Official VA Occupancy Rules for Military Spouses in Texas

A common source of stress for military families is the Veteran Affairs (VA) occupancy requirement. The rule states that the veteran must intend to occupy the property as their primary residence. However, the VA provides a critical exception for active-duty service members on a PCS move. If you have official orders transferring you to a location like Joint Base San Antonio or Fort Cavazos (near Killeen), your spouse’s occupancy fulfills the requirement for you.

This means your family can move into your new San Antonio home and get settled before you even arrive in Texas. The key is demonstrating 'intent'. The VA and your lender need to see that you will be joining your family and using the home as your primary residence as soon as your military duties permit. Typically, the expectation is that you will occupy the home within a 'reasonable time', which is generally considered to be 60 days after closing, but your PCS orders provide a clear justification for any delay beyond that. (The data, information, or policy mentioned here may vary over time.)

The 'Reasonable Time' Rule Explained

For most VA borrowers, moving in within 60 days is standard. For an active-duty service member with PCS orders, this timeline is more flexible. Your lender will view your official orders as the governing timeline. If your orders state your report date is 90 days after your family closes on the house, that is considered reasonable and acceptable under VA guidelines. The crucial part is communicating this clearly to your loan officer from the very beginning.

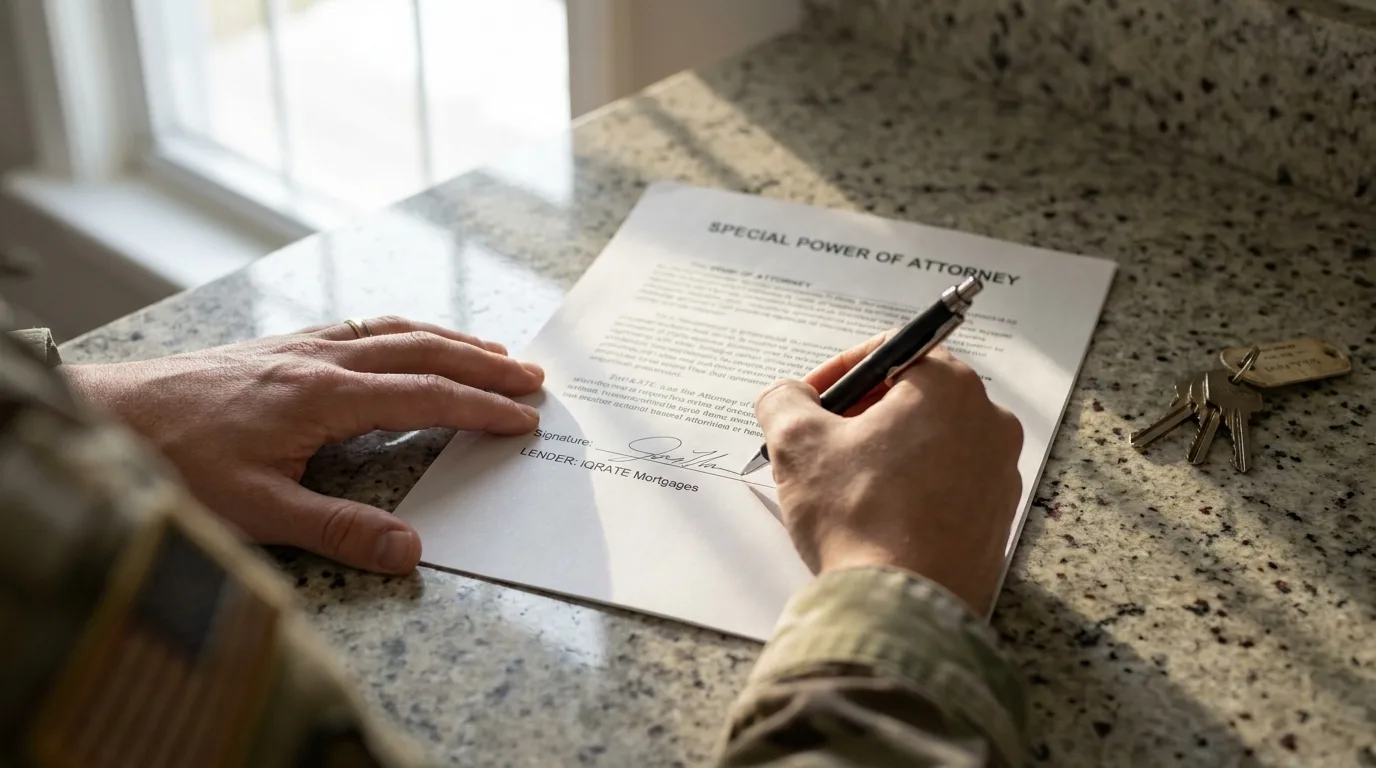

Power of Attorney Needs for a San Antonio VA Closing

For your spouse to sign legal documents on your behalf, they will need a Power of Attorney (POA). However, not just any POA will work. Most mortgage lenders and title companies require a Specific Power of Attorney. (The data, information, or policy mentioned here may vary over time.) This document is limited in scope and only grants your spouse the authority to execute documents related to the purchase of a specific property.

In contrast, a General Power of Attorney grants broad authority and is often rejected by lenders because it’s considered too wide-ranging and carries more risk. It is highly recommended that you work with your lender to get an approved POA draft before you have one created.

Here’s the best practice:

- Ask your lender for a sample or template of a Specific POA they will accept.

- Take that template to your military legal assistance office (JAG) to have it properly drafted and executed.

- Provide the executed POA back to the lender and title company for review and approval well in advance of the closing date.

Taking these steps prevents last-minute delays where the title company rejects your POA on the day of closing, which can derail your entire timeline.

Proving Occupancy Intent When You're Not Yet in Killeen

Since you won’t be at the closing table, the lender’s underwriter needs irrefutable proof of your intent to occupy the home. Your word isn’t enough; you need a solid paper trail. This documentation proves to the VA and the lender that the loan is for a primary residence and not an investment property.

Your spouse will need to provide a package of documents, including:

- A clear, legible copy of your PCS orders: This is the most critical document. It must show your name, your new duty station (e.g., Fort Cavazos), and your report date.

- A signed statement of intent: Your spouse may be asked to sign a letter at closing confirming they will be moving into the property immediately and that you will join them upon your arrival as specified by your orders.

- Evidence of moving arrangements: This could include contracts with moving companies, utility transfer confirmations for the new Killeen address, or even school enrollment forms for your children.

Together, these documents paint a clear picture for the underwriter, satisfying the VA's requirement and ensuring a smooth approval. (The data, information, or policy mentioned here may vary over time.)

Document Signing: What You Handle vs. Your Spouse

The division of labor for signing documents is straightforward once a POA is in place. Some documents require your direct signature early in the process, while your spouse handles everything at the closing table.

Documents you (the service member) typically sign:

- Initial Loan Application (URLA/Form 1003): You will almost always need to sign the initial application, which can be done electronically from wherever you are stationed.

- VA-Specific Documents: Forms like the VA Statement of Service (if applicable) and the Statement of Occupancy will require your signature.

- The Power of Attorney: You are the one granting the power, so you must be the one to sign the POA document, and it must be properly notarized.

Documents your spouse signs at closing (using the POA):

- Final Loan Application

- The Promissory Note: The legal document outlining the promise to repay the loan.

- The Deed of Trust: The document that secures the property as collateral for the loan in Texas.

- The Closing Disclosure: The final statement of loan terms and closing costs.

- All other title company and lender-specific documents.

Essentially, your spouse, acting as your 'attorney-in-fact', will sign your name on every document at closing, followed by their own name. For example: 'Sgt. John Doe by Jane Doe, his attorney-in-fact'.

How Early Closing Affects Your Home's Title and Deed

When your spouse signs on your behalf, it does not diminish your ownership rights. Both you and your spouse will be on the title and the deed as joint owners. The POA is simply the legal instrument that allows your spouse to execute the transaction for you. In Texas, a community property state, this is standard practice for married couples.

Legally, the transaction is treated exactly as if you were sitting at the closing table yourself. The Deed of Trust and Promissory Note you are committed to are fully binding. This process ensures you retain full legal ownership of your new home in San Antonio from the moment the closing is complete.

Using Future Basic Allowance for Housing (BAH) to Qualify

Yes, you can absolutely use your future BAH to qualify for your VA loan. Lenders are permitted to use future, confirmed income for active-duty military personnel. The BAH for a high-cost area like San Antonio can significantly increase your purchasing power.

To use this income, you must provide the lender with:

- Your PCS orders confirming the new duty station.

- Documentation of the BAH rate for that specific Military Housing Area (MHA). This can often be found on your Leave and Earnings Statement (LES) if it has been updated, or your lender can use the official Department of Defense BAH calculator for the corresponding zip code and pay grade.

For example, if your new BAH in Killeen will be $1,600 per month, the lender can add that amount to your base pay and other income to determine your debt-to-income ratio. This must be documented and sourced before final loan approval. (The data, information, or policy mentioned here may vary over time.)

Lender Preparation for an Early Spouse Closing in Texas

Proactive communication with your lender is the single most important factor for a successful early closing. A lender experienced with VA loans and military families will know exactly what to do.

Follow these steps for a smooth process:

- Disclose Your Situation Upfront: The very first time you speak with a loan officer, tell them you are active duty, have PCS orders, and that your spouse will be closing on your behalf with a POA.

- Provide All Documents Early: Submit your PCS orders, military IDs, and LES as soon as you have them. The earlier your loan officer has these, the better.

- Get a Lender-Approved POA Draft: Do not create a POA without the lender’s input. Ask for their specific requirements or a template to avoid rejection later.

- Have the POA Legally Executed: Use a military legal office or a qualified attorney to ensure the POA is drafted, signed, and notarized correctly.

- Coordinate with the Title Company: Your loan officer will connect you with the title company. Ensure they receive and approve a copy of the POA well before the scheduled closing date.

- Stay in Communication: Keep your loan officer updated on your travel and reporting timeline. Clear communication prevents last-minute surprises for everyone involved.

A PCS move to Texas is complex, but securing your home loan shouldn't be. If you're ready to create a clear strategy for your VA loan and an early spouse closing, take the next step to get your family settled. Apply for a Mortgage to start your journey home.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.