Am I Obligated to Use My Current Loan Servicer for an Interest Rate Reduction Refinance Loan?

No, you are absolutely not obligated to use your current mortgage company for a VA Interest Rate Reduction Refinance Loan (IRRRL). This is one of the most persistent and costly misconceptions among veterans seeking to lower their mortgage payments. The Department of Veterans Affairs (VA) guarantees the loan but does not force you to stay with your current servicer. In fact, the program is designed to promote competition among lenders, which ultimately benefits you, the veteran.

Any VA-approved lender in the country can process your IRRRL. Your current lender may send you mailers or call you, making it seem like they are your only option. They have an advantage because they already have your information, but this convenience can come at a high price. By limiting yourself to one offer, you could be leaving thousands of dollars on the table over the life of your loan. The freedom to choose your lender is a fundamental right within the VA loan program, empowering you to secure the best possible terms.

How Shopping with Multiple Lenders Can Save You Money on Your Tampa Mortgage

Shopping around is the single most effective strategy for saving money on your refinance. Interest rates are not set by the VA; they are set by individual lenders. This means that on any given day, two different VA-approved lenders can offer you vastly different interest rates and fees for the exact same loan.

Let’s consider a realistic example. Imagine a veteran in Tampa, Florida, with a remaining VA loan balance of $350,000. They are looking to refinance to a lower rate.

- Lender A (Current Servicer): Offers an IRRRL at a 6.25% interest rate. Their origination fee is 1% ($3,500), and other closing costs total $1,500, for a total of $5,000 in fees.

- Lender B (New Lender): After shopping around, the veteran finds a lender offering a 5.875% interest rate. This lender has a lower origination fee of 0.5% ($1,750) and offers a lender credit to cover the remaining closing costs.

By choosing Lender B, the veteran in Tampa would save approximately $78 per month on their principal and interest payment. Over the life of a 30-year loan, that small monthly difference adds up to over $28,000 in savings.

Furthermore, their upfront closing costs are significantly lower. This scenario highlights why getting at least three quotes from different lenders is a critical step in the refinancing process. (The data, information, or policy mentioned here may vary over time.)

What Is a 'No-Cost' Refinance and What Should I Look Out For?

The term 'no-cost' or 'no-out-of-pocket-cost' IRRRL is a popular marketing tool, but it's important to understand how it works. There is no such thing as a truly free loan; the costs are simply paid for in a different way. Typically, you achieve a 'no-cost' refinance through one of two methods: rolling the costs into the new loan balance or accepting a slightly higher interest rate in exchange for a lender credit.

Understanding Lender Credits vs. Rolling Costs into the Loan

- Rolling Costs into the Loan: With an IRRRL, you are allowed to finance the VA Funding Fee and other allowable closing costs. For example, if your closing costs are $4,000, your new loan amount would be your current principal balance plus that $4,000. While you don't pay anything at closing, you are now paying interest on a slightly larger loan for its entire term.

- Lender Credits: This is often the more attractive option. The lender offers you a credit to cover some or all of your closing costs. In exchange, you accept a slightly higher interest rate than the absolute lowest rate available. For example, the 'par' rate might be 5.75%, but the lender offers you a 6.0% rate and provides a $4,000 credit to make it a 'no-cost' loan. You avoid increasing your loan balance, but your monthly payment will be slightly higher than it would have been at the par rate. (The data, information, or policy mentioned here may vary over time.)

When evaluating a 'no-cost' offer, always ask the lender to show you the Loan Estimate. It will clearly itemize the costs and show any lender credits applied in Section J. This transparency allows you to make an informed decision about whether the convenience is worth the trade-off.

What Documents Are Needed to Apply for a VA IRRRL with a New Lender in Jacksonville?

One of the biggest advantages of the VA IRRRL is its streamlined documentation process. Because you are refinancing an existing VA loan, the lender's primary concern is confirming your entitlement and the details of your current mortgage. An appraisal and income verification are generally not required, which speeds up the process significantly.

For a veteran in Jacksonville applying with a new lender, the required documentation is minimal:

- Certificate of Eligibility (COE): While you should have a copy from your original loan, the new lender can typically pull this for you quickly and easily.

- Copy of Your Current Mortgage Note: This document outlines the terms of your existing loan.

- A Recent Mortgage Statement: This shows your current principal balance, interest rate, and servicer information.

- Proof of Homeowners Insurance: A copy of your insurance declarations page is needed to ensure the property is insured.

- Government-Issued Identification: A valid driver's license or other photo ID to verify your identity.

That's usually it. The simplicity is why it's often called a 'streamline' refinance. A good lender can gather most of this information with your authorization, making the application process for a Jacksonville veteran remarkably fast and painless.

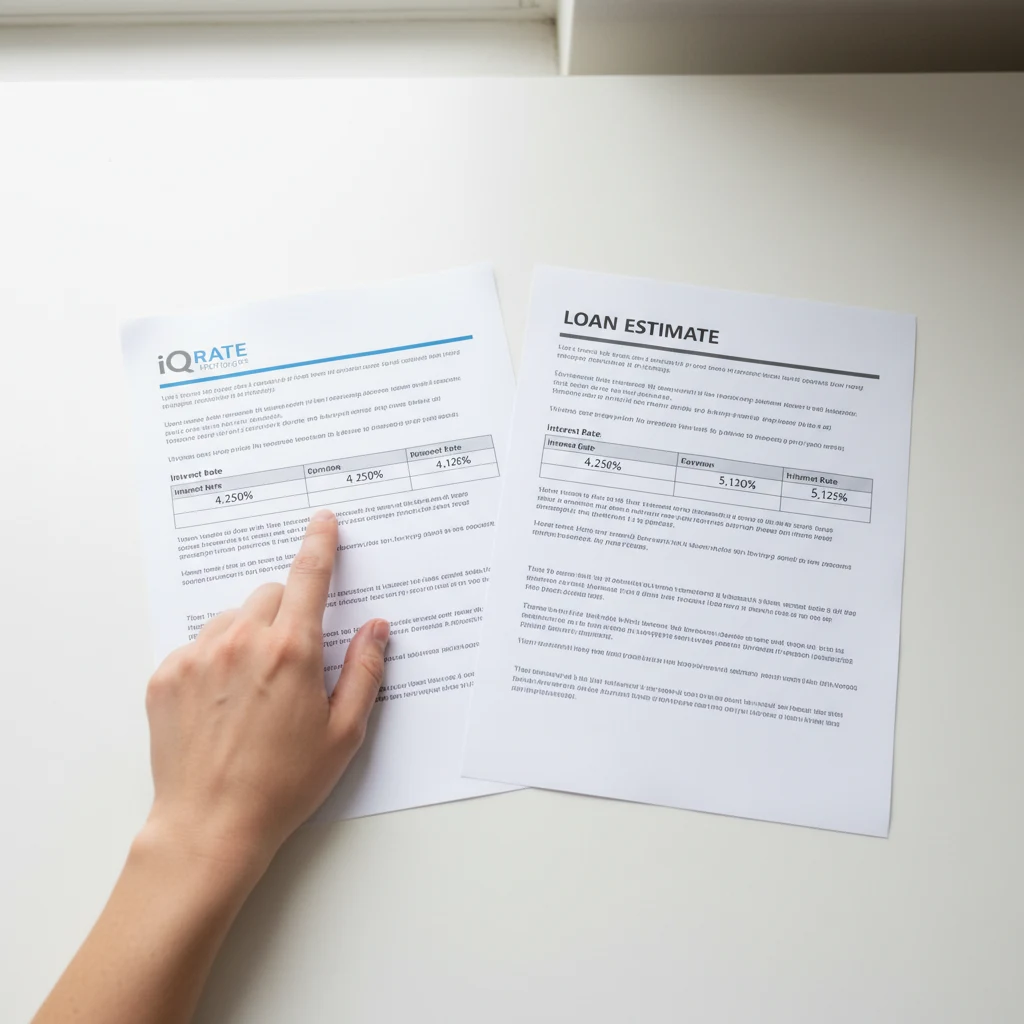

How to Effectively Compare Loan Estimates from Different Companies

Once you have Loan Estimates (LEs) from two or three lenders, you can perform an apples-to-apples comparison to find the best deal. The LE is a standardized three-page form, making this comparison straightforward if you know where to look.

Key Sections to Scrutinize on Your Loan Estimate

- Page 1 - Interest Rate and Monthly Payment: This is the most obvious comparison point. Look at the interest rate and the projected Principal & Interest payment. A lower rate almost always means long-term savings.

- Page 2, Section A - Origination Charges: This is the lender's direct profit center. It includes processing fees, underwriting fees, and points. Some lenders charge a flat fee, while others charge a percentage of the loan amount. This is a critical section for comparison, as these fees can vary dramatically.

- Page 2, Section J - Total Closing Costs & Lender Credits: This section is crucial. At the bottom, you will see a line item for 'Lender Credits'. A positive number here means the lender is giving you money to offset other costs. A larger credit is better for you. Compare the final 'Cash to Close' figure. For an IRRRL, this number should be zero or very close to it if you are opting for a 'no-cost' refinance.

Don't just focus on the interest rate. A lender might offer a rock-bottom rate but charge very high origination fees. Another lender may have a slightly higher rate but offer a substantial lender credit that covers all your costs. The Loan Estimate helps you see the complete financial picture.

Can a New Lender Process My Refinance Faster Than My Current One?

Yes, it's entirely possible and even common for a new lender to process your IRRRL faster than your current servicer. Processing speed has nothing to do with who currently holds your loan; it's a function of the lender's internal systems, staffing levels, and overall efficiency.

Large national banks that service millions of loans can often be bogged down by bureaucracy and long turn times. A smaller, more agile independent mortgage broker or lender might have dedicated teams that specialize in VA loans and can move your file from application to closing in just a few weeks. They are motivated to earn your business and provide excellent service to do so. Never assume your current servicer will be the fastest option. When you are shopping for rates, ask each potential lender about their average closing time for an IRRRL. (The data, information, or policy mentioned here may vary over time.)

Are IRRRL Rates Different Between Lenders for the Same Veteran?

Yes, absolutely. The VA does not set interest rates. The VA's role is to provide a guaranty to the lender, which reduces the lender's risk and allows them to offer favorable terms. However, each individual lending institution—banks, credit unions, and mortgage companies—sets its own rates daily.

These rates are based on several factors:

- Current Market Conditions: Lenders base their rates on the bond market, particularly mortgage-backed securities (MBS).

- Lender's Profit Margin: Each company has different overhead costs and profit goals, which are baked into the rate they offer you.

- Risk Appetite: While the VA guaranty minimizes risk, some lenders are more conservative than others.

Because of these variables, two lenders could offer the same veteran in Florida a rate that differs by 0.25% to 0.50% or more on the same day. This is the core reason why shopping your loan is not just a suggestion but a financial necessity. (The data, information, or policy mentioned here may vary over time.)

What Are the Signs of a Predatory Refinance Offer?

The VA has strict rules to protect veterans from predatory lending, but it's still wise to be vigilant. Here are some red flags to watch out for when considering an IRRRL offer:

- High-Pressure Sales Tactics: A lender who pressures you to sign immediately, claiming an offer is 'only good for today', is a major red flag. Reputable lenders provide a Loan Estimate that is valid for a set period, giving you time to compare.

- Promises of 'Skipping' Payments: Some lenders advertise that you can skip one or two mortgage payments. This isn't a gift. The interest from those skipped payments is simply rolled into your new loan balance, costing you more in the long run.

- Excessive Fees: Scrutinize Section A of the Loan Estimate. Unusually high 'origination', 'processing', or 'underwriting' fees can be a sign that the lender is padding their profits at your expense.

- Encouraging a Cash-Out Refinance Unnecessarily: If your goal is simply to lower your rate and payment, an IRRRL is the right product. If a lender aggressively pushes you toward a VA Cash-Out refinance, which has more stringent requirements and potentially higher costs, be cautious. They may be trying to generate a larger loan and higher fees.

- Vague or Evasive Answers: If a loan officer can't clearly explain the costs, benefits, and terms of the loan in a way you understand, it's time to walk away. Transparency is key.

Ready to see how much you could save on your VA IRRRL? Comparing offers from VA-approved lenders is the key to securing the most competitive rate and terms for your situation. Take the first step and Apply now to see your personalized options.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.