Common Misleading VA IRRRL Advertisements

As a veteran homeowner, you've likely seen the mailers and online ads. They arrive with a sense of urgency, often decorated with official-looking seals, promising to lower your mortgage payment through a VA Interest Rate Reduction Refinance Loan (IRRRL). While the VA IRRRL program is a legitimate and valuable benefit, many lenders use misleading tactics to sell refinances that primarily benefit them, not you.

Here are the most common red flags to watch for in advertisements targeting homeowners in Miami and beyond:

- 'Skip a Payment (or Two)': This is a classic bait-and-switch. You are not skipping payments for free. The interest that accrues during those months is added to your new loan principal. You end up paying interest on that interest for the life of the new loan.

- 'No Out-of-Pocket Costs': This phrase is technically true but highly deceptive. It simply means the closing costs are rolled into your new loan balance, not that they don't exist. This increases your total debt and reduces your home equity.

- 'Government-Required Refinance': No government agency will ever require you to refinance your mortgage. These claims use official-sounding language to create a false sense of obligation and are a major red flag.

- 'Extremely Low Interest Rates': Ads often feature teaser rates that are only available to borrowers with perfect credit and require paying expensive 'discount points'. The rate you are actually offered may be significantly higher.

- 'Cash Out Offers Disguised as IRRRLs': An IRRRL is strictly for reducing your interest rate and payment. If a lender offers you cash back at closing, it is not a true IRRRL. It is a cash-out refinance, which has different requirements and implications for your equity.

Calculating the True Cost of a 'No-Cost' Refinance

The term 'no-cost' refinance is a marketing gimmick. There are always costs associated with originating a new mortgage, including lender fees, title insurance, and government funding fees. In a 'no-cost' IRRRL, these fees are financed into the new loan.

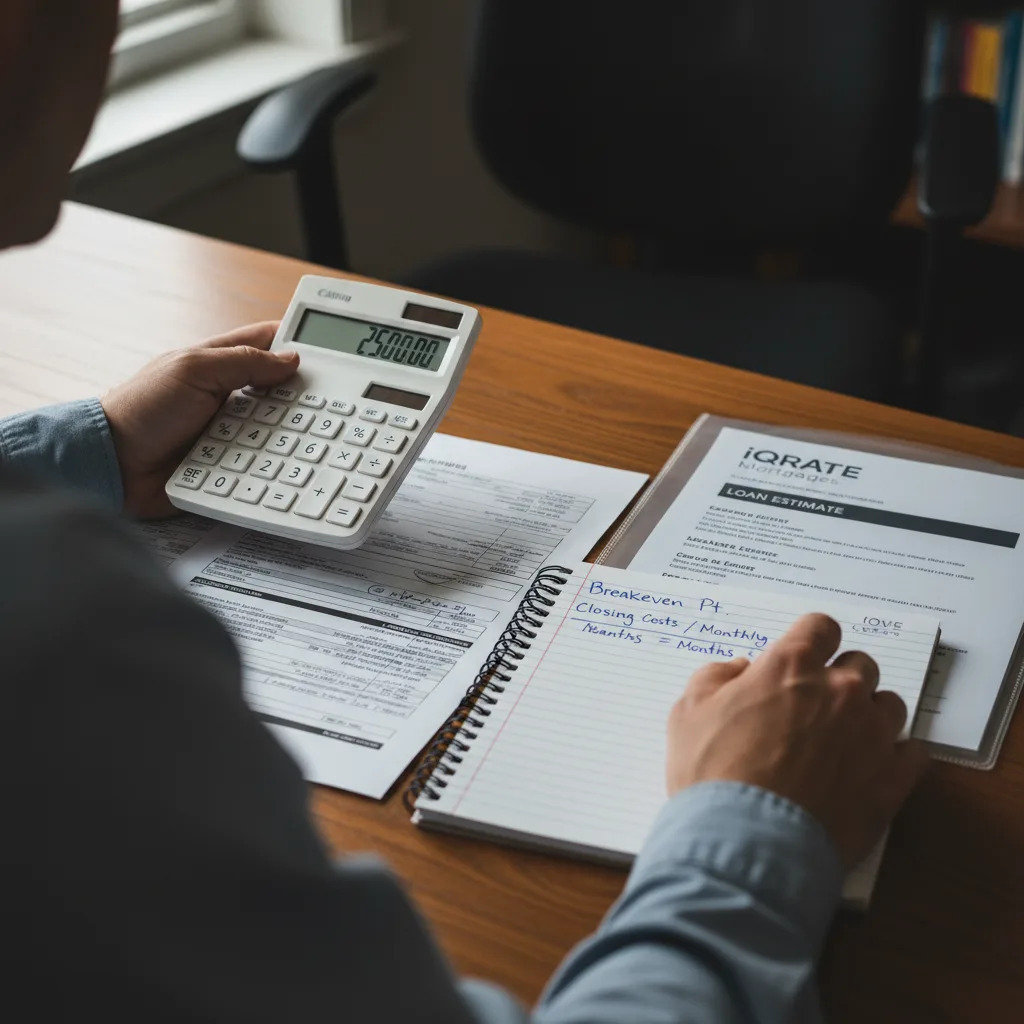

To understand the true cost, you must calculate your recoupment period, also known as the breakeven point. This is the number of months it will take for your monthly savings to cover the total closing costs.

The Recoupment Period Formula

- Find Total Closing Costs: Look at your Loan Estimate. This includes the VA Funding Fee, origination fees, appraisal fees (if any), title charges, and any discount points. Let's say the total is

$7,500. (The data, information, or policy mentioned here may vary over time.) - Calculate Monthly Savings: Compare the principal and interest (P&I) payment on your current loan to the proposed P&I payment on the new loan. Let's say your current payment is

$2,200and the new payment is$2,000. Your monthly savings are$200. - Divide Costs by Savings:

Total Closing Costs / Monthly Savings = Recoupment Period in Months

Using our example: $7,500 / $200 = 37.5 months.

It would take you 37.5 months, or just over three years, just to break even on the cost of this refinance. If you plan to sell your home in Orlando within that timeframe, you will lose money on the deal.

When the Rate Reduction Doesn't Justify the Fees

The entire purpose of an IRRRL is for the veteran to receive a tangible financial benefit. The VA has specific rules about this, known as the 'Net Tangible Benefit Test'. However, a loan can meet the legal minimum requirement and still be a poor financial decision for you.

Reject the offer if the numbers show a weak benefit:

- The Recoupment Period is Too Long: A general rule of thumb is that if you can't recoup the closing costs within 24 to 36 months, the refinance may not be worth it. The longer the period, the higher the risk that you'll sell or refinance again before you've realized any actual savings.

- The Interest Rate Drop is Minimal: Shaving just 0.25% off your rate might not produce enough monthly savings to justify thousands of dollars in new closing costs. For a homeowner in Miami with a

$450,000loan balance, a 0.25% rate reduction saves only about$70per month. If the closing costs are$7,000, the recoupment period is 100 months, or over eight years. (The data, information, or policy mentioned here may vary over time.) - You're Paying for Discount Points: Lenders may charge 'discount points' to buy down the interest rate. One point costs 1% of the loan amount. If a lender is charging you points to achieve the advertised rate, it dramatically increases your upfront costs and extends your breakeven point.

Spotting Hidden Fees on the Loan Estimate

The Loan Estimate (LE) is a standardized three-page document that outlines the terms of the loan offer. You must review it meticulously. Don't just look at the payment; look at the costs. (The data, information, or policy mentioned here may vary over time.)

Key Sections to Scrutinize:

- Section A: Origination Charges: This is what the lender charges for creating the loan. It can include an origination fee, application fee, and discount points. Question any fee that seems excessive. While a 1% origination fee is common, some lenders try to add other 'junk' fees.

- Section B: Services You Cannot Shop For: These are required third-party services, like an appraisal or credit report fee. For an IRRRL, an appraisal is typically not required, so seeing a fee here is a red flag.

- Section E: Taxes and Other Government Fees: This section includes the VA Funding Fee. For an IRRRL, this fee is 0.5% of the loan amount. Ensure it is calculated correctly. Veterans receiving VA disability compensation are exempt from this fee.

- Page 2, 'Loan Costs' vs. 'Cash to Close': This section shows the total costs being added to your loan. Compare the 'Total Loan Costs' to the 'Estimated Cash to Close'. If 'Cash to Close' is zero or a small number, it confirms that all those costs are being rolled into your new, higher loan balance.

How an IRRRL Can Negatively Impact Your Home Equity

Home equity is the difference between your home's value and your mortgage balance; it's a critical component of your personal wealth. Every time you refinance and roll the closing costs into the loan, you increase your debt and decrease your home equity.

Example:

- Your home in Orlando is valued at

$400,000. - Your current VA loan balance is

$320,000. - Your current equity is

$80,000.

An IRRRL offer includes $8,000 in closing costs that are rolled into the loan. Your new loan balance becomes $328,000. Instantly, your home equity drops from $80,000 to $72,000.

This might not seem drastic, but it sets you back on your journey to owning your home free and clear. If you do this every few years, a practice known as 'loan churning', you can end up with a high loan balance on a home you've been paying on for over a decade.

The Truth Behind Skipping a Mortgage Payment

This is one of the most effective and misleading marketing tactics. The lender structures the closing so that you don't have a payment due for the first 30-60 days. It feels like a vacation from bills, but it's an expensive illusion.

The interest on your loan accrues daily. The interest from the 'skipped' period is simply added to your principal balance when the new loan is finalized. You are essentially taking out a small loan to cover your mortgage payment and then paying interest on it for the next 30 years.

The VA explicitly states that a lender cannot advertise 'skipped payments' as the primary benefit of the loan, as it is not a true benefit to the borrower.

Key Questions to Ask a Lender About Their VA IRRRL Offer

Before you proceed with any IRRRL, get on the phone with the loan officer and ask direct questions. Their answers (or lack thereof) will reveal the quality of the offer.

- 'What is the total dollar amount of closing costs and fees being added to my loan balance?'

- 'What is the exact recoupment period for this loan in months?'

- 'Are there any discount points included in this offer? If so, what would the interest rate be without them?'

- 'Can you confirm that you are not charging an appraisal fee or any other fees that the VA does not permit on an IRRRL?'

- 'Will my new loan balance be higher than my current one? By how much?'

- 'What is the APR (Annual Percentage Rate)?' (The APR includes fees and interest, giving a more accurate picture of the loan's cost than the interest rate alone).

When Keeping Your Current VA Loan Is the Smarter Financial Move

Sometimes, the best action is no action. A VA loan is an incredible benefit, and your existing mortgage might already be a fantastic deal. It is always the smarter financial move to keep your current VA loan when:

- The Recoupment Period is Longer Than Your Time Horizon: If you think you might sell your home or move in the next few years, a refinance with a long breakeven point will result in a net financial loss.

- The Offer Erodes Your Equity: If the new loan significantly increases your principal balance, you are trading long-term wealth for a small amount of short-term monthly cash flow.

- The Interest Rate Reduction is Negligible: If you already have a great rate, chasing a slightly lower one often doesn't make financial sense once closing costs are factored in.

- The Lender is Vague or Evasive: If a loan officer can't give you clear, straight answers to the questions listed above, it's a massive red flag. A trustworthy lender will be transparent about all costs and terms. If you're evaluating a VA IRRRL offer in Florida and the numbers seem confusing, don't sign anything without getting a second opinion. A transparent mortgage strategist can review your Loan Estimate and help you determine if the refinance truly benefits your financial goals.

Feeling uncertain about a VA IRRRL offer? Don't let confusing advertisements dictate your financial future. We provide clear, honest mortgage advice to help you make the best decision for your family. Ready for a transparent look at your options? Apply now.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References