over the last 24 months.

- This averages to $100,000 per month in gross revenue.

- The lender, knowing your industry, applies a 50% expense factor.

- Your qualifying monthly income is calculated as $50,000 ($100,000 x 0.50).

- This equates to a $600,000 annual qualifying income, which may be double or triple the AGI on your tax returns.

This method allows you to qualify based on your actual cash flow, not your tax-minimized net income. While interest rates on these programs may be slightly higher than a traditional jumbo loan, they provide access to the financing you need to purchase the right property.

Proving Consistent K1 Distributions

If you are a partner or shareholder in an S-Corporation or partnership, you receive a Schedule K-1 that reports your share of the company's income, losses, deductions, and credits. A common mistake is assuming that the income shown on your K-1 is automatically counted toward your mortgage qualification. Underwriters need to see that you have access to that money and that you are consistently receiving it as cash.

To prove this, you will need to provide a complete package of documents:

- Last two years of personal and business tax returns, including all schedules and K-1s.

- A letter from the business's CPA confirming that the business is healthy enough to support your continued distributions without negatively impacting its operations.

- Proof of distribution: This is the most crucial part. You must provide business bank statements showing the funds leaving the business account and your personal bank statements showing the corresponding deposits. Lenders look for a consistent pattern, not a single large withdrawal made just before applying for a mortgage.

How Lenders Analyze Business Debt vs. Personal Debt

Effectively managing your Debt-to-Income (DTI) ratio is key. For a business owner, a critical distinction is made between personal debts and business debts that are paid by the business.

According to Fannie Mae and Freddie Mac guidelines, if a debt (like a company vehicle loan or a business credit card) is in your personal name but is paid directly from a business bank account, it can be excluded from your personal DTI calculation. To qualify for this exclusion, you must provide 12 months of canceled checks or business bank statements showing a consistent history of the payment being made directly from the business account. (The data, information, or policy mentioned here may vary over time.)

This is a game-changer. Removing a $1,200 per month truck payment from your personal DTI calculation has the same effect as earning an additional $1,200 per month. This alone can dramatically increase your borrowing power and help you qualify for a significantly larger jumbo loan.

Specific Jumbo Loan Programs in Miami for Business Owners

Florida's luxury real estate markets, especially Miami and Naples, are filled with self-employed professionals, and specialized lenders have created products to serve them. You won't find these flexible programs at most large national banks. Instead, you need to work with a mortgage broker who has access to a network of portfolio and non-QM lenders.

Popular programs include:

- 12/24 Month Bank Statement Loans: As detailed above, these are the most common solution, using business cash flow instead of tax returns.

- Asset Depletion Loans: Perfect for high-net-worth individuals who have significant liquid assets (stocks, bonds, retirement funds) but may not have consistent W2 or business income. Lenders calculate a monthly income by dividing the total value of assets by a set term, such as 360 months. (The data, information, or policy mentioned here may vary over time.)

- P&L Only Programs: For very strong borrowers, some niche lenders may offer programs that rely solely on a 12 or 24-month CPA-prepared P&L statement, business bank statements, and a strong credit profile.

These programs are designed with the understanding that a successful business owner's finances are more complex than a salaried employee's. They provide the flexibility needed to secure financing for high-value properties. Understanding how underwriters view your business income is the key to unlocking your maximum jumbo loan potential. If you're a self-employed homebuyer in Florida, navigating the world of jumbo loans can be complex, but you don't have to do it alone. Ready to get a clear assessment of your true borrowing power? Apply now to connect with a mortgage strategist who specializes in solutions for business owners.

Unlock your true borrowing power. If you're a self-employed professional, connect with a jumbo loan specialist and see what you truly qualify for. Apply now for a clear financial assessment.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

Fannie Mae: Underwriting Factors for a Self-Employed Borrower

Consumer Financial Protection Bureau (CFPB): Debt-to-income ratio