What Does 'Veteran Affairs Approved' Mean for a Condo?

When you use a Veteran Affairs (VA) home loan, the VA guarantees a portion of the loan for the lender. This protection allows lenders to offer incredible benefits like zero down payment and no private mortgage insurance (PMI). However, to protect both the veteran and the government's investment, the VA sets strict standards not only for the borrower but also for the property itself. For a condominium, this means the entire project or complex must be 'VA Approved'.

This isn't about the physical condition of your specific unit. Instead, the VA approval process is a comprehensive review of the condominium project's health and governance. The VA wants to ensure the Homeowners Association (HOA) is financially sound, legally compliant, and operates in a way that protects the property values of all residents. Essentially, the VA is vetting the HOA to prevent a veteran from buying into a mismanaged or financially unstable community that could lead to special assessments, lawsuits, or declining values.

Key Areas the VA Scrutinizes:

- Financial Stability: The HOA must have adequate reserve funds for future repairs and a realistic operating budget. The VA checks for a high number of delinquent HOA dues.

- Legal Compliance: The project's governing documents (like Covenants, Conditions, and Restrictions or CC&Rs) cannot contain clauses that unfairly restrict the owner's ability to sell or lease their property.

- Owner-Occupancy Rate: The VA prefers communities where a majority of residents are owner-occupants rather than renters, as this typically indicates a more stable and well-maintained environment.

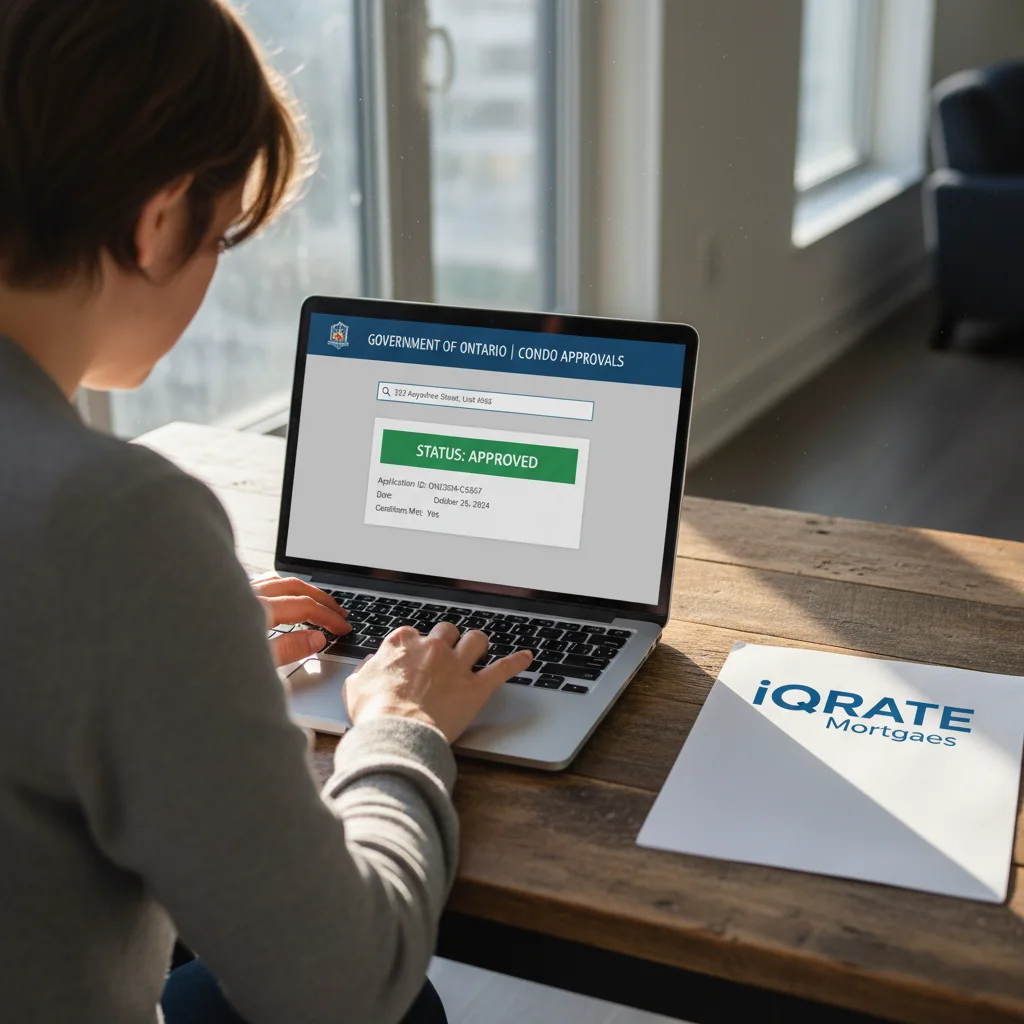

How to Check if a San Diego Condominium is Approved

Before you get too attached to a condo in San Diego, the very first step is to check its VA approval status. This is a simple process that can save you significant time and potential heartbreak. The VA maintains a public, searchable database of all approved condominium projects across the country.

Here’s how to check:

- Visit the Official Portal: Navigate to the VA’s official Condo Report search page. This is the only official source.

- Enter Search Criteria: You can search by the Condominium ID number if you have it, but it’s usually easier to search by name or location. Select 'California' as the state and enter 'San Diego' for the county.

- Specify Condo Name: Type the legal name of the condominium association into the 'Condominium Name' field. Be as specific as possible. Sometimes the marketing name of a building differs from its legal HOA name, so you may need to ask the seller’s agent for the correct information.

- Review the Status: The search results will show one of three statuses:

- 'Approved': The project is currently approved, and you can proceed with a VA loan, assuming all other loan qualifications are met.

- 'Accepted Without Conditions': This is another term for approved.

- 'Unaccepted' or No Result: The project is not on the VA-approved list. This means you cannot use a standard VA loan for a unit in this building without taking further action.

Doing this check early in your home search, especially with your real estate agent, can prevent you from wasting time on properties that are not eligible for your financing.

Why Some Long Beach Condos Fail to Get VA Approval

It can be baffling when a beautiful, well-maintained condominium building in a desirable area like Long Beach is not on the VA-approved list. The reasons almost always trace back to the HOA's financial or legal structure, which may not meet the VA's stringent requirements designed to protect veterans.

HOA Legal and Financial Issues

This is the most common category for rejection. The VA needs to see that the HOA is a responsible and stable entity. Red flags include:

- Pending Litigation: If the HOA is currently involved in a significant lawsuit (e.g., with a contractor over construction defects or with a resident), the VA will typically deny approval until the litigation is resolved. The financial risk is considered too high.

- Inadequate Reserve Funds: HOAs are required to maintain a reserve fund to cover major future expenses like roof replacement, elevator repairs, or repainting. The VA generally wants to see that at least 10% of the HOA’s annual income is allocated to this reserve fund. (The data, information, or policy mentioned here may vary over time.) An underfunded reserve could lead to large, unexpected special assessments for homeowners.

- High Delinquency Rate: If more than 15% of the condo owners are over 60 days late on their HOA dues, it signals financial instability within the community. (The data, information, or policy mentioned here may vary over time.) This directly impacts the HOA's ability to pay for maintenance and services.

Restrictive Covenants and Bylaws

The VA carefully reviews the HOA’s governing documents (CC&Rs). Certain clauses can trigger an immediate denial:

- Right of First Refusal: Some older bylaws include a 'right of first refusal', which allows the HOA or another owner to purchase a unit before an outside buyer can, even if the seller has accepted an offer. The VA prohibits this because it can interfere with the free transfer of property.

- Excessive Leasing Restrictions: While the VA wants high owner-occupancy, it does not approve projects that severely restrict a veteran’s right to rent out their unit in the future.

- High Investor Concentration: If more than 50% of the units are owned by investors and used as rentals, the VA may deny the project. (The data, information, or policy mentioned here may vary over time.) They view high tenant-to-owner ratios as a potential risk to property upkeep and community stability.

The 'Spot Approval' Process for a Single Unit

If you find a condo in a non-approved building, all is not lost. The VA offers a path called Single-Unit Approval (SUA), often referred to as 'spot approval'. This process allows a lender to seek VA approval for just one specific unit within an unapproved project, rather than getting the entire complex approved.

However, the project must still meet certain baseline criteria. A spot approval is not a loophole for problematic buildings. For a unit to be eligible for SUA, the condominium complex must generally meet these conditions:

- Established Community: The project must be fully complete, not in the middle of construction or phasing.

- Owner-Occupancy: At least 50% of the units must be owner-occupied. (The data, information, or policy mentioned here may vary over time.)

- Financial Health: No more than 15% of unit owners can be delinquent on their HOA dues. (The data, information, or policy mentioned here may vary over time.)

- Size Limitations: In projects with fewer than 20 units, no single owner can own more than two units. In projects with 20 or more units, no single owner can own more than 25% of the total units.

- No Disqualifying Legal Issues: The project cannot have the same red flags that would cause a full project denial, such as major litigation.

Your VA-approved lender is responsible for submitting the SUA request and all required documentation to the VA on your behalf.

Timeline for the VA Condo Approval Process

Timing is a critical factor, as the condo approval process runs parallel to your loan underwriting and can extend your closing timeline. You must factor this into your purchase contract.

- Full Project Approval: If you are trying to get an entire complex approved for the first time, the process can be lengthy. After the HOA provides all necessary documents to your lender, it typically takes the VA 30 to 60 days to review the package and issue a decision. (The data, information, or policy mentioned here may vary over time.) Delays often happen when an HOA is slow to provide complete and accurate documentation.

- Single-Unit Approval (SUA): The spot approval process is generally faster. Once the lender has the required documents, the review and decision from the VA can take approximately 15 to 30 business days. (The data, information, or policy mentioned here may vary over time.) However, this still adds several weeks to a standard 30-day closing period.

It is essential to communicate with your lender and real estate agent to set realistic expectations for the seller and ensure your contract includes enough time to accommodate the VA's review.

Who Handles the Approval Request?

This is a common point of confusion. The responsibility for getting a condo approved is a collaborative effort, but the official submission to the VA must be handled by a VA-approved lender.

- The Buyer & Real Estate Agent: You and your agent identify that the property needs approval and communicate this to your lender.

- The Lender: Your loan officer is the primary driver of the process. They will request a specific list of documents from the HOA or its management company and will be the one to assemble the submission package and formally send it to the VA for review.

- The Homeowners Association (HOA): The HOA or its management company is responsible for providing all the required legal and financial documents. Their cooperation and speed are the most critical factors in the timeline. Some HOAs charge a fee for compiling and providing these documents.

Ultimately, the buyer's mortgage lender is responsible for initiating and managing the approval process with the VA.

Alternative Loans if a Condo Can't Be VA Approved

If the condo project in Long Beach simply cannot meet VA guidelines, or if you don’t have time to wait for the approval process, you have other excellent financing options:

- Conventional Loan: This is the most common alternative. While you will likely need a down payment (typically 3-5% minimum) and will have to pay PMI if you put down less than 20%, conventional loans do not require the building to be on a specific approved list. (The data, information, or policy mentioned here may vary over time.) Their standards for condo reviews are often more flexible than the VA's.

- FHA Loan: The Federal Housing Administration (FHA) also insures loans and has its own list of approved condominium projects. It's a separate list from the VA's, so it’s worth checking the FHA-approved condo list. A building might be FHA-approved even if it isn't VA-approved.

- CalVet Home Loan: For veterans in California, the CalVet loan program is another fantastic option. CalVet loans have their own guidelines and may be able to finance a condo that the federal VA program cannot.

Essential Documents the HOA Must Provide

For a lender to submit an approval request, they need a comprehensive package of documents from the HOA. Being aware of this list can help you understand if the HOA is prepared and willing to cooperate.

Key documents include:

- Governing Documents: This includes the Declaration or CC&Rs, Bylaws, and any Articles of Incorporation.

- Financial Statements: A current balance sheet and year-to-date income/expense statement.

- Annual Budget: The approved budget for the current year.

- Meeting Minutes: Minutes from the last two HOA meetings.

- Insurance Declaration: Proof of the master hazard insurance policy for the complex.

- Occupancy Statement: A letter stating the total number of units, the number of owner-occupied units, and the number of units with delinquent dues.

- Litigation Statement: A formal statement disclosing any current or pending litigation. Navigating the VA condo approval process requires expertise and a proactive lender. If you're a veteran looking to buy a condo in San Diego or Long Beach, working with a mortgage professional who understands these specific VA requirements is essential for a smooth and successful closing.

Feeling confident about the VA condo approval process is the first step. If you're ready to move forward with a team that understands the nuances for veterans in San Diego and Long Beach, we're here to help. Apply now to start your pre-approval and get one step closer to your new home.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References