What Are Lender Overlays and Why Do They Exist?

A mortgage denial is frustrating, especially when you believe you meet the requirements. If your FHA loan application was denied in Las Vegas with a 620 credit score, you've likely encountered a lender overlay.

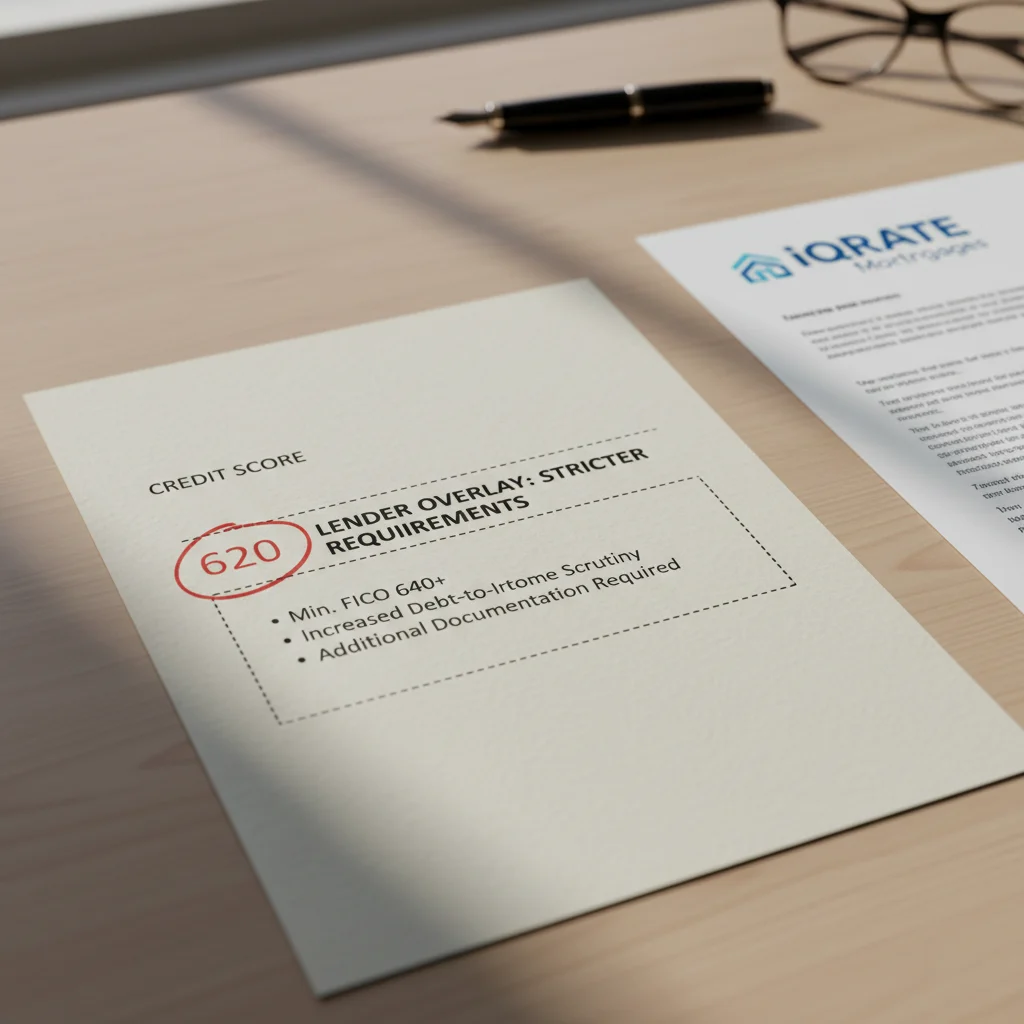

An overlay is an additional, stricter guideline a lender adds on top of the minimum requirements set by the Federal Housing Administration (FHA). The FHA itself doesn't lend money; it only insures the loan. The actual funds come from a private lender, and that lender has the right to impose its own rules to minimize its financial risk.

Think of it this way: the FHA sets the floor, but the lender can build the ceiling wherever they want. For example:

- FHA Guideline: Minimum credit score of 580 for a 3.5% down payment.

- Lender Overlay: Minimum credit score of 640 for the same loan.

Lenders use overlays for several reasons:

- Risk Management: Lenders believe borrowers with higher credit scores are less likely to default. They impose a higher minimum score to protect their portfolio.

- Investor Requirements: Many lenders sell their closed loans on the secondary market. The investors who buy these loans may demand stricter standards than the FHA, forcing the lender to add overlays.

- Operational Capacity: Underwriting loans for borrowers with lower scores or complex financial histories requires more time and experienced staff. Some lenders avoid this by setting overlays that filter out these applications.

So, your 620 score didn't disqualify you from an FHA loan; it just disqualified you from that specific lender's version of an FHA loan.

Is a 620 Credit Score High Risk for a Las Vegas FHA Loan?

From the FHA's official standpoint, a 620 credit score is not considered high risk. The FHA's mission is to promote homeownership, and their guidelines are intentionally flexible to help borrowers who may not qualify for conventional loans. Their rules clearly state:

- 580+ Credit Score: Eligible for maximum financing with a 3.5% down payment.

- 500-579 Credit Score: Eligible for a loan with a 10% down payment.

However, in the eyes of a lender with a '640 minimum' overlay, your 620 score falls into their high-risk category. This is a business decision on their part, not a reflection of your overall creditworthiness or ability to repay the loan. Many capable homebuyers in cities like Henderson and Las Vegas get denied not because they are a true risk, but because they simply applied with the wrong institution.

How to Find FHA Lenders in Las Vegas With No Overlays

Finding a lender that adheres to true FHA guidelines is the most important step after a denial. The good news is that these lenders exist; you just have to know how to find them.

Work With an Independent Mortgage Broker

This is the most efficient strategy. Unlike a bank loan officer who only offers one set of products and rules, a mortgage broker partners with dozens or even hundreds of wholesale lenders. They have access to a diverse range of loan programs and know exactly which lenders have no FHA credit score overlays. A broker can take your single application and submit it to a lender who is comfortable with a 620 score, saving you time and preventing further credit inquiries.

Ask the Right Questions Upfront

When speaking with a new loan officer, be direct to avoid wasting time. Before you even submit an application, ask these questions:

- 'What is your lender's absolute minimum credit score for an FHA loan?'

- 'Do you have any lender overlays on FHA loans related to credit score or debt-to-income ratios?'

If they answer '640' or 'yes', you know to move on. A transparent loan officer will give you a straight answer.

Other Factors That Can Cause an FHA Loan Denial

While a lender overlay is the most common reason for a denial with a 620 score, other issues in your file could also be contributing factors. It's crucial to review your entire financial profile.

- High Debt-to-Income (DTI) Ratio: FHA guidelines can be generous, sometimes allowing a DTI ratio over 50%. However, a lender might impose an overlay capping DTI at 45%. If your score is 620 and your DTI is 52%, the lender may see this combination as too risky.

- Insufficient Cash to Close: You need to verify you have enough funds for the 3.5% down payment plus closing costs, which typically run 2-5% of the purchase price. (The data, information, or policy mentioned here may vary over time.) Gifts from family are acceptable but must be properly documented.

- Unstable Employment History: The FHA requires a consistent two-year employment history. Frequent job changes, significant gaps in employment, or a recent switch from a salaried (W2) role to self-employment can be red flags for an underwriter.

- Property Condition: FHA appraisals include Minimum Property Standards (MPS). If the home you want to buy in Henderson has issues like a leaky roof, peeling paint, or a faulty HVAC system, the appraiser will flag it. The loan cannot close until these issues are repaired.

Can a Manual Underwrite Secure an FHA Approval?

Yes, a manual underwrite can be a powerful tool for getting an FHA loan approved, especially for files that don't fit perfectly into the automated system's algorithm.

Most loan applications are first processed by an Automated Underwriting System (AUS). If the AUS returns a 'Refer' or 'Caution' finding, it doesn't mean an automatic denial. It means the file requires a human underwriter to review it—a process called manual underwriting.

For a borrower with a 620 score, a manual underwrite allows an underwriter to consider compensating factors that the AUS might ignore. These can include:

- Large cash reserves after closing.

- A low DTI ratio.

- A long, stable history with the same employer.

- Minimal 'payment shock' (your new mortgage payment is similar to your current rent).

A skilled loan officer can build a strong case for a manual underwrite, demonstrating that despite the credit score, you are a reliable borrower.

Does a Lower Score Mean a Much Higher Interest Rate?

A lower credit score will result in a higher interest rate, but the impact is often less severe with FHA loans compared to conventional loans. Conventional loans use a risk-based pricing model with Loan-Level Price Adjustments (LLPAs), where a lower score can significantly increase your rate and costs.

FHA loan pricing is less sensitive to credit scores. While a difference exists, it's usually smaller. For example, on a $450,000 home purchase in Las Vegas, a borrower with a 740 score might secure a rate of 6.25%, while a borrower with a 620 score might be offered 6.75%. The difference in the monthly principal and interest payment would be around $175. (The data, information, or policy mentioned here may vary over time.)

Will Henderson Down Payment Assistance Programs Work With Lower Scores?

This is a critical point of caution. Many Down Payment Assistance (DPA) programs are designed to work with FHA loans, but they often come with their own set of overlays—including higher credit score minimums.

For instance, a Nevada state DPA program might require a 640 credit score, even if you find an FHA lender willing to approve your loan at 620. In this scenario, you would have to choose between using the DPA program (which would require improving your score) or forgoing the assistance to close sooner with the more flexible lender.

Before you count on DPA funds, you or your mortgage professional must verify the credit score requirements for both the DPA provider and the mortgage lender to ensure they are compatible. If you've been denied for an FHA loan in Nevada due to a lender overlay, don't give up. The issue isn't your eligibility, but the lender you chose. A mortgage expert can connect you with lenders who follow true FHA guidelines, turning your denial into an approval.

Don't let a lender overlay stop your homeownership dream. If you're ready to connect with a mortgage expert who understands true FHA guidelines and can find a path to approval, the next step is simple. Apply now to get a clear assessment of your options.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.