How soon can I start the VA loan process before my PCS move?

Receiving your Permanent Change of Station (PCS) orders kicks off a flurry of activity, and securing housing is at the top of the list. You can, and should, start the VA loan process well before you pack a single box. Most lenders allow you to begin the pre-approval process as soon as you have your official orders in hand, which can be anywhere from 60 to 90 days before your report date. (The data, information, or policy mentioned here may vary over time.)

Starting early provides a significant strategic advantage. It gives you a clear, lender-verified budget, allowing you to house hunt with confidence. For military families moving to competitive markets like Killeen or El Paso, being pre-approved makes your offer much stronger to sellers who prefer a quick and certain closing.

To get started, you will need three key military documents:

- Your Certificate of Eligibility (COE): This official document proves to the lender that you meet the VA's requirements for a home loan based on your service.

- Your PCS Orders: These confirm your new duty station and report date, which is critical for satisfying occupancy requirements.

- Your Leave and Earnings Statement (LES): This verifies your income, rank, and time in service.

Getting pre-approved early allows you to lock in an interest rate, protecting you from market fluctuations while you search for your new home. It transforms a stressful scramble into a well-managed plan.

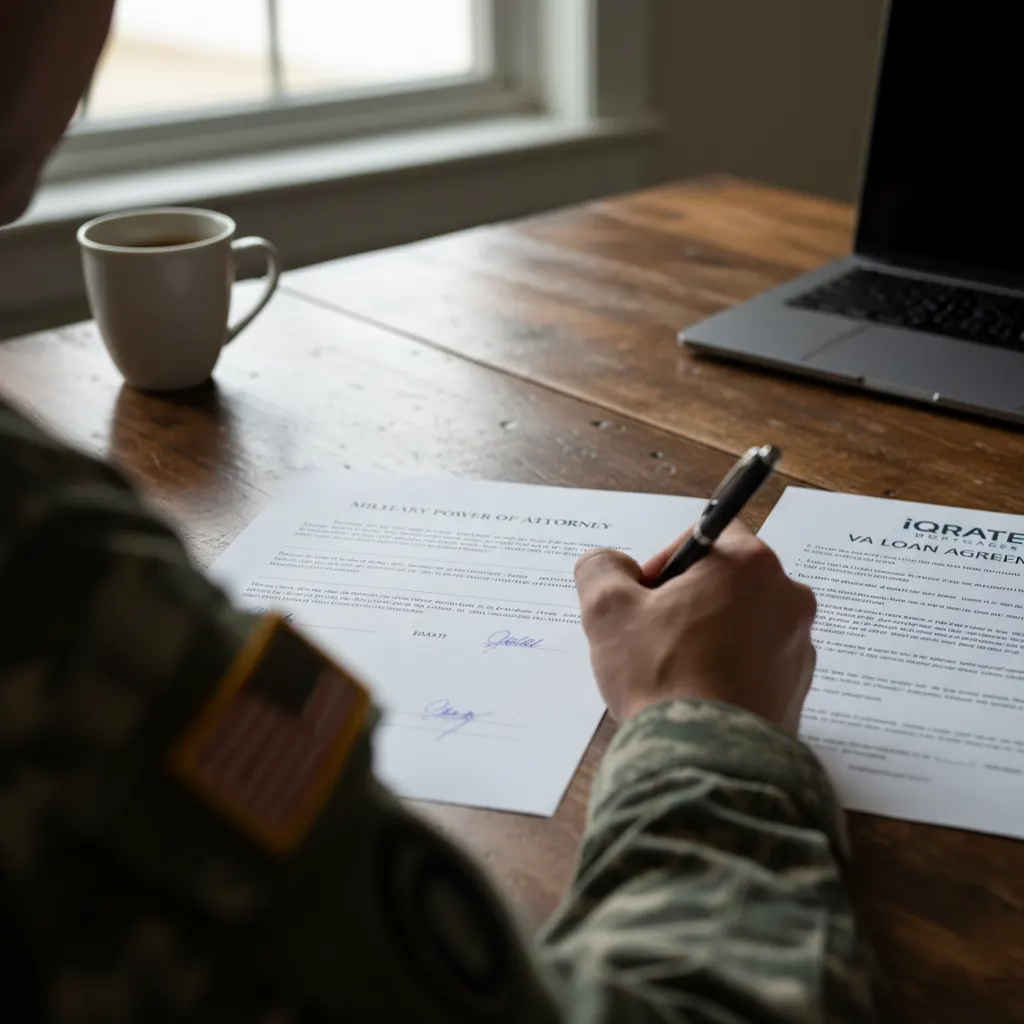

What is a military Power of Attorney and how is it used for closing?

A Power of Attorney (POA) is a legal document that grants a trusted individual, known as the 'attorney-in-fact', the authority to act on your behalf in specific matters. For a service member handling a remote home purchase, a POA is an indispensable tool.

There are two main types of POAs, but only one is suitable for a real estate transaction:

- General Power of Attorney: This grants broad authority to your attorney-in-fact to handle almost all your financial and legal affairs. Lenders and title companies generally reject these for home closings because they are too broad.

- Special Power of Attorney (also called a Specific or Limited POA): This is the document you need. It grants very specific, limited powers for a single purpose. For a home purchase, the Special POA must explicitly state the authority to execute documents related to the purchase of a specific property, often including the property address.

How to Use a POA for Your Remote Closing

The process is straightforward but requires precision. First, you must have the Special POA drafted, typically by a Judge Advocate General's (JAG) office on base, which is a free service for military members. The document must meet the legal standards of the State of Texas and the specific requirements of your lender and the title company. (The data, information, or policy mentioned here may vary over time.) Your lender will review and approve the POA language before closing. On closing day, your designated attorney-in-fact, often your spouse, will attend the signing and execute the final documents on your behalf.

Can my spouse handle the home purchase in San Antonio if I am deployed?

Yes, absolutely. This is one of the most common and effective ways to manage a PCS home purchase when the service member is deployed, TDY, or otherwise unavailable. With a properly executed Special Power of Attorney, your spouse can manage nearly every aspect of the transaction in San Antonio while you are away.

Your spouse can:

- Attend property showings and open houses.

- Make an offer on a home.

- Sign the purchase contract and initial disclosures.

- Attend the home inspection and negotiate any potential repairs.

- Conduct the final walk-through before closing.

- Sign all final closing documents, including the mortgage note and deed of trust.

For this process to work smoothly, communication is key. You and your spouse should be in constant contact, and your lender and real estate agent should be aware of the arrangement from the beginning. Providing them with a copy of the approved Special POA early in the process prevents last-minute delays.

How do I satisfy the VA loan occupancy rule if I have not arrived yet?

The VA loan program is designed for primary residences, meaning the veteran must intend to occupy the home within a 'reasonable time' after closing. The VA typically defines this as 60 days. This rule can cause anxiety for service members buying a home before a PCS, but the VA has built-in exceptions for active-duty personnel.

Your PCS orders are the key to satisfying this requirement. By providing a copy of your orders to the lender, you are formally certifying your intent to occupy the property as your primary residence upon your arrival at your new duty station. The 60-day clock does not start until you have officially reported for duty.

Furthermore, the VA offers another important allowance for military families. The occupancy requirement is considered met if your spouse moves into the home within the 60-day timeframe, even if your arrival is delayed. For instance, if you purchase a home near Fort Bliss in El Paso and your spouse moves in, but you are sent on a 30-day TDY immediately upon arrival, you are still in full compliance with VA rules. This flexibility is designed specifically to accommodate the unpredictable nature of military service.

What is the process for conducting a remote home inspection?

A home inspection is arguably one of the most critical steps in the homebuying process, and conducting it remotely requires a coordinated effort. Never skip the inspection just because you cannot be there in person.

Here is a reliable process for a successful remote inspection:

- Hire a Highly-Rated Inspector: Research and hire a licensed, insured, and well-reviewed home inspector in your target city, whether it is Killeen, El Paso, or San Antonio. Your real estate agent can provide recommendations, but be sure to check their online reviews and credentials yourself.

- Designate an On-Site Attendee: Your real estate agent or spouse (if they are already in the area) must attend the inspection. They will be your eyes and ears, able to ask the inspector questions and see potential issues firsthand.

- Request a Detailed Digital Report: Ensure the inspector's final report will include high-resolution photos of every issue, big or small. Many inspectors now include video walkthroughs of major systems (like HVAC and plumbing) or problem areas.

- Schedule a Post-Inspection Debrief: Arrange a video call with the inspector and your agent to review the report together. This allows you to ask detailed questions and get a better understanding of the severity of any findings. This step is crucial for making an informed decision about whether to proceed with the purchase, request repairs, or negotiate the price.

How can I manage the closing process from a different location?

When closing day arrives, you have several options for signing the final paperwork from afar. The best method depends on your location, your lender's policies, and title company capabilities.

Using a Special Power of Attorney (POA)

Process: As detailed earlier, your designated attorney-in-fact attends the closing in person and signs on your behalf. Pros: This is the most common, reliable, and widely accepted method for a remote military closing. It creates a smooth, traditional closing experience. Cons: It requires you to have a trusted individual available at the closing location.

Remote Online Notarization (RON)

Process: You connect with a notary via a secure video conferencing platform. You electronically sign the documents, and the notary digitally applies their seal. Texas is a RON-approved state. Pros: Highly convenient, allowing you to close from anywhere with an internet connection. Cons: Not all lenders and title companies have adopted the technology. You must confirm this is an option at the very beginning of the loan process. (The data, information, or policy mentioned here may vary over time.)

Mail-Away Closing

Process: The title company overnights the document package to you. You find a local notary (on base or at a U.S. embassy if overseas), sign the documents, and overnight them back. Pros: It works when other options are not available. Cons: This is the slowest and riskiest method. Shipping delays can jeopardize your closing date. Any small error, like a missed signature, requires resending the documents and can cause significant delays.

What documents should I prepare for a seamless remote VA loan approval?

Being organized is your best defense against delays. Having your documents gathered and ready to submit will streamline the underwriting process. Here is a checklist of what you will typically need:

Military-Specific Documents

Certificate of Eligibility (COE): Your lender can usually help you obtain this online in minutes.Copy of your Official PCS Orders: This confirms your relocation and timeline.Leave and Earnings Statements (LES): The most recent two months.Statement of Service: Only required if you are a newer service member; it is a letter from your commanding officer verifying your service details.

Standard Financial Documents

Government-Issued Photo ID: Driver's license or passport.W-2s and Tax Returns: The last two years of federal tax returns, including all schedules.Bank Statements: The last two months for all checking, savings, and investment accounts to verify assets for closing costs. (The data, information, or policy mentioned here may vary over time.)Approved Special Power of Attorney: If you plan to use a POA for closing.Divorce Decree or Child Support Orders: If applicable, to account for any alimony or child support payments. Navigating a PCS move and a VA loan requires expert coordination. If you have questions about using a POA or timing your remote closing in Texas, contact a mortgage specialist who understands the unique needs of military families.

Your PCS orders are your ticket to a new home. Let us help you navigate the VA loan process with expertise tailored to military families. Take the first step toward a smooth remote closing and Apply now.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References