Why a Good Credit Score Isn't a Guaranteed Mortgage Approval

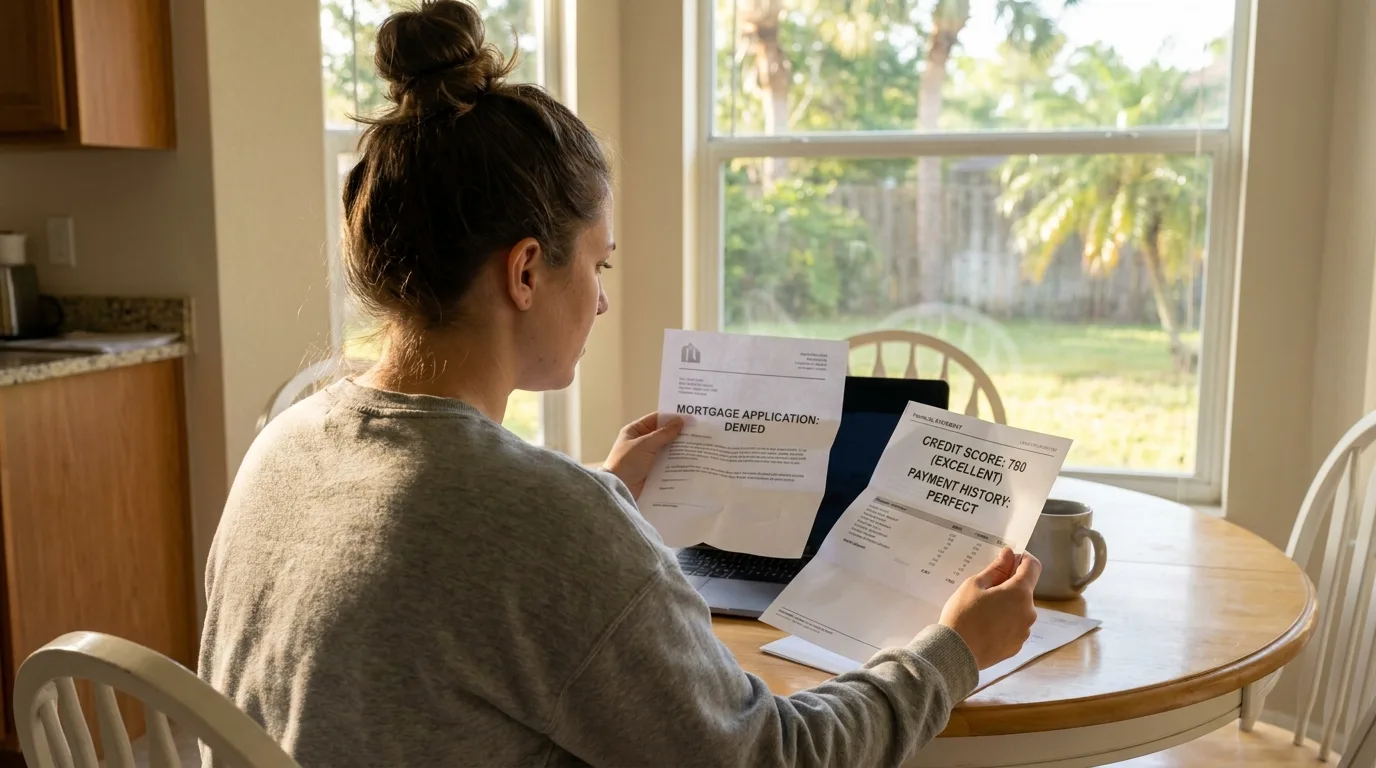

Receiving a mortgage denial when you have a credit score over 700 is incredibly frustrating. You've managed your finances responsibly, paid bills on time, and maintained a score that should unlock the best loan terms. So why the rejection? The answer lies in the difference between a high score and a robust credit profile.

Mortgage lenders rely on Automated Underwriting Systems (AUS) like Fannie Mae's Desktop Underwriter (DU) or Freddie Mac's Loan Product Advisor (LPA). These systems look beyond the three-digit score. They analyze:

- Credit History Length: How long have you been using credit? A history shorter than two years can be a red flag.

- Number of Tradelines: How many credit accounts do you have (credit cards, auto loans, student loans)? Too few accounts provide limited data for the AUS to assess risk.

- Type of Credit: A mix of credit types, such as revolving debt (credit cards) and installment loans (car loans), is viewed more favorably than just one or two credit cards.

A homebuyer in Tampa could have a 760 credit score derived from a single credit card they've had for ten years and a car loan they paid off three years ago. While the score is excellent, the AUS may see an insufficient amount of recent, active credit data and issue a denial.

Understanding the 'Thin Credit File' Automated Denial

A 'thin credit file' is the primary culprit behind good-credit mortgage denials. This term describes a credit report that lacks enough information for an AUS to confidently predict future payment behavior. It doesn't mean you have bad credit; it means you have not enough credit history.

Automated systems are programmed with algorithms that correlate specific data points with loan default risk. A thin file is flagged because:

- It Lacks Predictive Data: Without multiple accounts over several years, the system has no statistical basis to confirm you can handle a large, long-term mortgage payment.

- It Resembles Inexperience: To an algorithm, a short or limited credit history looks the same whether you're a responsible person who avoids debt or a young adult with no credit experience.

- It Cannot Evaluate Non-Traditional Payments: The AUS does not see the rent, utility, or insurance payments you've made consistently for years. It only sees what's reported to the major credit bureaus: Equifax, Experian, and TransUnion.

This is why an applicant in Orlando with a 720 score but only two active credit cards might be denied, while someone with a 680 score but five diverse tradelines and a decade of history gets approved. (The data, information, or policy mentioned here may vary over time.)

How to Prove Creditworthiness in Tampa Without Many Accounts

If an AUS denies you for a thin file, the next step is to prove your financial reliability with documentation the system ignored. This is where you build a case for a manual underwrite. You can demonstrate a strong payment history by gathering 'alternative credit' data.

Focus on consistent payments made over the last 12-24 months. Strong examples include:

- Rental Payments: Provide copies of canceled checks or bank statements showing on-time rent payments.

- Utility Bills: Gather 12 months of statements from your electric, water, gas, and internet providers.

- Insurance Premiums: Show proof of on-time payments for car, renter's, or life insurance.

- Other Regular Payments: This can include tuition, cell phone bills, or even regular deposits into a savings account.

The Solution: What Is a Manual Underwrite and How to Request One

A manual underwrite bypasses the AUS and puts your loan application in front of a human underwriter. This individual has the authority to look beyond the algorithm's decision and evaluate the complete picture of your financial habits. They can analyze the alternative credit data you've gathered and make a common-sense lending decision.

How to Request It: You typically cannot request a manual underwrite yourself. This is a process initiated by your mortgage broker or lender. When you receive an AUS denial due to a thin file, you should immediately:

- Contact Your Loan Officer: Explain the situation and ask if a manual underwrite is an option with that specific lender.

- Work with an Experienced Broker: A skilled mortgage broker who specializes in complex cases will know which wholesale lenders are receptive to manually underwriting loans. They can resubmit your file to a lender who will give it the human review it deserves.

- Be Prepared to Provide Extra Documentation: The key to a successful manual underwrite is thorough documentation. Your loan officer will provide a precise list of what's needed.

Documents Needed to Strengthen a Manually Underwritten File

To get an approval, you must provide clear, convincing evidence of your financial stability. The underwriter is looking for proof that you manage your money well, even if it's not reflected on your credit report.

Key documents include:

- Verification of Rent (VOR): A form completed by your landlord confirming 12-24 months of on-time rent payments.

- Bank Statements: At least two to three months of statements showing consistent income, responsible spending, and sufficient cash reserves.

- Proof of Alternative Credit: 12 months of canceled checks or statements for at least three non-traditional sources (e.g., utilities, insurance, phone bill).

- Letter of Explanation (LOX): A brief, clear letter explaining why your credit file is thin. For example, 'I have always prioritized living debt-free and therefore only use a single credit card for emergencies'.

Using Rental History to Prove Payment Reliability in Orlando

For many renters in Orlando and across Florida, their largest monthly expense—rent—is never reported to credit bureaus. This is a huge missed opportunity to demonstrate creditworthiness. In a manual underwrite, rental history becomes your most powerful tool.

A lender sees a consistent history of on-time rental payments as a strong indicator that you can handle a mortgage payment, which is often a similar amount. If you can prove you've successfully paid $2,200 in rent every month for two years, it gives the underwriter confidence you can manage a $2,300 mortgage payment (principal, interest, taxes, and insurance).

Are There Specific Loans for Thin Credit Files?

Yes. While conventional loans can be manually underwritten, government-backed loans are often more flexible for borrowers with non-traditional credit history.

- FHA Loans: The Federal Housing Administration explicitly allows for manual underwriting and has clear guidelines for using non-traditional credit. They are often the best option for first-time homebuyers with thin files.

- VA Loans: Available to eligible veterans and service members, VA loans are also more lenient and have established manual underwriting procedures.

- USDA Loans: For homes in eligible rural areas, USDA loans also accommodate thin or alternative credit files. (The data, information, or policy mentioned here may vary over time.)

How to Build a Stronger Credit File for Future Home Loans

If a manual underwrite isn't an option or you want to prepare for the future, focus on strategically building your credit profile. The goal is to create the robust history that automated systems want to see.

- Open Two to Three New Credit Cards: Choose cards with no annual fees. Use them for small, regular purchases (like gas or groceries) and pay the balance in full every month. This adds new, positive tradelines.

- Become an Authorized User: Ask a family member with excellent, long-standing credit to add you as an authorized user on one of their credit cards. Their positive payment history will appear on your report.

- Consider a Credit-Builder Loan: These are small loans offered by credit unions or banks where the money you borrow is held in a savings account. You make small monthly payments, and once the loan is paid off, the funds are released to you. Your payments are reported to the credit bureaus, building a positive history.

- Use Rent-Reporting Services: Services like Rental Kharma or LevelCredit can report your on-time rent payments to the credit bureaus for a small fee, directly helping to build your file. A mortgage denial from an automated system is not the end of the road. If you have a good credit score but a thin credit file, partnering with a mortgage expert who understands manual underwriting can make all the difference. An experienced broker can navigate the process and present your financial story for a successful approval.

A denial from an automated system isn't the final say on your homeownership dream. If your strong financial habits aren't reflected in your credit file, our team can help you navigate the manual underwriting process and present your complete financial picture. Take the next step with an expert who understands. Apply now to explore your options.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.