Can I use a VA loan to buy a two-to-four unit property?

Yes, you absolutely can use a VA home loan to purchase a property with two, three, or even four units. This is one of the most powerful and underutilized benefits available to eligible veterans, active-duty service members, and surviving spouses. The key requirement is that the property must serve as your primary residence. This means you must personally occupy one of the units.

The Department of Veterans Affairs guarantees these loans, allowing you to enter the real estate investment world with significant advantages. Whether you're eyeing a duplex in Oceanside or a four-plex closer to downtown San Diego, the VA loan program is designed to support you, provided the property meets VA's Minimum Property Requirements (MPRs) for safety, structural soundness, and sanitation.

Key Eligibility for a VA Multi-Family Loan

- Certificate of Eligibility (COE): You must have a valid COE proving you meet the military service requirements.

- Primary Occupancy: You must intend to occupy one of the units as your main home.

- Lender Qualifications: You still need to meet the lender's credit and income standards.

- Property Approval: The property must pass a VA appraisal and inspection to ensure it meets MPRs.

How does the rental income from other units help me qualify?

This is the core of the 'house hack' strategy and a massive advantage for VA loan borrowers. Lenders can use the projected rental income from the other units to help you qualify for the loan. This income can be used to offset your monthly mortgage payment, effectively lowering your debt-to-income (DTI) ratio.

Here’s how it works: During the appraisal process, the VA appraiser will determine the fair market rent for the units you don't plan to occupy. Lenders will typically allow you to use about 75% of this gross monthly rental income to qualify. (The data, information, or policy mentioned here may vary over time.) The 25% buffer accounts for potential vacancies and maintenance costs.

Example: Duplex in Oceanside

Let's say you want to buy a duplex in Oceanside for $950,000. Your estimated monthly mortgage payment (Principal, Interest, Taxes, and Insurance) is $6,200.

- The second unit has a projected fair market rent of $2,800 per month.

- The lender will likely use 75% of that income: $2,800 x 0.75 = $2,100.

- This $2,100 is subtracted from your housing expense for qualification purposes: $6,200 - $2,100 = $4,100.

By using the rental income, your qualifying DTI is calculated based on a $4,100 housing payment instead of $6,200, making it significantly easier to get approved for the loan.

What are the occupancy requirements for a VA loan on a duplex in Coronado?

Occupancy is a non-negotiable rule for VA loans. The VA guarantees these loans with favorable terms because they are intended to help veterans secure housing, not purely for investment purposes. When you buy a multi-family property, like a duplex in Coronado, you must certify your intent to live in one of the units as your primary residence.

Generally, you are expected to move into the property within a reasonable time, which is typically defined as 60 days from the closing date. You are also expected to live there for at least one year. After fulfilling this initial occupancy period, your plans can change. You could then move out and rent your unit, turning the entire property into a full-time investment while potentially using your remaining VA loan entitlement to buy another primary residence.

It’s crucial to be honest about your intentions. Falsely certifying occupancy is considered mortgage fraud, which carries severe penalties.

Is an FHA 203k loan better if the property needs repairs?

If the duplex you want to buy is a fixer-upper, an FHA 203k loan is almost certainly a better tool than a standard VA loan. VA loans have strict Minimum Property Requirements (MPRs). If a property has issues like a failing roof, peeling paint, or outdated electrical systems, it will likely fail the VA appraisal, and the loan won't be approved until the seller completes the repairs.

An FHA 203k Rehabilitation Loan, on the other hand, is specifically designed for properties that need work. It allows you to roll the cost of the purchase and the cost of the necessary repairs into a single mortgage. This is ideal for a house hacker looking to build sweat equity and force appreciation.

- Use a VA Loan if: The property is in good, move-in-ready condition and passes the VA appraisal.

- Use an FHA 203k Loan if: The property needs significant repairs or renovations to be habitable or to meet your standards.

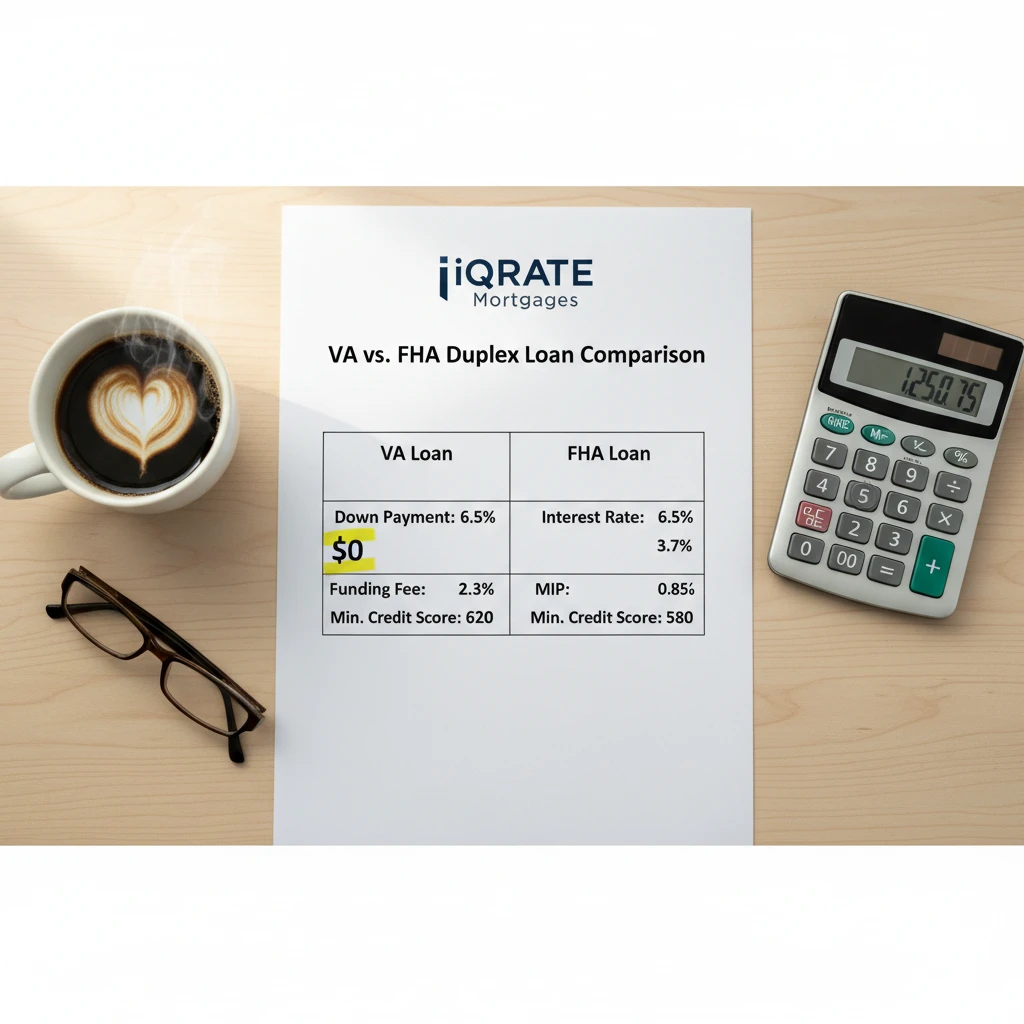

How do down payment requirements compare for VA versus FHA on a duplex?

The difference in down payment is one of the most significant financial advantages of the VA loan. For qualified veterans, a VA loan requires zero down payment, even on a multi-family property up to the conforming loan limit.

An FHA loan, while still a low-down-payment option, requires a minimum of 3.5% down. On a high-value property in the San Diego market, this difference amounts to tens of thousands of dollars in upfront cash.

Here is a comparison for a $1,100,000 duplex in San Diego:

- VA Loan: With a 0% minimum down payment, your required cash upfront is $0. This keeps more money in your pocket for closing costs or reserves. A VA funding fee applies but no monthly mortgage insurance is required.

- FHA Loan: With a 3.5% minimum down payment, your required cash upfront is $38,500. This loan also requires a 1.75% Upfront Mortgage Insurance Premium (UFMIP) and ongoing monthly mortgage insurance, adding to your total costs.

While the VA loan has a funding fee, it can often be rolled into the loan amount. FHA loans have both an upfront mortgage insurance premium (UFMIP) and a monthly mortgage insurance premium (MIP) that typically lasts for the life of the loan.

Which loan is more advantageous if I plan to move out in a few years?

Both VA and FHA loans require you to live in the property for at least one year. However, the VA loan offers more long-term flexibility and financial benefits if your plan is to eventually turn the duplex into a full rental property.

The VA Loan Advantage:

- No Monthly Mortgage Insurance: After you move out, your cash flow is significantly higher without a monthly mortgage insurance payment, which is a permanent feature of most FHA loans.

- Restoring Entitlement: Once you move and sell the property or pay off the loan, you can have your full VA entitlement restored to use again.

- Bonus Entitlement: Even if you keep the first property as a rental, you may have enough 'bonus' or 'remaining' entitlement to purchase another primary residence with a second VA loan, a strategy known as the 'two VA loan trick'.

The FHA Loan Consideration: An FHA loan is still a great option, but the persistent monthly MIP can eat into your rental profits long-term. Your best move is often to refinance out of the FHA loan into a conventional loan once you have at least 20% equity to eliminate the MIP.

For a long-term 'buy and hold' rental strategy, the VA loan's structure is generally more profitable.

Does the VA loan funding fee apply to multi-family purchases?

Yes, the VA funding fee applies to multi-family property purchases just as it does for single-family homes. This fee is a percentage of the loan amount and helps fund the VA loan program, reducing the cost to taxpayers.

The amount of the fee varies depending on several factors:

- Type of Service: Regular military, Reserves, or National Guard.

- Down Payment Amount: The fee is lower if you make a down payment of 5% or more.

- First-Time or Subsequent Use: The fee is higher for borrowers who have used their VA loan benefit before.

For a first-time user with zero down payment, the fee is typically 2.15%. For a subsequent user, it's 3.3%. (The data, information, or policy mentioned here may vary over time.) Importantly, this fee can be financed into the total loan amount, so it doesn't have to be paid in cash at closing.

Funding Fee Exemption

You are exempt from paying the VA funding fee if you are a veteran receiving VA compensation for a service-connected disability, a veteran who would be entitled to receive disability compensation if you did not receive retirement or active duty pay, or a surviving spouse of a veteran who died in service or from a service-connected disability.

Ready to put your VA benefits to work with a duplex house hack? Explore your options for a San Diego or Oceanside property and build a strategy that maximizes your investment. Apply now to get a clear analysis and secure your financial future.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

VA Home Loans for a Multifamily Property

HUD FHA Multifamily For-Profit Properties

Consumer Financial Protection Bureau - What is a debt-to-income ratio?