The Listing Presentation Dilemma: 'Can This Property Even Be Financed?'

You walk into a listing presentation for a unique condo in Miami. The view is spectacular, the location is prime, but the seller hits you with the question that sinks dozens of agents every day: 'I've heard this building is tough to get a loan in. Are we wasting our time?' This is the moment where top agents separate themselves from the pack. The typical response involves vague assurances and a 'let's cross that bridge when we get to it' mentality. Unfortunately, that’s not enough to earn a seller's trust or their signature on a listing agreement.

Sellers with 'problem properties' are risk-averse. They fear months of their home being tied up in a contract only for the buyer's financing to fall through at the last minute. For you, the agent, the stakes are just as high. Taking on a property that can't be financed leads to:

- Wasted Marketing Dollars: Professional photos, virtual tours, and ad campaigns add up quickly, all for a property that may be unsellable to 90% of the market.

- Lost Commission: The ultimate opportunity cost of spending three months on a deal that was doomed from the start.

- Damaged Reputation: A collapsed sale reflects poorly on everyone involved. The seller is frustrated, and your reputation for closing deals takes a hit.

In competitive markets like Naples and Miami, you can't afford to walk into a listing appointment with hope as your only strategy. You need to walk in with a concrete plan.

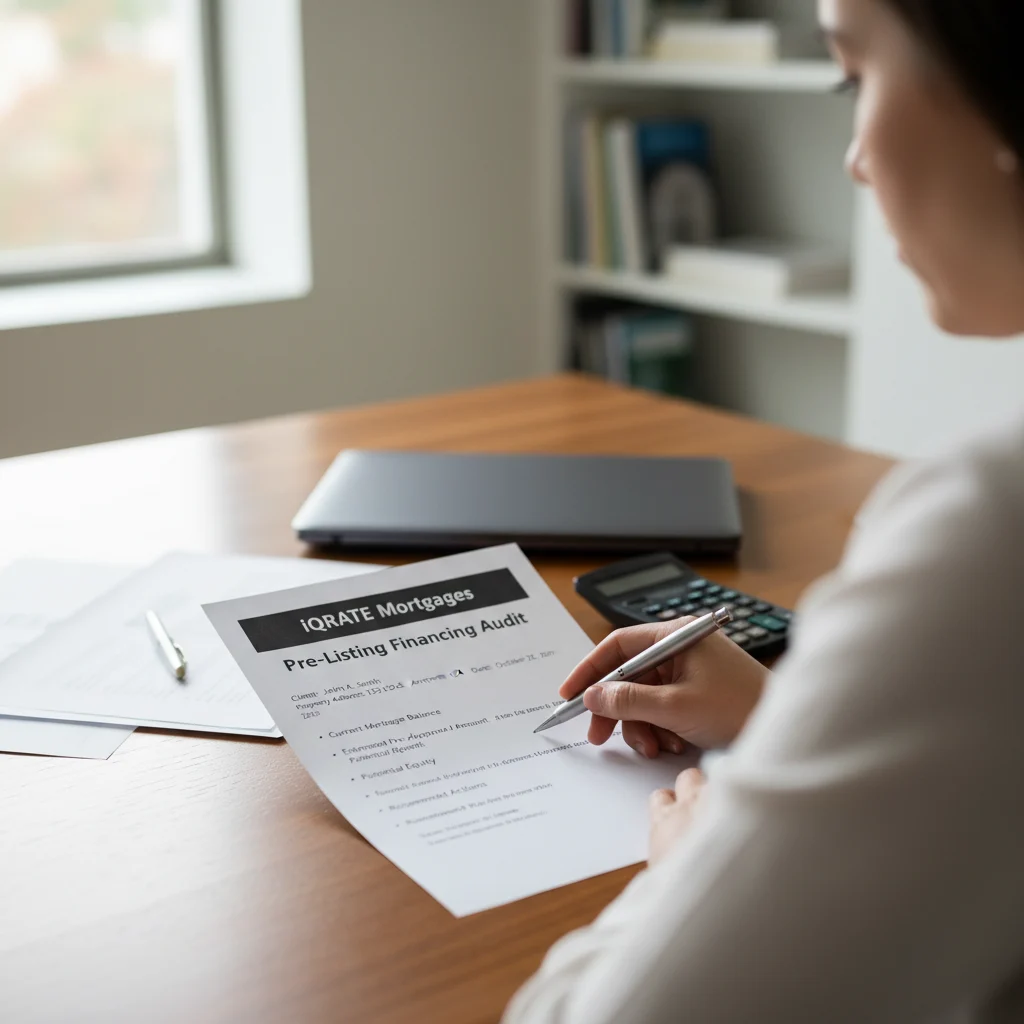

From Uncertainty to Contract: The Power of a Pre-Listing Financing Audit

Imagine a different scenario. The seller voices their financing concerns. Instead of offering empty platitudes, you present a 'Financing Viability Audit'. This document, prepared by a mortgage strategist, outlines specific, viable loan programs that are a perfect fit for their unique property. It details the types of buyers who would qualify, the potential terms, and a clear roadmap for a successful closing.

This audit transforms your value proposition. You are no longer just a marketing expert; you are a problem-solver with a tangible solution. The Financing Viability Audit is a pre-emptive strike against the single biggest hurdle in selling a challenging property. It shifts the conversation from 'if' the property can sell to 'how' it will sell, giving the seller the confidence they need to list with you.

What Makes a Property a 'Financing Challenge' in Florida?

Not all properties fit into the neat boxes that conventional lenders prefer. In Florida’s diverse real estate landscape, you will frequently encounter properties with quirks that send traditional underwriters running. Here are the most common culprits.

Non-Warrantable Condos in Miami

A condo is deemed 'non-warrantable' if it doesn't meet the strict criteria set by Fannie Mae and Freddie Mac. This immediately disqualifies buyers seeking conventional loans. Common reasons include:

- High Investor Concentration: Too many units are owned by investors rather than primary residents.

- Single Entity Ownership: One person or company owns more than 10% of the units. (The data, information, or policy mentioned here may vary over time.)

- Pending Litigation: The condo association is involved in a lawsuit.

- Inadequate Reserves: The HOA's budget doesn't meet lender requirements for maintenance and repairs. (The data, information, or policy mentioned here may vary over time.)

- Condo-Hotel Structure: The building operates partially as a hotel.

Example: A seller owns a unit in a popular South Beach condo-hotel. It’s a fantastic property, but nearly impossible to finance conventionally. An audit would identify lenders specializing in condo-hotel financing or portfolio loans, which are held on the lender's own books and don't need to meet government-backed standards. The audit provides a clear path forward, targeting a specific niche of vacation home or investor buyers.

Homes with Unpermitted Work or Significant Repair Needs

Florida's older housing stock often comes with surprises. A previous owner might have enclosed a patio without permits, or a 30-year-old roof might be at the end of its life. These issues are red flags for lenders, who worry about the property's value and safety.

Example: You're looking to list a charming single-family home in a historic Naples neighborhood, but it needs a new roof and has an unpermitted garage conversion. A standard buyer's loan will be denied. A Financing Viability Audit would propose solutions like an FHA 203(k) Renovation Loan or a Fannie Mae HomeStyle Loan. (The data, information, or policy mentioned here may vary over time.) These programs roll the cost of repairs into the mortgage. For a home listed at $450,000 needing $50,000 in work, the buyer could secure a single loan for $500,000, allowing them to purchase and immediately renovate the home. This opens up the property to a massive pool of buyers who don't have cash for post-closing repairs.

Unique and Mixed-Use Properties

What about a property with a small retail storefront on the ground floor and a residential apartment above? Or a property zoned for residential use but currently operating as a small business office? These 'mixed-use' properties don't fit the residential or commercial mold perfectly, making them difficult to finance.

An audit would explore niche lenders who offer specialized portfolio loans designed for such properties. It would identify the exact documentation needed, like profit and loss statements for the commercial portion, and prepare the seller and agent for the specific requirements, ensuring a smooth process.

How the Financing Viability Audit Secures Your Listing

This isn't just a piece of paper; it's a strategic process designed to give you a decisive advantage. Partnering with a mortgage broker who specializes in complex deals makes it seamless.

Step 1: Property and Seller Intake

The process begins with a deep dive into the property. We gather all relevant documents, such as the condo association's budget and master policy, a list of known property issues, and any existing surveys or appraisals. This is a fact-finding mission to identify every potential roadblock.

Step 2: Lender Network Analysis

This is where expertise makes all the difference. Instead of applying to one or two banks, a mortgage strategist leverages a network of over 100 lenders. The unique property scenario is presented to portfolio lenders, private banks, and credit unions that have an appetite for non-traditional loans. We find the partners who see opportunity where others see risk.

Step 3: The Audit Report - Your Secret Weapon

The final deliverable is a clear, concise report that you can present to the seller. It includes:

- 2-3 Viable Loan Programs: Specific loan products from named lenders that are a confirmed match for the property.

- Ideal Buyer Profile: A description of the buyer who would qualify (e.g., 'An investor with 25% down' or 'A primary resident using an FHA 203(k) loan').

- Estimated Terms: A realistic look at potential interest rates, down payment requirements, and closing timelines. (The data, information, or policy mentioned here may vary over time.)

- Required Documentation: A checklist of what a qualified buyer will need to provide.

Walking into your listing presentation in Miami or Naples with this report demonstrates unparalleled preparation and expertise. You have already solved the seller's biggest problem.

The Tangible Benefits for You and Your Seller

Adopting this strategy fundamentally changes the listing and sales process for challenging properties, creating a win-win for everyone involved.

For the Real Estate Agent

- Win More Listings: You stand out from competitors by providing concrete solutions, not just promises.

- Price the Property Accurately: Knowing the exact financing limitations allows you to set a price that reflects the true market, whether it's limited to cash buyers or open to renovation financing.

- Market Intelligently: You can tailor your marketing message to attract the right buyer profile identified in the audit.

- Reduce Deal Fallout: By pre-vetting the financing, you drastically lower the risk of a deal collapsing in underwriting, protecting your time and commission.

For the Seller

- Confidence to List: The audit removes the fear of the unknown and provides a clear path to a successful sale.

- Access to a Larger Buyer Pool: The property is no longer limited to cash-only offers. You unlock a vast market of financed buyers.

- Stronger Negotiating Position: With confirmed financing options available, sellers are less likely to accept a lowball cash offer out of desperation.

- A Faster, Smoother Closing: The financing strategy is established from day one, eliminating last-minute surprises and delays. Don't let financing uncertainty cost you another listing in Miami or Naples. Partner with a mortgage strategist who can give you the answers you need upfront. Contact iQRATE Mortgages today to request a complimentary Financing Viability Audit for your next problem property.

Facing a complex property situation in Miami or Naples? Let us provide the clarity you need. Apply now to start your complimentary Financing Viability Audit and turn your challenging listing into a closed deal.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

Fannie Mae Condominium Project Guidelines