Flood Insurance Requirements: FHA vs. Conventional

Buying a home in coastal Florida cities like Tampa or Naples means confronting the reality of flood zones. Lenders require flood insurance for properties in Special Flood Hazard Areas (SFHAs) to protect their investment, but the rules aren't the same for every loan. The type of mortgage you choose—Federal Housing Administration (FHA) or Conventional—dictates the type of insurance you can get, how much you need, and how you pay for it. Understanding these differences is critical to managing your long-term housing costs.

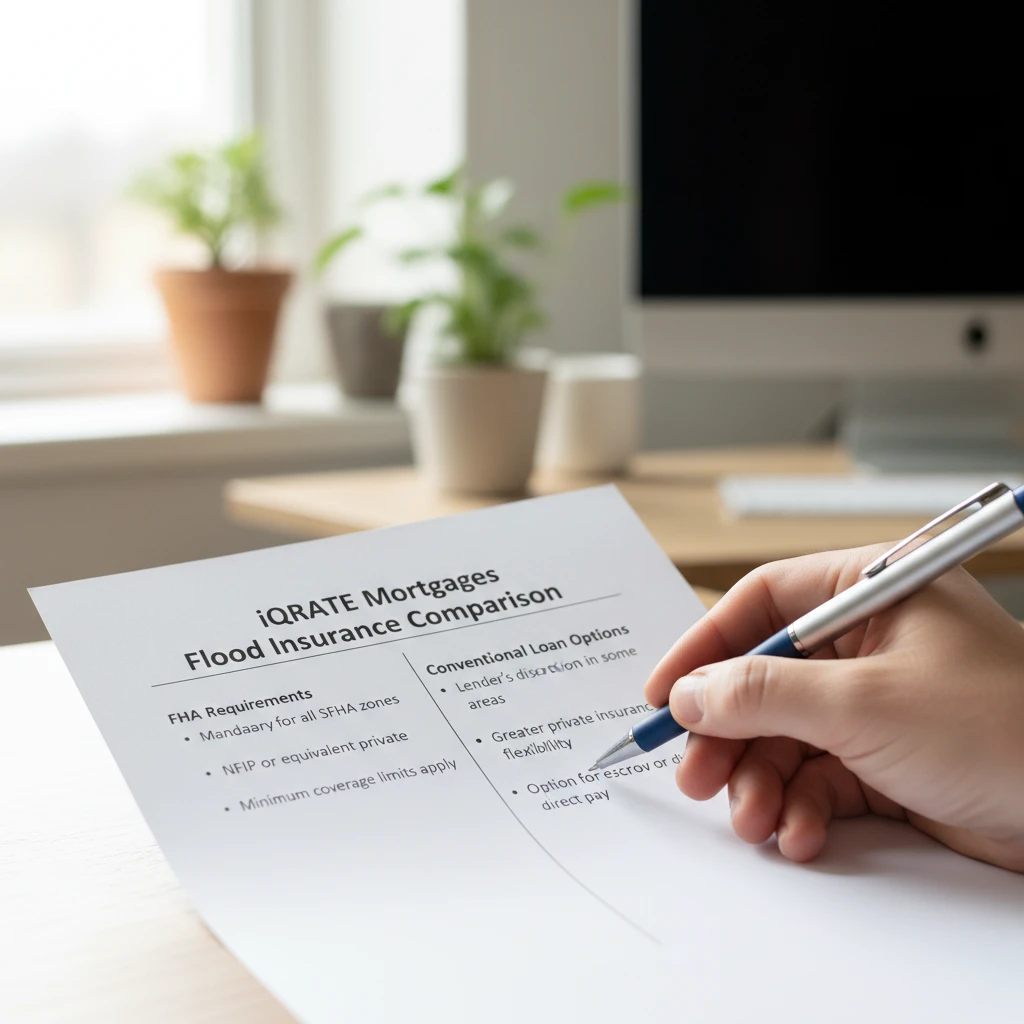

FHA Loan Minimum Flood Insurance Requirements

FHA loans are insured by the federal government, which means they must follow strict federal regulations regarding flood insurance. There is very little, if any, room for negotiation here. If the home you want to buy is in an SFHA as determined by the Federal Emergency Management Agency (FEMA), you must have flood insurance in place before closing.

- Coverage Amount: For an FHA loan, the required flood insurance coverage must be the lesser of these two amounts:

- The outstanding principal balance of the loan.

- The maximum coverage limit available from the National Flood Insurance Program (NFIP), which is currently $250,000 for the building/structure.

- Type of Insurance: Historically, FHA has almost exclusively required policies issued through the NFIP. While guidelines are slowly evolving to accept some private insurance, many FHA lenders still default to requiring an NFIP policy to guarantee compliance with HUD's strict standards. This can limit your ability to shop around for a better rate. (The data, information, or policy mentioned here may vary over time.)

- Unwavering Mandate: This requirement is absolute. If you cannot secure the necessary NFIP coverage for a property in Tampa, you will not be able to close on your FHA loan.

Are Conventional Loan Flood Rules More Flexible in Naples?

Yes, conventional loans generally offer more flexibility. These loans are not government-insured; instead, they must conform to the guidelines set by Fannie Mae and Freddie Mac. While they also mandate flood insurance for properties in an SFHA, their rules are often more accommodating, which can be a significant advantage for a buyer in a high-cost area like Naples.

- Acceptance of Private Insurance: The biggest difference is that conventional loans readily accept private flood insurance policies. As long as the private policy provides coverage that is 'at least as broad as' an NFIP policy and meets specific lender requirements for the insurer's financial strength, it's typically approved. The private market in Florida is competitive, and you may find a policy that offers equal or better coverage for a lower premium.

- Coverage Requirements: The coverage amount rules are similar to FHA—the lesser of the loan balance or the maximum NFIP limit. However, the flexibility to use a private policy means you might find options with higher coverage limits if needed, exceeding the NFIP's $250,000 cap.

- Deductible Options: Conventional lenders may allow for higher deductibles on a flood insurance policy compared to what's standard with the NFIP. Choosing a higher deductible can substantially lower your annual premium, though it means a higher out-of-pocket cost if you ever file a claim. (The data, information, or policy mentioned here may vary over time.)

Calculating the Financial Impact on Your Mortgage

Flood insurance isn't just a checkbox on a closing document; it's a significant monthly expense that directly impacts your loan qualification and budget. The annual premium is divided by 12 and added to your total monthly housing payment, which includes your principal, interest, property taxes, and homeowner's insurance (PITI).

How Flood Insurance Premiums Affect Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is the cornerstone of mortgage approval. It's calculated by dividing your total monthly debt payments (including your proposed housing payment) by your gross monthly income. Lenders use it to assess your ability to manage your payments.

Let's use a realistic example for a home in Tampa:

- Gross Monthly Income: $7,000

- Proposed Mortgage (P+I+T+I): $2,200

- Other Debts (Car loan, credit cards): $600

- Annual Flood Insurance Premium: $3,600

The flood insurance premium adds $300 ($3,600 / 12) to your monthly housing expense.

- Total Monthly Debt without Flood Insurance: $2,200 + $600 = $2,800

- DTI without Flood Insurance: $2,800 / $7,000 = 40%

Now, let's add the flood insurance:

- Total Monthly Debt with Flood Insurance: $2,200 + $600 + $300 = $3,100

- DTI with Flood Insurance: $3,100 / $7,000 = 44.2%

While this 44.2% DTI is above older, traditional limits, it would likely still be acceptable for many borrowers. FHA loans, with approval from an automated underwriting system, can often accommodate DTI ratios up to 56.99%. (The data, information, or policy mentioned here may vary over time.) Similarly, conventional loans can frequently be approved with DTI ratios up to 50% under current guidelines. (The data, information, or policy mentioned here may vary over time.) However, a lower DTI is always stronger, and a high flood insurance premium can still be the deciding factor between approval and denial, especially if other risk factors are present.

Can I Pay Flood Insurance Outside of My Escrow Account?

The answer depends entirely on your loan type and down payment.

- FHA Loans: No. FHA loans require an escrow account for the life of the loan. Your lender will collect funds for property taxes, homeowner's insurance, and flood insurance with every monthly mortgage payment and pay the bills on your behalf. There is no option to opt-out.

- Conventional Loans: Maybe. If you make a down payment of at least 20% (meaning your loan-to-value ratio is 80% or less), you can typically request to waive the escrow account. (The data, information, or policy mentioned here may vary over time.) This would allow you to pay your flood insurance premium directly to the insurance company in one lump sum annually. While this gives you more control over your funds, it also means you are responsible for saving and making a large payment on time. Failure to do so could put you in default on your mortgage terms.

Strategies for Managing Flood Insurance Costs

Since flood insurance is mandatory and can be expensive, finding ways to manage the cost is crucial. Your choice of loan program plays a direct role in the strategies available to you.

Which Loan Type Allows Higher-Deductible Policies?

Conventional loans are the clear winner here. Because they accept private flood insurance, you gain access to a wider range of policy structures. A private insurer might offer a policy with a $5,000 or $10,000 deductible, which could lower your annual premium by hundreds of dollars compared to the standard $1,000 or $2,000 deductible common with NFIP policies. This gives you the power to assume a bit more risk in exchange for a lower, more manageable monthly mortgage payment.

FHA loans, typically tied to NFIP policies, offer very limited deductible options. You have far less ability to customize the policy to reduce your premium, making your costs more fixed and often higher.

Does Private Flood Insurance Meet Both Loan Requirements?

This is a critical distinction, especially in a competitive insurance market like Florida.

- Conventional Loans: Yes, absolutely. As mentioned, Fannie Mae and Freddie Mac have clear guidelines for accepting private flood insurance. As long as the policy is from a reputable, financially sound insurer and provides coverage equivalent to an NFIP policy, it is generally accepted. This is the single greatest advantage for a conventional borrower in a Naples or Tampa flood zone.

- FHA Loans: It's complicated. While HUD (which oversees the FHA) issued a final rule to begin accepting private flood insurance, its implementation at the lender level has been slow and inconsistent. Many lenders still prefer or require an NFIP policy for FHA loans to avoid any compliance issues. You should not assume you can use private insurance with an FHA loan; you must confirm with your specific lender, and many will still say no. (The data, information, or policy mentioned here may vary over time.)

Long-Term Considerations for Flood Zone Properties

The flood risk of your property isn't static. FEMA continuously updates its Flood Insurance Rate Maps (FIRMs), which can change your insurance obligations overnight.

What Happens if Tampa Flood Maps Are Redrawn?

Flood map revisions can impact any homeowner, regardless of their mortgage type.

- Mapped Into an SFHA: If your Tampa property was not in an SFHA when you bought it but is later remapped into one, your lender will notify you that you are now required to obtain flood insurance. You will be given a deadline to secure a policy. If you fail to do so, the lender will 'force-place' an expensive policy on your behalf and bill you for it through your escrow account.

- Mapped Out of an SFHA: If your property is remapped out of a high-risk zone, you may no longer be federally required to carry flood insurance. You could cancel your policy and remove that expense from your monthly payment. However, given Florida's weather patterns, most financial advisors recommend keeping a lower-cost, preferred-risk policy for protection, as more than 20% of all flood claims occur outside of high-risk zones. Buying a home in a Tampa or Naples flood zone involves more than just picking a loan. To understand how flood insurance costs will specifically affect your monthly payment and overall approval, it's best to review your options with a mortgage expert who understands Florida's unique insurance market.

Understanding how flood insurance impacts your loan options is the first step. To get a clear picture of your qualifications and confidently navigate the Florida market, Apply now for a personalized mortgage assessment.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

FEMA - National Flood Insurance Program