Why Lenders Average Self-Employed Income

When you apply for a mortgage as a self-employed individual, lenders don't just look at your most recent earnings. They look for a stable and predictable income history. The primary tool they use for this is income averaging, typically over a 24-month period based on your federal tax returns. The logic is straightforward: they want to mitigate risk. A single high-earning year could be a fluke, while a two-year average provides a more conservative and, in their view, realistic picture of your ability to repay a large loan over 30 years.

This standard practice, however, can be incredibly frustrating for successful business owners. Imagine your consulting firm billed $90,000 in 2022 but, after landing two major clients, billed $200,000 in 2023. You live and budget based on your current success, but the lender sees your qualifying income as only $145,000 (($90,000 + $200,000) / 2). This calculation can drastically reduce your purchasing power, pushing your ideal home out of reach. The underwriter’s core question is: 'Is the $200,000 year the new normal, or was it an outlier?' Your job is to provide the evidence that proves it's the new standard for your business.

What Documents Prove Your Income Is Stable and Growing?

To convince an underwriter to use your most recent, higher income, you must go beyond your tax returns. You need to build a comprehensive file that paints a clear picture of your business's current and future financial health. Relying solely on tax returns, which are historical documents, is a common mistake. Instead, assemble a package that includes the following:

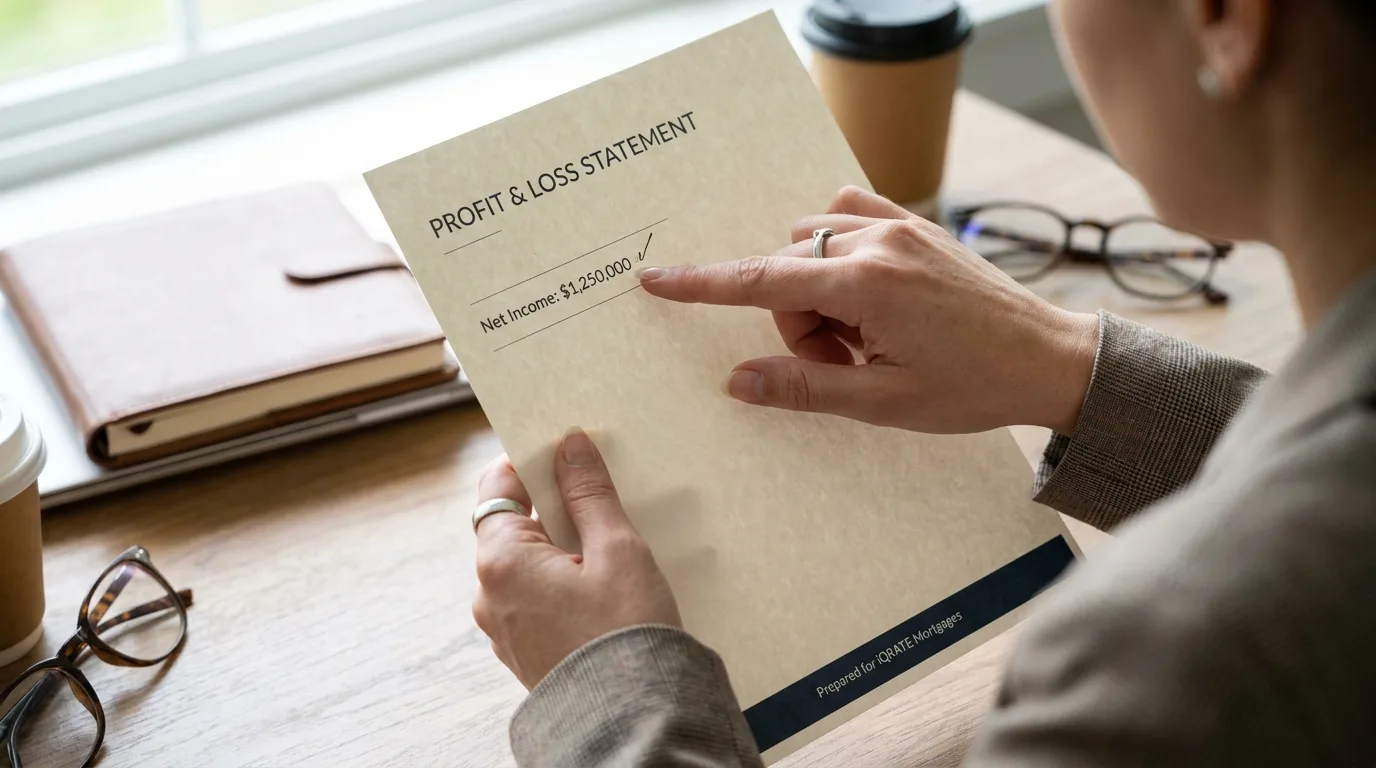

- Year-to-Date Profit & Loss (P&L) Statement: This is the single most important document. A P&L prepared by a Certified Public Accountant (CPA) shows your revenue, expenses, and net income for the current year. If it demonstrates a continued upward trend from your last tax return, it’s powerful evidence.

- Business Bank Statements: Provide at least 12, but preferably 24, months of statements. This allows the underwriter to see consistent cash flow, verify the revenue claimed on your P&L, and assess the overall financial stability of your business operations.

- Signed Contracts or Agreements: Do you have long-term contracts with clients? Provide copies. These documents prove future, guaranteed income and directly counter the idea that your recent success was a one-time event.

- A Detailed List of Clients: Showing a diverse client base can demonstrate that your income isn't reliant on a single source, which is a major risk factor for lenders.

- Evidence of Business Longevity: If your business has been operating for more than five years, even if your income fluctuated, provide your business license or registration documents to prove its history.

Can a Profit and Loss Statement Overcome a Weak Tax Year?

Yes, a well-prepared P&L can absolutely overcome a weaker prior tax year, but it cannot do so in a vacuum. It must be part of a larger, cohesive story. An underwriter won't simply discard a filed tax return in favor of an internal financial statement. However, when a CPA-prepared P&L is combined with a strong Letter of Explanation and corroborating bank statements, it can persuade the underwriter to give more weight to your recent performance.

For example, a graphic designer had a net income of only $65,000 in 2022 because they invested heavily in new software and hardware. In 2023, that investment paid off, and their income jumped to $130,000. Their P&L for the first half of 2024 shows they are on track for $150,000. This P&L proves the investment was sound and the income trend is not just continuing but accelerating.

Making Your P&L Credible for Underwriters

For a P&L to be taken seriously, it must meet certain standards:

- Third-Party Preparation: It must be prepared and signed by a non-biased third party, like a CPA or licensed tax preparer. A P&L you create yourself in QuickBooks holds little to no weight.

- Detailed and Itemized: It should clearly break down sources of revenue and categories of expenses. This transparency builds credibility.

- Aligned with Bank Statements: The gross revenue reported on the P&L must be reconcilable with the deposits shown on your business bank statements for the same period.

How Business Structure Changes Affect Income Averaging

Changing your business entity—for example, from a sole proprietorship to an S-Corporation—is a common step for growing businesses. While it makes sense for tax purposes, it can create significant hurdles in the mortgage process. To an underwriter, the S-Corp is a brand-new business, and they will want to see a two-year history from the date of incorporation, regardless of how long you operated as a sole proprietor.

To overcome this, you must prove continuity. You need to document that it’s the same business, just with a different legal wrapper. Provide the underwriter with:

- A letter from your CPA explaining that the business operations, services, and client base remained identical after the structural change.

- Tax returns for both the old and new entities (e.g., your final Schedule C as a sole proprietor and your first 1120-S return for the S-Corp).

- Evidence that you have the same business address, website, and phone number.

By clearly linking the old business to the new one, you can help the underwriter justify using the combined income history instead of starting the clock over.

Qualifying With Only One Year of Tax Returns

While the industry standard is two years of tax returns for self-employed borrowers, it is sometimes possible to qualify with just one. This is an exception, not the rule, and is typically reserved for borrowers with very strong overall financial profiles. Conventional loans backed by Fannie Mae and Freddie Mac have provisions for this, but you must meet a high bar.

To be considered, you will need several compensating factors, such as:

- Excellent Credit: A FICO score of 720 or higher is often the minimum.

- Large Down Payment: Putting 20-25% or more down reduces the lender's risk.

- Significant Cash Reserves: You'll need to show you have enough liquid assets to cover at least 6-12 months of mortgage payments (including principal, interest, taxes, and insurance) after closing.

- Proof of a Solid Business: The business itself should have a track record of at least five years, which you can prove with business licenses or other documentation, even if you've only been drawing income from it for a shorter period. (The data, information, or policy mentioned here may vary over time.)

This option is most viable for established professionals in stable industries who recently transitioned from a W-2 job to opening their own practice in the same field.

Writing a Powerful Letter of Explanation for Your Income

A Letter of Explanation (LOX) is your opportunity to speak directly to the underwriter and provide the context behind the numbers. A common mistake is to write an emotional plea; instead, you should write a professional business case. The goal is to explain why a previous year was lower and why your current, higher income is stable and likely to continue.

Key Components of an Effective Letter of Explanation

Your LOX should be structured, concise, and factual. Focus on these four points:

- Acknowledge the Discrepancy: Start by stating the facts. 'My 2022 tax returns show a net income of $85,000, while my 2023 returns show $160,000. I am writing to provide context for this significant growth.'

- Provide a Clear, Business-Related Reason: Explain the 'why'. 'In 2022, I made a strategic decision to invest $50,000 in new equipment and certifications. While this reduced my taxable income for that year, it directly expanded my service capacity and allowed me to secure higher-paying contracts in 2023.' Avoid vague or personal reasons that don't relate to the business's health.

- Prove the Upward Trend is Sustainable: This is where you connect the letter to your other documents. 'As you can see from my attached year-to-date P&L, my business is on track to earn over $180,000 this year. This is supported by the two new long-term client contracts I have also provided.'

- Conclude with Confidence: End on a professional note. 'This documentation demonstrates a clear and sustainable upward trend in my business's profitability, and I am confident in my ability to manage the financial responsibilities of this mortgage.'

Flexible Loan Programs for Fluctuating Income

If your income profile doesn't fit neatly into the conventional mortgage box, there are alternative loan programs specifically designed for business owners.

- Bank Statement Loans (Non-QM): These are the most popular alternative for self-employed borrowers. Instead of tax returns, lenders use 12 or 24 months of your business bank statements to qualify you. They calculate your income based on your average monthly deposits, essentially ignoring tax write-offs. This allows you to qualify based on your business's actual cash flow, not its net taxable income. (The data, information, or policy mentioned here may vary over time.)

- FHA Loans: While FHA guidelines also typically require a two-year income average, they can sometimes be more lenient if the income decline was caused by a specific, explainable circumstance and your income has since recovered and stabilized for at least 12 months. (The data, information, or policy mentioned here may vary over time.)

- Portfolio Loans: These loans are kept on the books of the lending institution (like a local credit union or bank) instead of being sold. Because they don't have to conform to Fannie Mae or Freddie Mac rules, the lender can set its own underwriting criteria, which can be more flexible for strong borrowers with unique income situations. (The data, information, or policy mentioned here may vary over time.)

How Your CPA Can Strengthen Your Mortgage Application

Your CPA is one of the most valuable members of your mortgage team. Their role goes far beyond just filing your taxes. A proactive CPA can:

- Prepare an Underwriter-Ready P&L: A CPA-prepared P&L statement adds a layer of professional verification that underwriters trust.

- Write a Letter of Verification: Your CPA can provide a formal letter confirming the health and stability of your business, explaining that the recent income growth is sustainable, and verifying that the business will not be negatively affected by the new mortgage debt.

- Organize Your Financials: Self-employed tax returns (Schedule C, 1120-S, K-1s) can be complex. Your CPA can help organize these documents and ensure they are presented to the lender in a clear, logical format, preventing unnecessary questions and delays from the underwriting team. If your business is thriving but your tax returns don't tell the whole story, don't let income averaging stop you. A strategic approach to documentation can make all the difference. Connect with a mortgage advisor who specializes in self-employed scenarios to build a compelling case for your Austin or Dallas home loan.

Navigating the mortgage process with a self-employed income requires a strategic approach. Our specialists understand the nuances of your financial journey and can help you present a compelling case to lenders. Ready to turn your business success into homeownership? Apply now to get started.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

Fannie Mae: Self-Employment Income Guidelines

CFPB: What documents do I need for a mortgage if I'm self-employed?