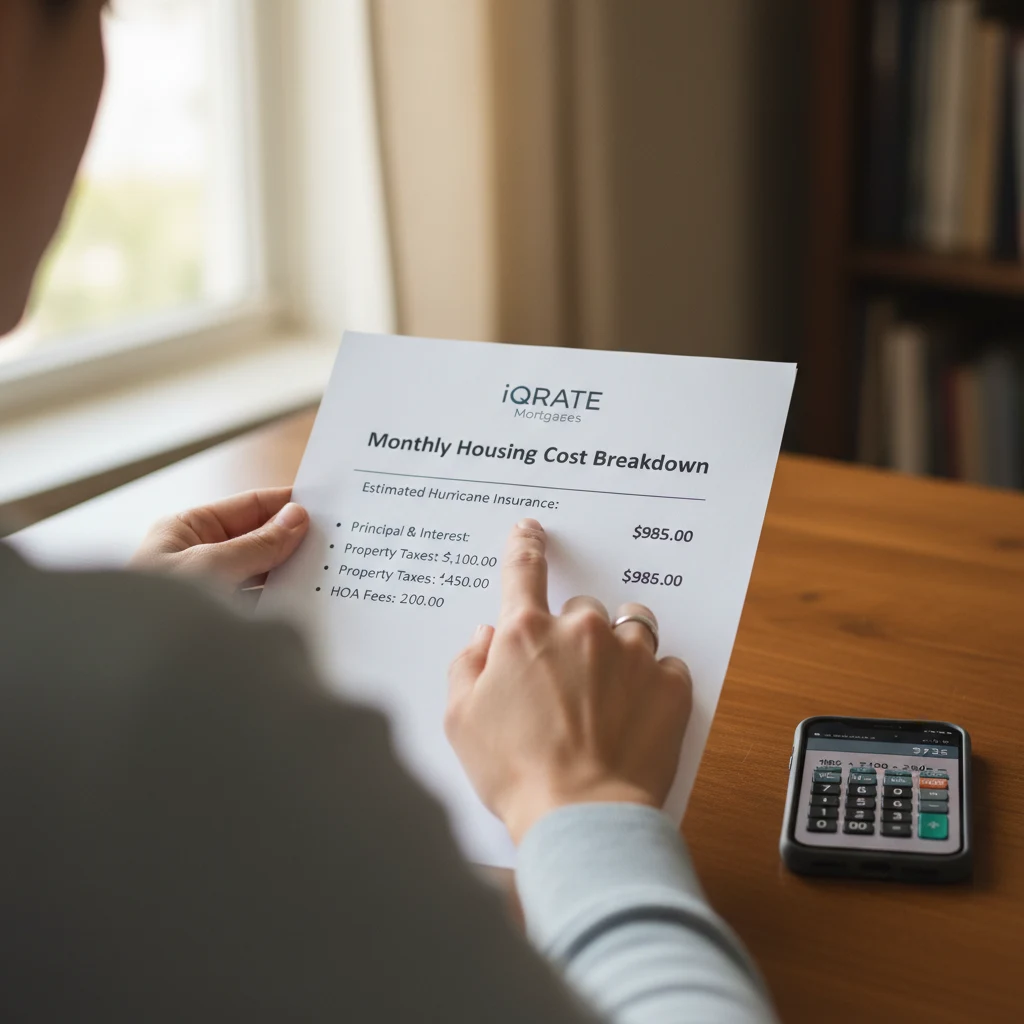

The Four Parts of a PITI Mortgage Payment

When you first look at mortgage calculators, they often show you a simple payment based on the loan amount and interest rate. This number represents only two of the four critical components that make up your total monthly housing payment. To truly understand your costs, you need to understand PITI, which stands for Principal, Interest, Taxes, and Insurance. Miscalculating this figure is one of the most common and costly mistakes Miami homebuyers make. Your lender will look at your total PITI, plus any other debts, to determine your debt-to-income (DTI) ratio and approve your loan.

Here’s a breakdown of each element:

- Principal: This is the portion of your payment that goes directly toward paying down the original amount you borrowed. In the early years of your loan, the principal portion is small, but it gradually increases over the life of the loan as your balance decreases.

- Interest: This is the cost of borrowing the money, paid to the lender. In the beginning of your mortgage term, the majority of your payment will go toward interest. As you pay down the principal, the interest portion of your payment shrinks.

- Taxes: This refers to property taxes. Instead of paying a large lump sum to the county once a year, your lender typically collects 1/12th of your estimated annual property tax bill with each monthly mortgage payment. They hold these funds in an escrow account and pay the bill on your behalf when it's due. This prevents homeowners from defaulting on their property taxes, which could put the lender's investment at risk.

- Insurance: This includes homeowners insurance (also called hazard insurance) and, if required, mortgage insurance. Similar to taxes, the lender collects 1/12th of your annual homeowners insurance premium each month and holds it in your escrow account. They then pay the premium directly to your insurance company when it's due. This ensures the property is protected against damage from events like fires or hurricanes, safeguarding both your and the lender's investment.

For example, on a $400,000 loan at 6.5% interest, your principal and interest (P&I) might be around $2,528. But after adding estimated Miami property taxes and insurance, your total PITI could easily exceed $3,800 per month. (The data, information, or policy mentioned here may vary over time.) Ignoring taxes and insurance gives you a dangerously incomplete picture of affordability.

Calculating Property Taxes for Your Miami Home Loan

Property taxes in Florida can be a significant part of your monthly housing expense, and Miami-Dade County is no exception. They are a primary source of funding for local schools, police, fire departments, and infrastructure. Understanding how they are calculated is essential for any prospective homebuyer in Miami or Hialeah.

Property taxes are determined by two main factors: the assessed value of the property and the millage rate.

- Assessed Value: The county property appraiser determines the value of your home for tax purposes. This is not always the same as the market value or the price you paid for the home. Florida offers several exemptions that can lower your home's taxable value, most notably the Homestead Exemption, which can reduce your assessed value by up to $50,000 if the property is your permanent residence.

- Millage Rate: This is the tax rate. One 'mill' is equal to $1 of tax for every $1,000 of taxable property value. The total millage rate is a combination of rates set by the county, city, school board, and other special taxing districts. These rates can vary significantly even between nearby neighborhoods.

Let’s walk through a realistic example for a home in Miami:

- Purchase Price: $500,000

- Assessed Value (by county): $480,000

- Homestead Exemption: $50,000

- Taxable Value: $480,000 - $50,000 = $430,000

- Combined Millage Rate (example): 20 mills (or 0.020)

To calculate the annual property tax, you multiply the taxable value by the millage rate:

$430,000 * 0.020 = $8,600 per year

To find the monthly amount added to your mortgage payment, you divide this by 12:

$8,600 / 12 = $716.67 per month

This $717 is just for property taxes. It's crucial to look up the current millage rates for the specific address you're considering, as a home in a different school district or municipality could have a noticeably different tax bill. (The data, information, or policy mentioned here may vary over time.)

Why Homeowners Insurance Is So Expensive in Hialeah

Florida is known for its beautiful weather, but it's also located in a region highly susceptible to natural disasters, particularly hurricanes. This elevated risk is the primary driver behind the state's notoriously high homeowners insurance premiums, and cities like Hialeah and Miami are right in the path of potential storms.

Insurance companies base their premiums on the statistical likelihood of having to pay out a claim. In South Florida, the risk of catastrophic damage from a hurricane is extremely high. This leads to several factors that inflate your costs:

- Hurricane Deductibles: Most Florida policies have a separate, much higher deductible for hurricane damage. Instead of a flat dollar amount (like $1,000), it's often a percentage of your home's insured value, typically 2%, 5%, or even 10%. On a $500,000 home with a 2% hurricane deductible, you would have to pay the first $10,000 of damages out of pocket before your insurance kicks in.

- Flood Insurance: Standard homeowners insurance policies do not cover damage from flooding, which includes storm surge from hurricanes. If your property is in a designated flood zone, your lender will mandate that you purchase a separate flood insurance policy, adding another significant annual expense.

- Age and Construction of the Home: Older homes that aren't built to modern hurricane codes will have much higher premiums. Features like impact windows, a newer roof with hurricane straps, and a reinforced garage door can lead to substantial discounts.

- Reinsurance Costs: Florida insurance companies have to buy their own insurance, called reinsurance, to cover their losses after a major storm. These global reinsurance costs have skyrocketed, and those increases are passed directly to consumers.

For a typical single-family home in Hialeah, it is not uncommon for annual homeowners insurance premiums to range from $4,000 to $8,000 or more. (The data, information, or policy mentioned here may vary over time.) A $6,000 annual premium adds $500 per month to your PITI payment. It is absolutely essential to get insurance quotes before you make an offer on a home to avoid any surprises.

How Much Does FHA Mortgage Insurance Add to My Monthly Costs?

FHA loans are a popular option for first-time homebuyers because of their low down payment requirement (as little as 3.5%) and flexible credit guidelines. However, this accessibility comes at a cost: FHA Mortgage Insurance Premium (MIP). FHA MIP is required on all FHA loans, regardless of your down payment amount.

FHA mortgage insurance has two parts:

- Upfront Mortgage Insurance Premium (UFMIP): This is a one-time fee, currently 1.75% of the loan amount. It's usually rolled into your total loan balance, so you don't pay it out of pocket at closing, but you do pay interest on it for the life of the loan.

- Annual Mortgage Insurance Premium (MIP): This is an ongoing cost, paid in monthly installments as part of your PITI payment. The rate depends on your loan term, loan amount, and loan-to-value (LTV) ratio. For most borrowers putting down 3.5%, the annual MIP is 0.55% of the average outstanding loan balance. (The data, information, or policy mentioned here may vary over time.)

Let’s see how this affects a home purchase in Miami:

- Purchase Price: $450,000

- Down Payment (3.5%): $15,750

- Base Loan Amount: $434,250

- UFMIP (1.75% of base loan): $7,600 (This is added to the loan)

- Total Loan Amount: $441,850

Now, we calculate the monthly MIP based on the annual rate of 0.55% of the base loan amount:

($434,250 * 0.0055) / 12 = $199.03 per month

This $199 is added to your monthly payment. A critical point to remember is that if you make a down payment of less than 10% on an FHA loan, you will pay MIP for the entire life of the loan. It does not automatically fall off.

Private Mortgage Insurance: A Cheaper Conventional Loan Option?

For borrowers with good credit, a conventional loan might offer a more affordable alternative through Private Mortgage Insurance (PMI). Like FHA MIP, PMI is required when you make a down payment of less than 20% on a conventional loan. It protects the lender in case you default.

However, PMI works very differently from FHA MIP, often in ways that benefit the borrower:

- Risk-Based Pricing: PMI rates are not one-size-fits-all. They are determined by your credit score and your loan-to-value (LTV) ratio. A borrower with a 760 credit score and 10% down will pay a much lower PMI rate than a borrower with a 680 score and 5% down.

- Cancellable: This is the biggest advantage. By law, you can request to have PMI removed once your loan balance reaches 80% of the home's original value. Furthermore, lenders are required to automatically terminate PMI when your balance drops to 78%.

- No Upfront Premium: Unlike FHA loans, most conventional PMI plans do not have a large upfront premium rolled into the loan.

Let’s compare with the same $450,000 home purchase, but with a conventional loan and 5% down:

- Purchase Price: $450,000

- Down Payment (5%): $22,500

- Loan Amount: $427,500

- Borrower Credit Score: 740

With a good credit score, the monthly PMI rate could be around 0.45%. (The data, information, or policy mentioned here may vary over time.) Let's calculate the monthly cost:

($427,500 * 0.0045) / 12 = $160.31 per month

In this scenario, the monthly PMI is about $39 cheaper than the FHA MIP. More importantly, this borrower can eventually eliminate the $160 monthly payment, while the FHA borrower would be stuck with their $199 payment for the life of the loan unless they refinance.

Getting Accurate Tax and Insurance Estimates Before an Offer

An educated homebuyer is a prepared homebuyer. Relying on generic online calculators for your budget is a recipe for disaster in a high-cost market like South Florida. To avoid being 'house poor', you must do your due diligence before you even submit an offer.

Here are actionable steps to get accurate numbers:

- Check the County Property Appraiser Website: For any property in Miami or Hialeah, you can visit the Miami-Dade County Property Appraiser's website. Look up the address to see its current assessed value and tax history. While the taxes may be reassessed after you buy, the history gives you a very realistic baseline.

- Call Multiple Insurance Agents: Do not wait for your lender to estimate your insurance. As soon as you are serious about a property, call at least two or three independent insurance agents. Provide them with the property address and details. They can give you firm quotes for homeowners and flood insurance, which can vary wildly between companies.

- Ask Your Lender for a Detailed Loan Estimate: A Loan Estimate is a standardized document that breaks down all your estimated costs, including your monthly PITI. A good loan officer will use the actual tax data and the insurance quote you provide to give you a highly accurate monthly payment projection.

Don't Forget Homeowners Association (HOA) Fees

Finally, one major expense is often overlooked because it's not technically part of your PITI payment: Homeowners Association (HOA) fees. Condos, townhomes, and many single-family home communities in Miami and Hialeah are governed by an HOA.

These fees cover the maintenance of common areas like swimming pools, landscaping, security, and building exteriors. HOA fees can range from a couple of hundred dollars to over a thousand dollars per month. (The data, information, or policy mentioned here may vary over time.)

Crucially, while you pay the HOA directly and not through your mortgage servicer's escrow account, your lender absolutely includes this fee when calculating your debt-to-income ratio. A $600 monthly HOA fee has the same impact on your borrowing power as a $600 car payment. Always verify the current HOA fee for any property you're considering and ask if any special assessments are planned, as these can add unexpected costs. Understanding the complete picture of your monthly housing costs is the most important step in a successful home purchase. Before you start your search in Miami or Hialeah, connect with a mortgage expert who can provide a detailed and accurate breakdown of your potential PITI payment, ensuring you find a home that truly fits your budget.

Understanding your complete PITI is the first step to smart homeownership. If you're ready to see how these numbers apply to your dream home in Miami or Hialeah, we're here to help. Take the next step and Apply now for a clear, no-obligation mortgage pre-qualification.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

Consumer Financial Protection Bureau (CFPB) - What is PITI?

U.S. Department of Housing and Urban Development (HUD) - FHA Mortgage Insurance