What is a Veteran Affairs Interest Rate Reduction Refinance Loan?

A Veteran Affairs Interest Rate Reduction Refinance Loan, commonly known as a VA IRRRL or Streamline Refinance, is a mortgage product exclusively for veterans who already have a VA home loan. Its primary purpose is simple: to help you secure a lower interest rate, which in turn lowers your monthly mortgage payment. The 'streamline' name refers to the reduced amount of paperwork and underwriting required compared to a conventional refinance or a new home purchase loan.

Key features of an IRRRL include:

- No Appraisal Required: In most cases, the lender does not require a new property appraisal, which saves you time and money.

- No Income Verification: Lenders typically don't require you to re-verify your income, making the process faster for those whose financial situation may have changed.

- Limited Underwriting: The process focuses on the benefit to the veteran—namely, the interest rate reduction. Credit score requirements are often more lenient than with other loan types.

- Primary Occupancy: You only need to certify that you previously occupied the home as your primary residence. This makes it a great option for refinancing a property that is now a rental.

The core requirement is that the new loan results in a tangible benefit, such as moving from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage or achieving a lower principal and interest payment. It is not a tool for taking cash out of your home's equity.

How do lenders advertise these as 'no-cost' loans in Miami?

The term 'no-cost' or 'no out-of-pocket' is a powerful marketing tool that can be misleading. When a lender in Miami or elsewhere in Florida offers a 'no-cost' VA IRRRL, it does not mean the transaction is free. The closing costs associated with any mortgage—origination fees, title insurance, recording fees, and the VA funding fee—still exist. Instead of you paying for them with a check at closing, these costs are handled in one of two ways:

Rolling Costs into the Loan: This is the most common method. The lender takes all the closing costs and adds them to your new loan principal. For example, if you are refinancing a $350,000 loan and have $5,000 in closing costs, your new loan balance will be $355,000. You pay nothing upfront, but you are now paying interest on a larger loan amount over the life of the loan.

Accepting a Higher Interest Rate (Lender Credits): A lender might offer you a slightly higher interest rate in exchange for a 'lender credit' that covers some or all of your closing costs. For instance, you might qualify for a 5.5% interest rate, but the lender offers you a 5.75% rate and uses the difference to pay your closing costs. While you avoid increasing your loan balance, your monthly payment will be higher than it could have been, and you'll pay more in interest over the long run.

Neither option is inherently 'bad', but it's critical to understand that the costs are being paid one way or another. The 'no-cost' label simply refers to the absence of upfront, out-of-pocket expenses.

What are the typical closing costs that can be rolled into the loan?

With a VA IRRRL, the Department of Veterans Affairs allows most of the closing costs to be financed into the new loan. This makes the streamline process accessible even if you don't have cash on hand for closing. The costs you can expect to see on your loan estimate include:

- VA Funding Fee: This is a mandatory fee paid directly to the VA to help fund the loan guaranty program. For an IRRRL, the fee is a flat 0.5% of the loan amount for all veterans, regardless of service history or down payment. (The data, information, or policy mentioned here may vary over time.)

- Lender's Origination Fee: This fee covers the lender's administrative costs for processing and underwriting your loan. The VA caps this fee at 1% of the loan amount. (The data, information, or policy mentioned here may vary over time.)

- Discount Points: These are optional fees you can pay to 'buy down' your interest rate. One point typically costs 1% of the loan amount.

- Title and Recording Fees: These are third-party charges for title insurance, which protects the lender, and county fees for officially recording the new mortgage lien.

- Other Third-Party Fees: This can include charges for a credit report or other minor administrative services.

What you cannot roll into an IRRRL are things like property taxes and homeowners insurance. These must be handled separately through your escrow account.

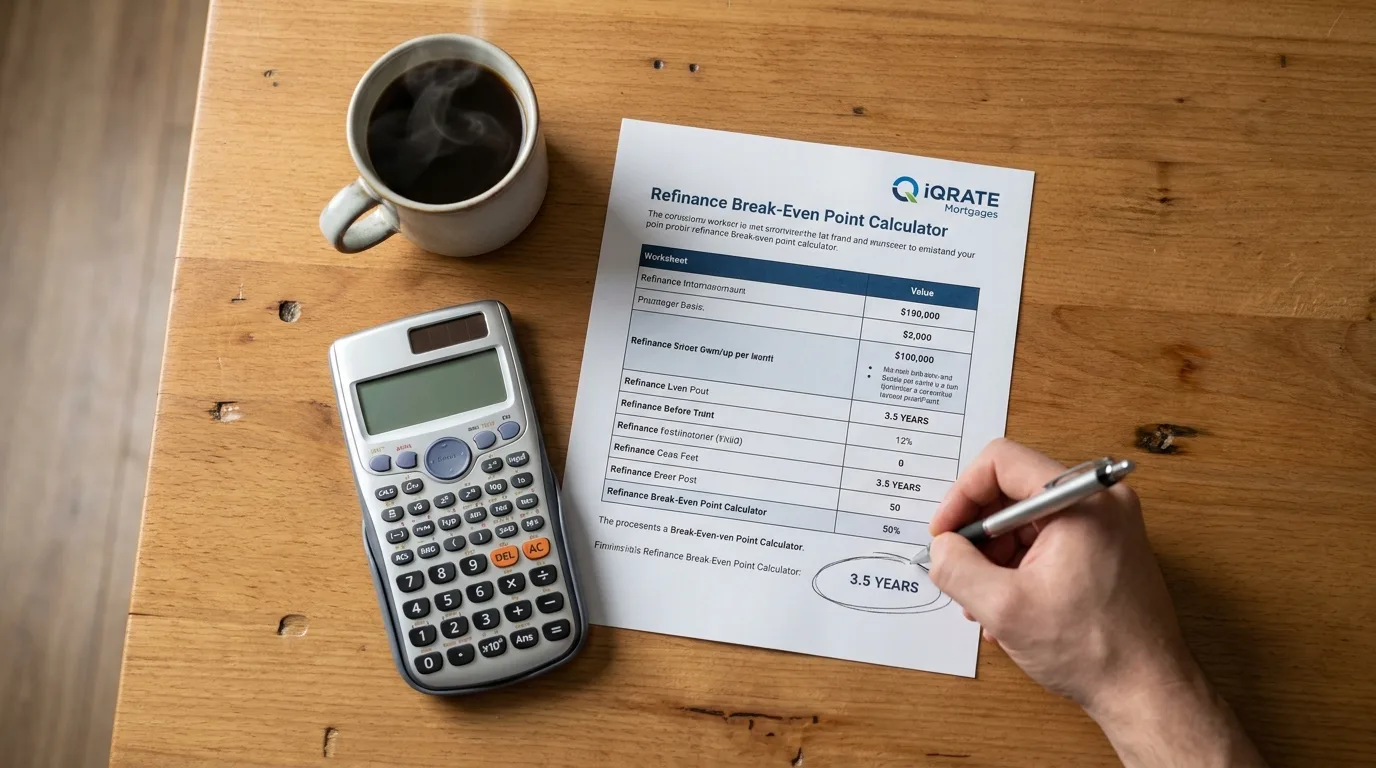

How do I calculate the break-even point for my Orlando refinance?

Understanding your break-even point is the most important calculation you can make when considering a VA IRRRL. It tells you the exact number of months it will take for your accumulated monthly savings to cover the total closing costs. After this point, you begin to realize true savings.

The formula is straightforward:

Total Closing Costs ÷ Monthly Savings = Break-Even Point (in months)

Let's walk through a realistic example for a veteran living in an Orlando suburb:

- Current Loan Balance: $400,000

- Current Interest Rate: 6.5% (Principal & Interest Payment: $2,528)

- New Proposed Interest Rate: 5.5%

Step 1: Calculate the Total Closing Costs

- VA Funding Fee (0.5% of $400,000): $2,000

- Lender Origination Fee (1% of $400,000): $4,000

- Title & Recording Fees: $1,200

- Total Closing Costs: $2,000 + $4,000 + $1,200 = $7,200

Step 2: Calculate the New Monthly Payment and Savings

- The new loan balance will be the original balance plus the closing costs: $400,000 + $7,200 = $407,200.

- New Principal & Interest Payment at 5.5% on $407,200: $2,312

- Monthly Savings: $2,528 (old payment) - $2,312 (new payment) = $216

Step 3: Calculate the Break-Even Point

- $7,200 (Total Costs) ÷ $216 (Monthly Savings) = 33.3 months

In this Orlando scenario, it will take just over 33 months, or about 2 years and 9 months, to recoup the costs of the refinance. If you plan to stay in your home longer than that, the IRRRL is a financially sound decision. If you might sell before then, the refinance would cost you money.

Does a lower interest rate always mean I will save money?

No, a lower interest rate is not an automatic guarantee of long-term savings. The total cost of a loan depends on three factors: the loan amount, the interest rate, and the loan term. While an IRRRL effectively lowers your rate, it can negatively impact the other two factors if you're not careful.

Consider a situation where you have 25 years remaining on your current 30-year mortgage. If you refinance into a new 30-year term to get the lowest possible payment, you have just added five years of payments back onto your timeline. Even with a lower interest rate, paying a mortgage for an extra five years could lead to you paying thousands more in total interest over the life of the loan.

This is why the net tangible benefit rule is so important. A good lender will show you an amortization schedule comparing your old loan to your new one, clearly illustrating the total interest paid in both scenarios. If the primary goal is long-term wealth building, you should aim to refinance into a term that is equal to or shorter than what you have remaining on your current loan. A 25-year or 20-year term might have a slightly higher payment than a new 30-year term, but it will save you a substantial amount in interest and help you build equity faster.

When is it a bad idea to get a streamline refinance in Florida?

A VA IRRRL is a powerful tool, but it's not right for every situation. Here are several scenarios where proceeding with a streamline refinance in Florida could be a financial mistake:

- You Plan to Sell Soon: If your break-even point is 36 months but you plan to relocate from Miami for a new job in 18 months, you will lose money on the transaction. You won't own the home long enough for the monthly savings to cover the closing costs.

- The Monthly Savings are Minimal: If a refinance only saves you $40 or $50 per month, the break-even point could be many years away. A small change in your budget might not be worth re-starting your loan term or adding costs to your principal.

- Your Goal is Debt Consolidation: The IRRRL program strictly limits the amount of cash back a veteran can receive. If you need to pay off high-interest credit cards or other debt, the VA Cash-Out Refinance is the appropriate product, not an IRRRL.

- You're Extending Your Loan Term Significantly: As mentioned before, refinancing from a loan with 22 years left into a new 30-year mortgage can dramatically increase the total interest you pay over time, even if the rate is lower. This is a common pitfall.

What questions should I ask a lender about their IRRRL offer?

To protect yourself and ensure you're making an informed decision, you must ask direct and specific questions. Any reputable lender should be able to provide clear and immediate answers.

- 'Can you provide me with an official Loan Estimate?' This document legally requires lenders to disclose all costs, the interest rate, and the new loan amount. Do not rely on verbal quotes.

- 'What is the total dollar amount of the closing costs being added to my loan balance?' Get the exact number. This is crucial for your break-even calculation.

- 'What is the new loan term? Is it different from my current term?' Make sure you know if you are extending the life of your debt.

- 'Based on these costs and my new payment, what is my exact break-even point in months?' Make the lender do the math for you and then double-check it yourself.

- 'Are there any discount points included in this offer? Are they required?' Understand if you are paying extra to lower the rate and if you have the option to decline them for a slightly higher rate and lower costs.

- 'Can you show me a comparison of the total interest paid over the life of the old loan versus the new loan?' This reveals the true long-term financial impact of the decision.

Can I get cash out with this type of Veteran Affairs loan?

No, you cannot get a significant amount of cash out with a VA IRRRL. The program's sole purpose is to reduce your interest rate and monthly payment. While you may receive a small amount of money back at closing, this is typically a reimbursement for fees you paid upfront and is not considered 'cash out'. If your primary goal is to tap into your home's equity to receive cash for renovations, debt consolidation, or other purposes, you need to use the VA Cash-Out Refinance loan program. This is a different product with different requirements, including a new appraisal and full income and credit underwriting. Understanding the nuances of a VA IRRRL is key to making a decision that benefits your financial future. If you're ready to see a clear, transparent breakdown of your potential savings and break-even point, contact a mortgage expert who can analyze your specific situation and provide an honest assessment.

Ready to determine if a VA IRRRL is your next smart financial decision? Let's review your options and calculate your actual savings. Apply now for a transparent mortgage analysis.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.