Why Standard Lenders Reject Seemingly Perfect Properties

In the competitive real estate markets of Miami and Naples, a listing with a unique complication can quickly become a dead end. Standard lenders and large banks operate on a model of minimizing risk, which means adhering strictly to guidelines set by government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac. Any deviation from these rigid standards triggers an automatic denial, regardless of the property's desirability or the buyer's qualifications.

These rejections often stem from issues that seem minor to a seller or agent but represent significant liability to a lender. The core reason is saleability on the secondary market. Lenders bundle conforming loans and sell them to investors. A loan for a property with a non-compliant feature cannot be included in these bundles, forcing the lender to hold it on their own books—a risk they are rarely willing to take.

Common reasons for rejection include:

- Non-Warrantable Condo Status: A condominium project in Miami might be flagged as non-warrantable if one owner holds more than 10% of the units, a single entity (like a hotel) owns commercial space exceeding 35% of the total square footage, or the HOA is involved in active litigation. Even if the lawsuit is minor, it's an immediate red flag for conventional underwriting.

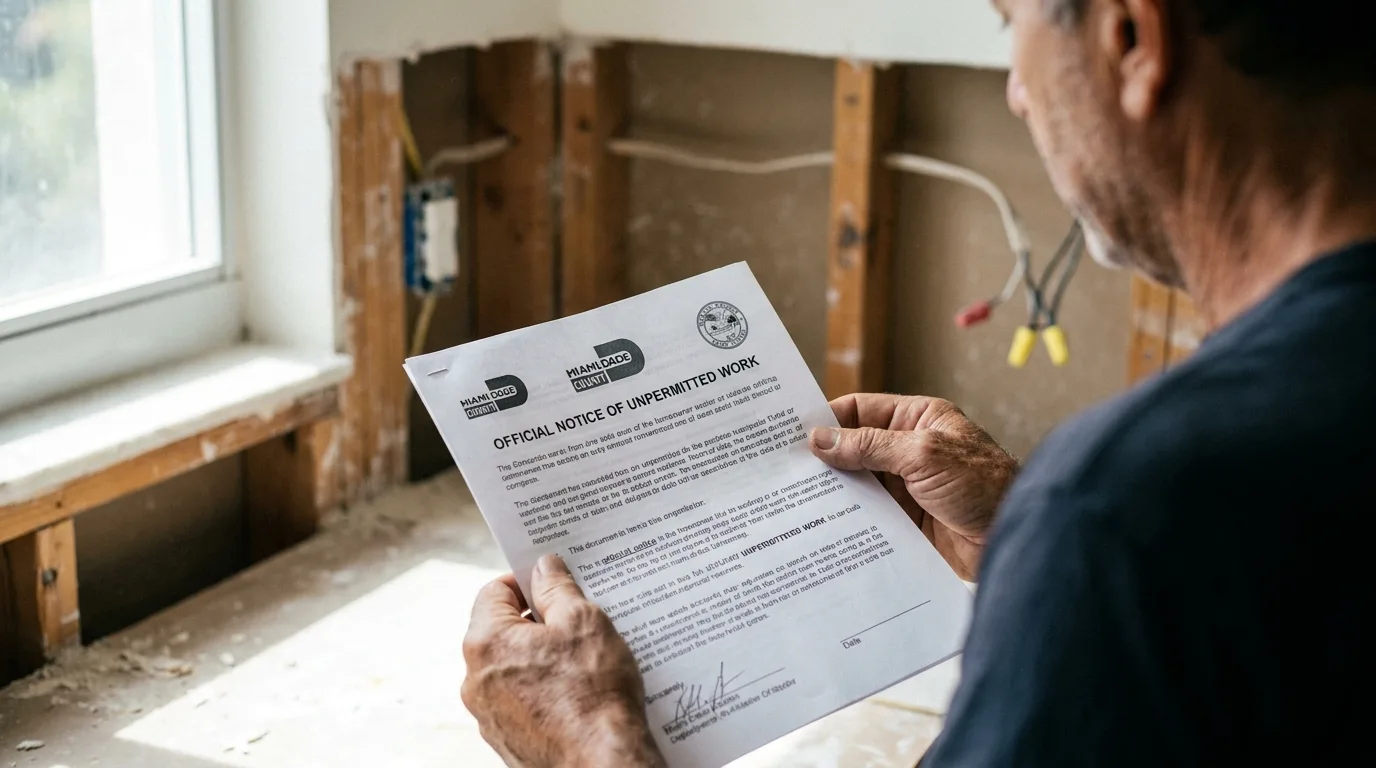

- Unpermitted Additions or Renovations: A beautifully renovated kitchen or an added Florida room becomes a liability if the work was done without proper permits. Lenders see this as a potential safety hazard, a code violation that could result in fines or mandated removal, and an issue that clouds the property's title and appraised value.

- Unique Legal Structures: Properties held in a trust, part of a co-op, or having unusual deed restrictions can complicate the lending process beyond the scope of a standard loan officer's expertise and their bank's narrow guidelines.

- Deferred Maintenance or Structural Concerns: While some issues are cosmetic, things like an aging roof nearing the end of its insurable life or evidence of past water intrusion can lead a lender to deny financing until repairs are completed, which sellers are often unwilling or unable to do upfront.

What is a Pre-Listing Finance Audit?

A Pre-Listing Finance Audit is a proactive strategy that flips the traditional real estate model on its head. Instead of waiting for a buyer’s lender to discover a problem at the eleventh hour, this audit identifies and solves financing hurdles before the property is even listed. It is a comprehensive analysis of a property's financial, legal, and physical health to engineer a specific, viable financing path that can be offered alongside the listing.

This audit is far more than a simple pre-qualification; it’s a deep dive into the property itself. The process meticulously analyzes:

- Condominium Documents & HOA Health: The audit team scrutinizes the condo questionnaire, budget, reserve funds, and meeting minutes. The goal is to identify red flags like insufficient reserves, high delinquency rates, or pending special assessments. For a high-rise in Naples, this could mean catching a planned concrete restoration project that would otherwise halt a conventional loan.

- Permit and Zoning Records: We pull municipal records to verify that all additions, renovations, and major system upgrades were properly permitted. If unpermitted work is found, the audit outlines the exact steps and documentation needed to resolve it for lending purposes.

- Title and Survey Examination: The audit examines the title history for any liens, encroachments, or easements that could complicate a transfer of ownership and secure a loan against the property.

- Property Condition and Insurability: The physical state of the property is assessed to ensure it meets the general collateral standards for a network of specialized lenders. This includes checking the age and condition of the roof, electrical systems, and plumbing to avoid last-minute insurance denials or underwriting conditions.

By completing this work upfront, a property's biggest liability is transformed into a powerful marketing asset: a pre-certified, ready-to-finance solution.

How to Market a 'Pre-Certified' Financing Solution in the MLS

Once the Pre-Listing Finance Audit is complete and a specific loan solution is engineered, you have a powerful tool to differentiate your listing. Marketing this advantage effectively is key to attracting the right buyers and agents, reducing market time, and securing a stronger negotiating position. The goal is to communicate confidence and eliminate uncertainty.

Here’s how to strategically position your pre-vetted property in the MLS and other marketing channels:

- Use Strategic Language in Public Remarks: Instead of leaving the financing to chance, you can make a bold statement. Your public remarks in the MLS can include phrases like:

- 'Financing solution pre-vetted for this property. Ask for details.'

- 'Unique property with financing secured. Don't let your buyer's bank say no.'

- 'Non-warrantable condo? No problem. We have a lender ready for this specific unit.'

- Add Detailed Notes in Broker Remarks: The broker-to-broker remarks section is the perfect place for more direct information. You can be specific about the solution:

- 'Seller has arranged a Pre-Listing Finance Audit. Portfolio loan with XYZ terms available for qualified buyers. This property will not qualify for conventional financing. Contact listing agent for lender contact.'

- 'Unpermitted addition has been cleared with our lending partner. All necessary documentation is on file to ensure a smooth closing.'

- Create a 'Financing Fact Sheet': Prepare a one-page PDF that can be attached to the MLS listing or emailed to interested agents. This document should briefly explain the challenge (e.g., HOA litigation) and the solution (e.g., approved by a specific portfolio lender). It provides tangible proof and saves the buyer's agent hours of fruitless searching for a lender.

This proactive approach completely changes the conversation. Agents with buyers who have been previously rejected for similar properties will see your listing as a golden opportunity, not a headache.

Which Loan Products Solve for Complex Florida Properties?

Conventional loans are not the only option. A key part of the Pre-Listing Finance Audit is matching the property's specific issue to a lender and loan product designed to handle it. Here are the primary solutions for common financing roadblocks in markets like Miami and Naples.

Non-Warrantable Condos or HOA Litigation

When a condo project doesn’t meet Fannie Mae or Freddie Mac guidelines, it is deemed 'non-warrantable'. This is where portfolio loans become essential. A portfolio loan is funded by a bank or private lender and held on their own books (their 'portfolio') rather than being sold on the secondary market. This gives them the flexibility to set their own underwriting rules.

- Key Features: These lenders look at the deal holistically. If the HOA is in a lawsuit over a minor slip-and-fall, but the project is financially sound with strong reserves, a portfolio lender can approve the loan. They can overlook issues like high investor concentration or a single entity owning multiple units. They often require a slightly higher down payment (e.g., 20-25%) and may have a marginally higher interest rate, but they make the deal possible. (The data, information, or policy mentioned here may vary over time.)

Navigating Mortgages with Unpermitted Work

An unpermitted addition is a major underwriting obstacle because it raises questions about safety, value, and legal compliance. To clear this for a loan, an underwriter needs to be satisfied that the work is safe and does not negatively impact the property's marketability. The required documentation typically includes:

- An 'As-Is' Appraisal: The appraiser must be made aware of the unpermitted work. They will be asked to value the home 'as-is' and determine what, if any, value the unpermitted space contributes. In many cases, they will give it zero value, and the loan will be based on the legally permitted square footage.

- A Hold-Harmless Agreement: The borrower may need to sign an agreement stating they acknowledge the unpermitted space and will not hold the lender liable for any future issues related to it.

- Evidence of Safety and Craftsmanship: In some cases, a report from a licensed contractor or structural engineer confirming the addition is structurally sound and built to a reasonable standard can help satisfy the underwriter. The best-case scenario is obtaining an after-the-fact permit from the municipality, which resolves the issue completely.

How a Pre-Vetted Property Solution Increases Seller Negotiation Leverage

Knowledge is power in negotiations. By solving the financing equation before listing, a seller fundamentally shifts the balance of power. Buyers lose their most common and potent negotiation tool: the financing contingency. When a property is presented with a pre-certified financing solution, it gives the seller significant leverage.

- Eliminates 'Financing Risk' Discount: Buyers often make lower offers on properties with known issues, factoring in the risk that their loan will be denied. A pre-vetted solution removes this risk, justifying a full-price offer. The property is no longer 'distressed' or 'complicated'; it is a straightforward transaction.

- Strengthens Response to Lowball Offers: A seller can confidently reject low offers, knowing their property is accessible to a wider pool of qualified buyers, not just cash purchasers who typically expect a steep discount.

- Attracts Multiple, Confident Offers: When buyer agents see that the financing hurdle has been cleared, they can write offers with more confidence. This can lead to multiple-offer situations, driving the final sale price up and giving the seller the ability to choose the offer with the best terms.

What Is the Process for Transferring the Financing Solution?

The transfer process is designed to be seamless and collaborative. The listing agent’s role is to act as the bridge, connecting the buyer’s agent to the pre-vetted financing path. There is no complex handoff or transfer of legal documents. The process is simple:

- Introduction: Once an offer is accepted, the listing agent provides the buyer’s agent with the contact information for the mortgage strategist who performed the audit.

- Buyer Qualification: The buyer then applies for the loan directly with the designated mortgage professional. It's crucial to understand that while the property is pre-approved, the buyer must still meet the standard financial qualifications for the loan (credit, income, assets).

- Streamlined Underwriting: Because all the property-related documentation (condo docs, permit records, etc.) has already been gathered and approved, the underwriting process is significantly faster. The focus is solely on the buyer's financial profile, dramatically reducing the chance of last-minute property-related snags.

How This Strategy Reduces a Listing's Days on Market

Days on market (DOM) is a critical metric for any real estate agent. A listing that sits for too long becomes stale, attracts lowball offers, and damages both the seller's equity and the agent's reputation. The Pre-Listing Finance Audit strategy directly attacks the primary causes of inflated DOM.

- Wider Buyer Pool: Instead of being limited to cash buyers, the property is now open to any buyer who can qualify for the engineered loan solution. This instantly increases demand.

- Fewer Dead Deals: The number one reason contracts fall apart is financing. By solving this upfront, the likelihood of a deal collapsing in underwriting drops to nearly zero. This avoids the devastating process of putting a property back on the market after a failed sale, which adds weeks or even months to the DOM.

- Increased Urgency: A property with a clear, easy financing path is more attractive. Buyers and their agents recognize a smooth transaction when they see one, creating more urgency to submit an offer before someone else does. For a unique property in a fast-paced market like Miami, this can mean the difference between selling in 10 days versus 90.

If you're facing a complex property scenario, a proactive financing audit can transform a potential dead end into a done deal. Ready to explore a tailored mortgage solution that ensures a smooth closing? Apply now to unlock your property's true market potential.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

Fannie Mae Condominium Project Standards