Sourcing Foreign Funds for a Miami Jumbo Loan

Purchasing a luxury property in vibrant Florida cities like Miami or Palm Beach with a jumbo loan presents a unique challenge for international buyers: proving the source of your down payment. United States lending institutions operate under stringent federal regulations, including the Bank Secrecy Act (BSA), designed to prevent money laundering. This means every dollar originating from outside the U.S. is subject to intense scrutiny. For an underwriter, an undocumented, large sum of money appearing in an account is a major red flag that can halt your application.

This guide provides a clear roadmap for sourcing, seasoning, and transferring foreign funds. Following these steps ensures your financial documentation is pristine, helping you secure a jumbo loan without unnecessary delays or rejection.

Proving the Source of Foreign Funds: Required Documents

Lenders require a comprehensive and transparent paper trail. The goal is to show a legitimate and legal origin for every dollar being used for your down payment and closing costs. Ambiguity is the enemy of approval.

Key Documents for Sourcing Foreign Funds

- Bank Statements: You will need to provide at least two to three months of statements from both the foreign bank account where the funds originated and the U.S. bank account where they were deposited. These statements must show your name and the account number.

- Certified Translations: All documents not in English must be translated by a certified, independent third party. The translator must provide a letter certifying the accuracy of the translation.

- Letter of Explanation (LOX): A detailed letter explaining the source of the funds. For example, if the funds are from the sale of a property, you would explain that and provide the corresponding sales contract.

- Proof of Asset Sale: If your down payment comes from selling an asset like real estate or stocks, you must provide the fully executed sales contract, closing statement (like a HUD-1 or equivalent), and proof of the funds being deposited into your account.

- Business Financials: If funds are from a business, provide tax returns, profit and loss statements, and a letter from your accountant verifying the withdrawal will not negatively impact the business operations.

- Wire Transfer Receipts: A complete record of the wire transfer from the foreign institution to the U.S. institution. (The data, information, or policy mentioned here may vary over time.)

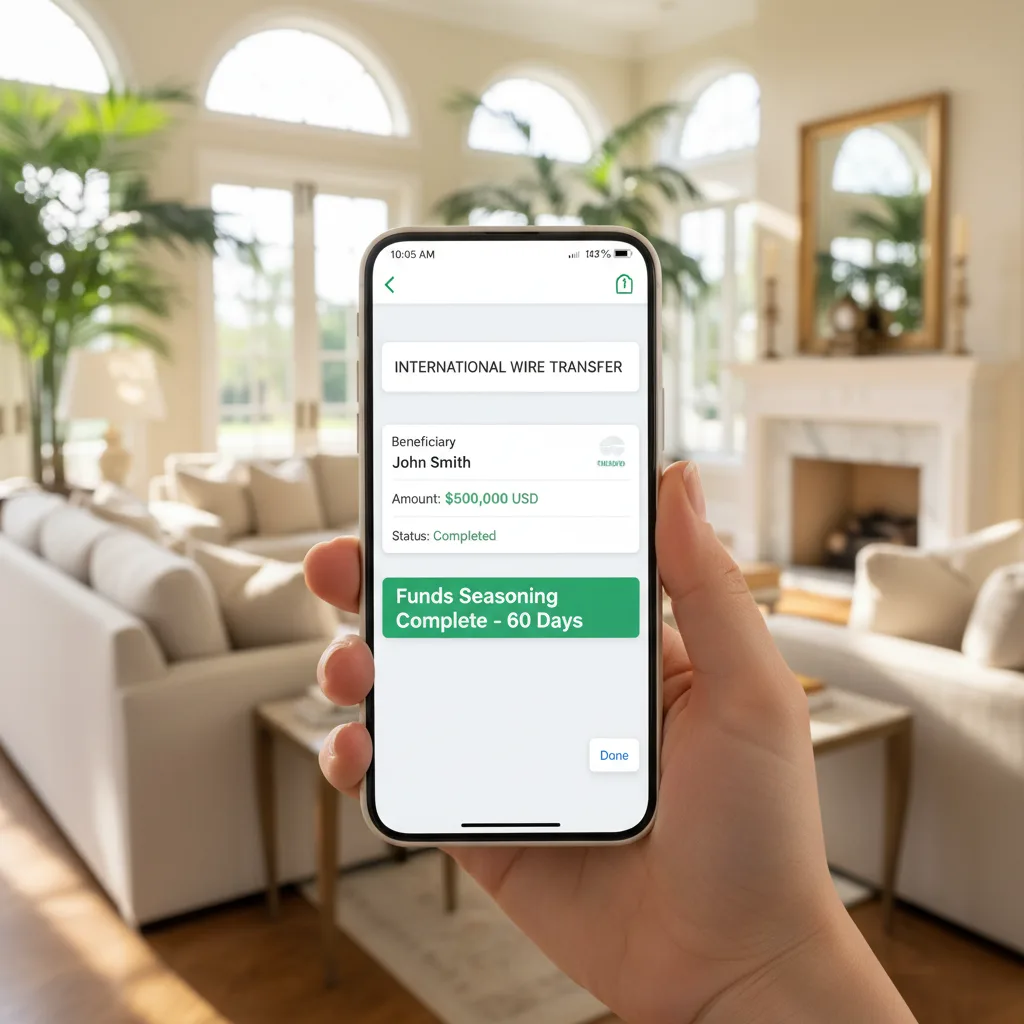

The Seasoning Period for Foreign Funds in U.S. Banks

'Seasoning' is the period funds must sit in a U.S. bank account before they can be used for a mortgage transaction. This process demonstrates to the lender that the funds are yours and are not from an unapproved source or a last-minute loan.

For most jumbo loans, the standard seasoning period is 60 to 90 days. Lenders will typically require the last two full bank statements. If your funds have been in your U.S. account for that duration, they are considered 'seasoned', and the sourcing requirements are significantly less intensive. However, if you transfer a large sum just before applying for a loan, you must be prepared to source the origin of those funds with the documents listed above. For a property in a high-value market like Palm Beach, underwriters will be especially meticulous about funds that appear unseasoned. (The data, information, or policy mentioned here may vary over time.)

Documenting an International Wire Transfer

Documenting the wire transfer is a critical step in creating the necessary paper trail. It connects the money leaving your foreign account to the money arriving in your U.S. account. The process must be transparent and meticulously recorded.

Step-by-Step Wire Transfer Documentation

- Obtain Wire Instructions: Get the official wire transfer instructions from your U.S. bank. Ensure the receiving account is in your name.

- Initiate the Transfer: When you send the wire from your foreign bank, obtain a detailed receipt. This receipt should show the sending bank's information, your name and account number, the receiving bank's information, and the exact amount sent in both the foreign currency and its U.S. dollar equivalent on that day.

- Confirm Receipt: Once the wire arrives in your U.S. account, get a confirmation receipt from the receiving bank. This document proves the funds landed successfully.

- Provide Both Receipts to Your Lender: Submit both the sending and receiving wire transfer receipts to your mortgage lender. This creates an unbroken chain of evidence for the underwriter.

Using Funds from a Foreign Business for Your Down Payment

Yes, you can use funds from a foreign business you own, but expect an even deeper level of scrutiny. Lenders need to confirm two things: that you have legal access to the funds and that the withdrawal will not destabilize the company, which could impact your future income and ability to repay the loan.

Documentation for Business-Sourced Funds

- Proof of Ownership: Documents showing you own the business and have the authority to withdraw funds.

- Business Financial Statements: Typically, the last two years of profit and loss statements and balance sheets, translated and certified.

- Accountant's Letter: A letter from the company's chartered accountant confirming that the withdrawal of funds is considered a distribution or dividend and will not adversely affect the business's financial health. This is a critical piece of evidence for the underwriter.

- Business Bank Statements: Statements showing the funds leaving the business account. (The data, information, or policy mentioned here may vary over time.)

Managing Currency Exchange Fluctuations

Currency exchange rates are constantly changing, which introduces a significant risk to your transaction. The U.S. dollar amount you need for your down payment and closing costs is fixed, but the value of your foreign currency is not. A sudden drop in your home currency's value could leave you short of the required funds at closing.

To mitigate this risk, it is highly advisable to transfer more money than you need. A safe buffer is typically 5% to 10% above the total required amount. For example, if you need $750,000 USD for your down payment and closing costs on a Miami Beach condo, you should consider transferring approximately $785,000 to $825,000 USD. This extra amount covers potential currency fluctuations and any intermediary bank fees associated with the wire transfer. Any excess funds can simply remain in your U.S. account after closing.

Common Underwriting Red Flags for Foreign Assets

Underwriters are trained to spot inconsistencies and potential risks. Avoiding these red flags will streamline your approval process.

- Large, Unexplained Deposits: Any large deposit that is not your regular income must be sourced. A sudden deposit of $100,000 without a clear paper trail is the biggest red flag.

- Commingled Funds: Using a business account for personal expenses or having funds transferred from multiple, unrelated third parties can complicate the sourcing process.

- Inconsistent Information: Names, addresses, or dates that do not match across your application, bank statements, and supporting documents.

- Funds from OFAC-Sanctioned Countries: Attempting to source funds from countries on the U.S. Office of Foreign Assets Control (OFAC) sanction list will result in an automatic denial.

- Rapid Asset Movement: Moving money through several different accounts in a short period before transferring it to the U.S. can look like an attempt to obscure the original source.

Documenting a Financial Gift from a Foreign Relative

Using a financial gift from a foreign relative is permissible, but it requires precise documentation from both you and the donor. The lender must be certain it is a true gift and not a disguised loan that you will have to repay.

Gift Fund Documentation Protocol

- The Gift Letter: This is a formal letter signed by the donor. It must include:

- The donor's name, address, and relationship to you.

- The exact dollar amount of the gift.

- A clear statement that the funds are a gift and there is no expectation of repayment.

- The date the funds were transferred.

- Proof of Donor's Ability to Give: The donor must provide their own bank statements showing they had the funds available to give without taking out a loan.

- The Paper Trail: You need to document the transfer of funds from the donor’s account to your account. This includes the donor's wire transfer receipt and the deposit receipt showing the funds arriving in your U.S. account. Every step must be documented. Navigating the complexities of foreign-sourced funds for a jumbo loan requires expert guidance. If you're planning a purchase in Miami or anywhere in Florida, partnering with a mortgage strategist who understands these unique challenges can be the difference between approval and denial.

When you're ready to navigate the complexities of a jumbo loan with confidence, take the first step toward securing your Florida property. Apply now to partner with our experts and build a clear plan for a successful closing.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

Fannie Mae Selling Guide: Asset Documentation

Financial Crimes Enforcement Network (FinCEN) - Bank Secrecy Act

Consumer Financial Protection Bureau (CFPB) - Mortgage Closing Process