Veteran Property Tax Exemptions in Houston and Across Texas

Texas offers some of the most generous property tax exemptions in the country for its disabled veterans, a benefit that directly impacts your wallet when buying a home. These exemptions are not automatic; you must apply for them, but they can drastically lower your monthly mortgage payment. The amount of the exemption is tiered based on the disability rating assigned by the U.S. Department of Veterans Affairs (VA).

Here’s how the exemptions break down for qualifying disabled veterans:

- 10% to 29% Disability Rating: An exemption of $5,000 from your property's assessed value.

- 30% to 49% Disability Rating: An exemption of $7,500 from your property's assessed value.

- 50% to 69% Disability Rating: An exemption of $10,000 from your property's assessed value.

- 70% to 99% Disability Rating (and not 100%): An exemption of $12,000 from your property's assessed value.

- 100% Disability Rating or Unemployability: A total exemption from paying property taxes on your homestead.

This 100% exemption is a game-changer for veterans purchasing a home in competitive markets like Austin. It completely eliminates the 'T' (taxes) from your PITI (Principal, Interest, Taxes, Insurance) payment, which is the core component lenders use to determine your loan qualification.

How Lenders Factor Exemptions into a VA Loan

When you apply for a VA loan, lenders calculate your debt-to-income (DTI) ratio to assess your ability to repay the mortgage. Your DTI is your total monthly debt payments divided by your gross monthly income. A key part of this calculation is the estimated monthly mortgage payment, or PITI. By reducing the 'T' portion of this payment, your overall PITI decreases, which in turn lowers your DTI ratio.

Let’s look at a practical example in Austin:

- Home Price: $450,000

- Annual Property Taxes (without exemption): Approximately $8,100 (1.8% rate)

- Monthly Tax Payment (without exemption): $675

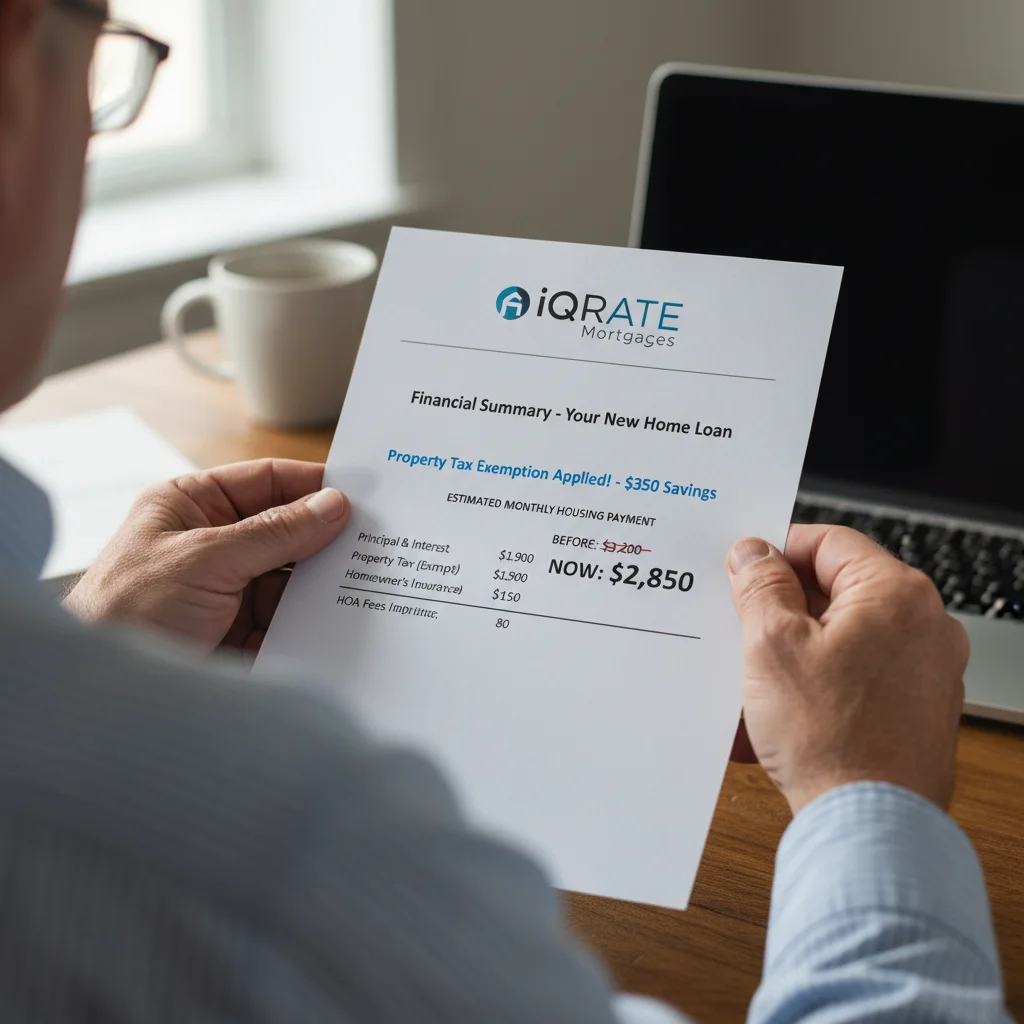

Scenario 1: Veteran with No Exemption Applied

- Principal & Interest (P&I): ~$2,700

- Taxes: $675

- Insurance: $150

- Total Estimated PITI: $3,525

Scenario 2: Veteran with a 100% Disability Rating

- Principal & Interest (P&I): ~$2,700

- Taxes: $0

- Insurance: $150

- Total Estimated PITI: $2,850

The lender can now use the lower $2,850 payment to calculate your DTI. This $675 monthly difference is significant. It shows the lender you have more disposable income to handle the mortgage, making you a stronger borrower and potentially allowing you to qualify for a more expensive home.

Disability Ratings and VA Loan Qualification

A common point of confusion for veterans in cities like San Antonio is how their disability rating itself impacts the loan. It's crucial to understand that lenders do not approve or deny you based on having a disability rating. Instead, they look at two financial factors that stem from it:

- Tax-Exempt Income: The monthly disability compensation you receive is non-taxable income. Lenders can 'gross up' this income, meaning they can count it as being worth more than its face value (often by 25%) because no taxes are taken out. This boosts your total qualifying income. (The data, information, or policy mentioned here may vary over time.)

- Property Tax Exemption: As detailed above, the rating grants you a specific property tax exemption, which lowers your projected monthly housing costs.

So, while a 70% rating doesn't directly impress an underwriter, the $12,000 property tax exemption and the 'grossed up' disability income it provides are powerful tools that directly and positively affect your mortgage qualification.

Required Documents for Your Mortgage Application

To ensure your lender can factor in the tax exemption before you close, you must provide the correct documentation proactively. You cannot assume the title company or lender will automatically know about your status. You will need:

- Your VA Certificate of Eligibility (COE): This is standard for any VA loan and proves you have the entitlement for the loan itself.

- VA Award Letter: This official letter from the VA clearly states your disability rating and the monthly compensation amount. This is the primary proof of your rating.

- Texas Comptroller Forms: You will need to complete and submit the required forms to the appraisal district of the county where you are buying the home, primarily Form 50-114 ('Application for Residence Homestead Exemption') and Form 50-135 ('Application for Disabled Veteran's or Survivor's Exemption'). Getting a letter from the county appraisal district confirming receipt and approval is the gold standard for your lender.

Bringing these documents to your loan officer at the very beginning of the process is essential for a smooth underwriting experience.

Using a Tax Exemption to Qualify for a Larger Home Loan

So, can this exemption really help you buy a more expensive home? Absolutely. By lowering your DTI, it frees up room in your budget, which translates directly to higher purchasing power.

Consider this comparison for a veteran buying a home in Houston with a gross monthly income of $8,000 and a common lender DTI benchmark of 41% for VA loans. (The data, information, or policy mentioned here may vary over time.)

- Maximum Monthly Housing Payment Allowed (PITI): $8,000 * 0.41 = $3,280

Without the 100% Tax Exemption:

- Let's assume a $400,000 home has a P&I of $2,400, insurance of $140, and taxes of $600.

- Total PITI: $3,140. This fits within the $3,280 limit.

- The veteran qualifies for the $400,000 home.

With the 100% Tax Exemption:

- The $600 monthly tax payment is eliminated.

- The lender now has an extra $600 of room to work with before hitting the $3,280 DTI cap.

- That extra $600 in payment ability (P&I) could translate to roughly $90,000 to $100,000 more in loan amount, depending on the interest rate.

- The veteran could now potentially qualify for a $490,000 home, all thanks to the exemption being properly applied during underwriting.

What if the Exemption is Applied After Closing?

This is a critical timing issue. If you close on your loan without the exemption being factored in by the lender, your initial monthly payments will be higher because they will include an estimated amount for property taxes, which is paid into an escrow account. You can still apply for the exemption with the county appraisal district after you own the home.

Once the county approves your exemption, they will notify your mortgage servicer. The servicer will then stop collecting property taxes for your escrow account. This will eventually lead to an 'escrow overage', and you will receive a refund check. Your monthly payment will then be lowered going forward. However, this does not help you with your initial loan qualification. To gain the benefit of a higher purchase price, the exemption must be documented and used by the underwriter before you sign the final closing documents.

Rules for Active Duty Military vs. Veterans

While active duty military personnel receive many benefits, including protections under the Servicemembers Civil Relief Act (SCRA), these specific Texas property tax exemptions are tied to a post-service VA disability rating. Therefore, most active duty members purchasing a home in Dallas would not be eligible for this particular benefit unless they are also a veteran with a qualifying disability rating from a prior service period.

Common Mistakes with Texas VA Loans and Tax Exemptions

Navigating this process can be tricky. Here are some common pitfalls to avoid:

- Assuming it's Automatic: Never assume the lender, title company, or real estate agent will handle the exemption for you. You must be proactive in providing the documentation.

- Waiting Until After Closing: As mentioned, this is the biggest mistake. You lose the primary benefit of increased purchasing power during qualification.

- Providing the Wrong Documents: A simple printout from your eBenefits account is often not enough. You need the official VA award letter and proof of filing with the county appraisal district.

- Misunderstanding County Deadlines: Each county appraisal district has its own deadlines for filing for exemptions. Be sure to check with the specific county where you are buying (e.g., Harris County for Houston, Travis County for Austin). (The data, information, or policy mentioned here may vary over time.) Navigating Texas property tax exemptions and VA loans can feel complex. If you're a veteran in Houston or Austin, working with a mortgage strategist who understands these specific rules can ensure you maximize your benefits and secure the best possible loan.

Putting these powerful Texas veteran benefits to work on your home loan can make a significant difference. If you're ready to see how your eligibility translates into real purchasing power, apply now and connect with specialists who can guide you through maximizing your qualifications.

Author Bio

David Ghazaryan is the expert mortgage strategist and founder behind iQRATE Mortgages. With a mission to fund home loans that traditional banks won't touch, David specializes in helping clients with unique financial situations, including those recovering from foreclosure or bankruptcy. He expertly crafts smart, strategic, and stress-free mortgages by leveraging a vast network of over 100 lenders to secure competitive rates for investors and homebuyers alike. Praised for exceptional customer service, David has helped hundreds of families with a 97% satisfaction rate, guiding them to the mortgage they deserve.

References

Texas Comptroller - Property Tax Exemptions for Disabled Veterans

U.S. Department of Veterans Affairs - VA Disability Compensation