What is a Mortgage Escrow Account and What Does It Pay in Austin?

Think of a mortgage escrow account as a dedicated savings account managed by your mortgage lender. Each month, a portion of your total mortgage payment is deposited into this account. The lender then uses these funds on your behalf to pay two significant homeownership expenses: your property taxes and your homeowners insurance premiums. This system is often referred to as PITI, which stands for Principal, Interest, Taxes, and Insurance. Your lender pays the principal and interest on the loan, while the escrow account handles the taxes and insurance.

The purpose of escrow is to ensure these critical bills are paid on time, protecting both you and the lender. If you failed to pay property taxes, the taxing authority (like Travis County for an Austin home) could place a lien on your property, which puts the lender's investment at risk.

Here’s a simple breakdown of the calculation:

- Annual Property Tax Bill: $9,000

- Annual Homeowners Insurance Premium: $3,000

- Total Annual Escrow Costs: $12,000

To cover this, the lender will collect $1,000 per month ($12,000 / 12) and place it into your escrow account. Federal law also allows lenders to keep a cushion in the account, typically equal to two months of escrow payments, to handle any unexpected increases. (The data, information, or policy mentioned here may vary over time.)

Why Is the First Year's Escrow Calculation Often Too Low for Texas Properties?

The most common cause of 'payment shock' for new Texas homeowners stems from how initial escrow payments are calculated. When you close on your home, the lender doesn't have your future tax bill. Instead, they base their initial escrow calculation on the seller's current property tax bill.

This creates a significant problem for a few key reasons:

- Lower Assessed Value: The seller may have owned the home for years. In Texas, the annual increase in a property's assessed value is often capped for existing homeowners with a homestead exemption. Their assessed value could be far below the home's current market value.

- Existing Exemptions: The seller almost certainly had a homestead exemption and potentially other exemptions (like for being over 65 or a veteran) that dramatically reduced their tax liability. These personal exemptions do not transfer to you, the new buyer.

As a result, your first year of mortgage payments is based on artificially low tax information. You are essentially paying based on the seller's discounted tax rate. The lender collects this lower amount for 12 months, creating a financial deficit when the actual, much higher tax bill comes due.

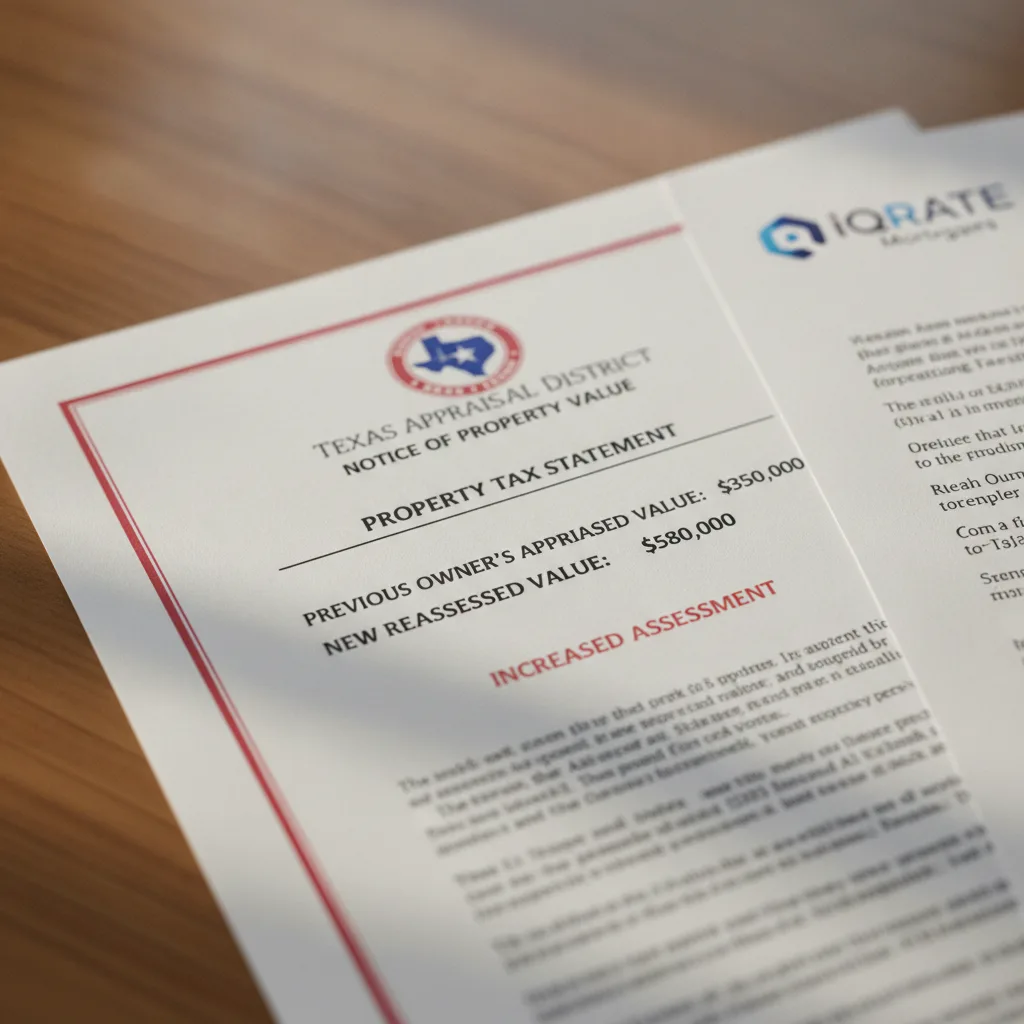

How Are Property Taxes Reassessed After a Home Sale in Dallas?

Once you purchase a home, the sale is recorded publicly. The local county appraisal district, such as the Dallas Central Appraisal District (DCAD), sees that the property sold for a new price. This sales price becomes the new baseline for your property's market value.

In the following year, the appraisal district will reassess the property's value to reflect what you paid for it. This is where new homeowners in cities like Dallas and Houston see a massive jump.

Let’s look at a realistic scenario:

- Seller's Situation: They bought their Dallas home in 2010. Their assessed value for tax purposes was capped and had only risen to $400,000.

- Your Purchase: You buy the home in 2024 for its current market value of $650,000.

- The Reassessment: In early 2025, DCAD will send you a notice of appraised value, updating the home's taxable value to be much closer to the $650,000 you paid. Your property tax bill will now be calculated based on this higher value.

This reassessment is the trigger for the entire escrow shortage problem. The amount your lender was collecting monthly is now completely inadequate to cover a tax bill based on a $650,000 valuation.

What is an Escrow Shortage Notice and What Are My Payment Options?

An escrow shortage occurs when the money in your escrow account is not enough to cover the actual property tax and insurance bills. Annually, your mortgage servicer conducts an 'escrow analysis' to reconcile the account.

When they see the new, higher tax bill from the county, they will determine you have a shortage. You will receive a letter detailing this shortage and explaining how your future payment will change. The new payment will be adjusted for two things:

- Covering the Shortage: You need to repay the deficit from the previous year.

- Funding the Future: The payment must be increased to collect enough for the next year's higher tax and insurance bills.

Your lender will typically give you two options to handle the shortage: (The data, information, or policy mentioned here may vary over time.)

- Option 1: Pay the Shortage in a Lump Sum. You can write a check for the entire shortage amount. Your monthly payment will still increase, but only to the level needed to cover future costs. This results in a lower monthly payment compared to the alternative.

- Option 2: Spread the Shortage Over 12 Months. The lender will divide the shortage amount by 12 and add it to your monthly mortgage payment for the next year. This is the default option if you do nothing.

Example of Payment Options

Let's say your initial escrow payment was $600/month. After reassessment, the true amount needed is $900/month. Over the first year, a shortage of $3,600 ($300 difference x 12 months) has accumulated.

- Lump Sum: You pay $3,600 upfront. Your new monthly escrow payment becomes $900.

- Spread it Out: The shortage ($3,600 / 12 = $300) is added to your new payment. Your next year's monthly escrow payment becomes $1,200 ($900 for new costs + $300 to cover the old shortage).

Can I Add Extra Money to My Escrow Account Each Month to Prepare?

Yes, absolutely. Being proactive is the best way to avoid the shock of a sudden payment increase. You can contact your mortgage servicer at any time and ask to pay extra toward your escrow account each month. This is a highly recommended strategy for any new Texas homeowner.

To do this effectively, you need to estimate your future tax bill. You can do this by taking your home's purchase price and multiplying it by the local tax rate (which is usually a combination of city, county, and school district rates). For example, if you bought a home in Houston for $450,000 and the combined tax rate is 2.5%, your estimated annual tax bill would be $11,250, or $937.50 per month. If your lender is only collecting $600, you should start paying an extra $337.50 monthly to build up a buffer.

How Does a Homestead Exemption Impact My Future Property Taxes?

A homestead exemption is a powerful tax-saving tool for Texas homeowners, but it's also a source of confusion for new buyers. It reduces the taxable value of your primary residence, lowering your overall property tax bill.

The most important thing to know is that homestead exemptions are not automatic and do not transfer from the previous owner. You must apply for your own exemption with your county appraisal district between January 1 and April 30 of the year after you purchase the home.

Filing for this exemption is critical. It will lower your tax bill for the second year and beyond. Furthermore, once established, the exemption generally caps the amount your home's assessed value can increase for tax purposes to 10% per year, protecting you from extreme spikes in property taxes as long as you own the home.

What Can I Do If the New Monthly Payment Is No Longer Affordable?

Receiving a notice that your mortgage payment is increasing by several hundred dollars can be distressing. If the new payment stretches your budget to its breaking point, do not ignore the notices from your lender. The worst thing you can do is to stop making payments.

Instead, take these steps:

- Contact Your Mortgage Servicer Immediately: Open the lines of communication. Explain your situation and ask what options are available. They want to avoid a foreclosure just as much as you do.

- Ask About Loss Mitigation Options: Your servicer can review your financial situation to see if you qualify for temporary relief, such as a forbearance plan (which pauses or reduces payments for a short period) or a loan modification that could potentially restructure your loan to make it more affordable.

- Seek Housing Counseling: Contact a HUD-approved housing counseling agency. These non-profit organizations offer free or low-cost advice to help you understand your options and negotiate with your lender.

Should I Waive Escrows If I Have the Option?

For some conventional loans where the buyer makes a down payment of 20% or more, the lender may offer the option to 'waive' escrow. (The data, information, or policy mentioned here may vary over time.) This means you would be responsible for paying your property tax and homeowners insurance bills directly. While this might seem appealing, it's a decision that requires serious consideration.

Pros of Waiving Escrow:

- Control: You have more control over your funds and can earn interest on the money you set aside for taxes and insurance.

- Lower Monthly Payment: Your required monthly payment to the lender will be lower since it only includes principal and interest.

Cons of Waiving Escrow:

- Discipline Required: You must be incredibly disciplined to save thousands of dollars for large, infrequent bills. Property taxes in Texas are typically paid in one or two large lump sums.

- High Risk: If you fail to save enough or forget a payment deadline, you could face steep penalties from the tax authority or a lapse in insurance coverage, which would be a default on your mortgage terms.

For the vast majority of homeowners, especially first-time buyers, maintaining an escrow account is the safer and more manageable choice. It automates the savings process and ensures your most important home-related bills are always paid on time. Understanding your Texas mortgage is the first step to financial stability. If you're preparing to buy in Austin, Dallas, or anywhere in Texas, planning for your real second-year payment is crucial. A knowledgeable mortgage advisor can help you budget accurately from day one.

Planning for your true homeownership costs is the key to a stress-free experience. If you're ready to navigate the Texas mortgage process with clarity and confidence, take the first step. Apply now to partner with a team that helps you budget for the real numbers from day one.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

CFPB - What is an escrow or impound account?